Table of Contents

- How to Open Sole Proprietorship Bank Account Online

- Step‑by‑Step Guide to Open Sole Proprietorship Bank Account Online

- Key Benefits of an Online Sole Proprietorship Account

- Choosing the Right Bank for Your Sole Proprietorship

- Traditional Big‑Bank Options

- Online‑Only Banks and Fintechs

- Credit Unions

- Common Pitfalls and How to Avoid Them

- Skipping the EIN

- Neglecting State Licensing

- Overlooking Fee Structures

- Not Setting Up Alerts

- Special Situations: When You Need a Second Chance Account

- Integrating Your New Account with Business Tools

- FAQ: Quick Answers About Opening a Sole Proprietorship Bank Account Online

- Do I need an EIN to open an account?

- Can I open the account from any state?

- How long does the verification process take?

- Are there any minimum balance requirements?

- Can I upgrade to a premium business account later?

Starting a one‑person business is exhilarating, but the paperwork that follows can feel like a maze. One of the first—and most essential—tasks is setting up a dedicated bank account. Keeping personal and business finances separate not only simplifies bookkeeping but also projects professionalism to clients and suppliers.

Fortunately, you no longer need to schedule a branch visit, stand in line, or wrestle with endless forms. The digital age has made it possible to open sole proprietorship bank account online in a matter of minutes, provided you have the right documents and a clear game plan. In this guide we’ll walk you through every step, share practical tips, and answer common questions so you can get your account up and running without a hitch.

How to Open Sole Proprietorship Bank Account Online

When you decide to open sole proprietorship bank account online, the process is surprisingly straightforward. Most major banks now offer dedicated portals for business customers, and many fintech platforms specialize in quick onboarding for solo entrepreneurs. Below is a concise roadmap that applies to most U.S. banks, though the exact requirements may vary slightly.

Step‑by‑Step Guide to Open Sole Proprietorship Bank Account Online

- Gather Required Documentation – You’ll typically need a government‑issued ID (driver’s license or passport), your Social Security Number (or EIN if you’ve obtained one), and proof of your business name (DBA filing, state registration, or a fictitious name certificate).

- Choose the Right Bank – Compare fees, transaction limits, integration options, and customer support. If you’re looking for a low‑cost option, the easy business bank account to open guide can help you spot the best fit.

- Start the Online Application – Navigate to the bank’s business banking page and click “Apply Now.” Most platforms will walk you through a secure questionnaire that captures your personal and business details.

- Verify Your Identity – Expect a short video call or a document upload to confirm your identity. Some banks use automated verification tools that check your ID against government databases.

- Fund the Account – A small initial deposit (often $25‑$100) is required to activate the account. You can fund it via an existing personal account, a debit card, or a wire transfer.

- Set Up Online Access – Once approved, you’ll receive login credentials. Take a few minutes to personalize security settings, enable two‑factor authentication, and explore mobile banking features.

- Link Business Tools – Integrate your new account with accounting software (QuickBooks, Xero) or payment processors (PayPal, Stripe). This step streamlines cash flow tracking and reduces manual data entry.

By following these steps, you can open sole proprietorship bank account online with confidence, knowing you’ve covered every essential detail.

Key Benefits of an Online Sole Proprietorship Account

Choosing to open sole proprietorship bank account online isn’t just about convenience; it brings tangible advantages for solo entrepreneurs.

- Speed – Most banks approve applications within 24‑48 hours, letting you start accepting payments right away.

- Lower Costs – Online‑only banks often waive monthly maintenance fees and offer free ACH transfers.

- Enhanced Security – Advanced encryption, biometric login, and real‑time fraud monitoring protect your funds.

- Seamless Integration – Direct API connections to invoicing platforms and payroll services keep your workflow smooth.

- Professional Image – A business‑named account adds credibility when clients see checks or electronic transfers from a legitimate entity.

Choosing the Right Bank for Your Sole Proprietorship

Not every bank is created equal, especially when it comes to serving a one‑person operation. Here are the main categories you’ll encounter, along with pros and cons to help you decide where to open sole proprietorship bank account online.

Traditional Big‑Bank Options

Institutions like Chase, Bank of America, and Wells Fargo have extensive branch networks and robust customer service. They often provide a full suite of business products, from credit cards to merchant services. However, they may charge higher monthly fees and require a higher minimum balance.

If you anticipate needing a line of credit or want the option to meet with a relationship manager, a traditional bank might be the safest bet. For a deeper dive into specific accounts, check out the business bank account for LLC online guide – many of the considerations apply to sole proprietors as well.

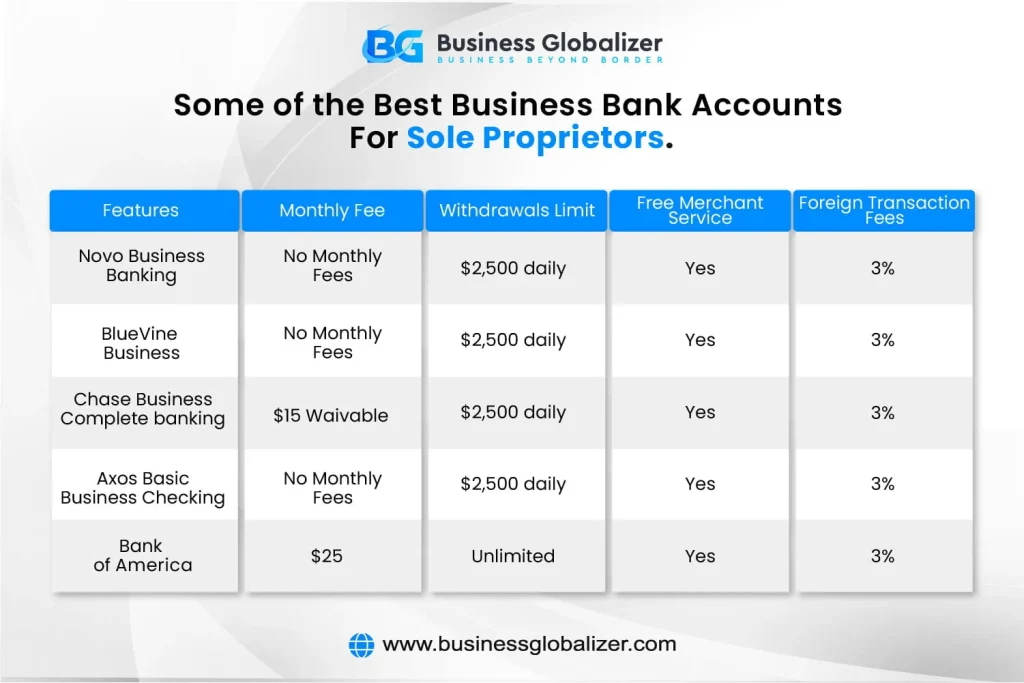

Online‑Only Banks and Fintechs

Neobanks such as Novo, Axos, and Mercury specialize in quick, digital onboarding. They usually waive fees, offer unlimited transactions, and provide modern dashboards that integrate with accounting tools. The trade‑off can be limited in‑person support and fewer loan products.

Credit Unions

Local credit unions often extend a personal touch, lower fees, and competitive rates. Membership requirements vary, but many are open to anyone living or working in a certain area. If you value community focus, a credit union may be a great place to open sole proprietorship bank account online.

Common Pitfalls and How to Avoid Them

Even with a streamlined process, it’s easy to stumble over a few hidden obstacles. Below are the most frequent mistakes and practical ways to sidestep them.

Skipping the EIN

While a sole proprietor can use a Social Security Number, many banks prefer (or even require) an Employer Identification Number (EIN). It’s free, quick to obtain from the IRS, and adds a layer of privacy by keeping your SSN off business documents. Think of the EIN as a business passport.

Neglecting State Licensing

Some industries—like food service or professional consulting—require state licenses or permits. If you haven’t secured those, the bank may reject your application. Double‑check your local regulations before you start the online form.

Overlooking Fee Structures

Even “no‑fee” accounts can have hidden costs: inbound wire fees, excessive ATM usage, or fees for paper statements. Read the fine print, and compare the total cost of ownership across a few providers.

Not Setting Up Alerts

Online banking platforms let you create low‑balance, large‑transaction, or suspicious‑activity alerts. Activating these early helps you catch errors or fraud before they become serious issues.

Special Situations: When You Need a Second Chance Account

If your credit history is less than pristine, you might worry about being denied. Some banks offer “second chance” accounts designed for people rebuilding their financial profile. While these accounts often have limited features, they can serve as a bridge until you qualify for a full‑service business account. Learn more in the second chance bank account guide.

Integrating Your New Account with Business Tools

Opening a sole proprietorship bank account online is just the first step. To truly reap the benefits, link the account to the tools you already use.

- Accounting Software – QuickBooks, FreshBooks, and Xero all support automatic bank feeds, reducing manual reconciliation.

- Payment Processors – Connect Stripe or Square to pull deposits directly into your business account.

- E‑Commerce Platforms – Shopify, WooCommerce, and BigCommerce can route sales revenue straight to your new account.

- Payroll Services – If you ever expand and hire part‑time help, platforms like Gusto will need a business checking number.

By automating these connections, you keep your financial data accurate, up‑to‑date, and ready for tax time.

FAQ: Quick Answers About Opening a Sole Proprietorship Bank Account Online

Do I need an EIN to open an account?

It’s not always mandatory, but most banks strongly prefer it. Obtaining an EIN is free and can be done instantly on the IRS website.

Can I open the account from any state?

Yes, most online banks accept applications nationwide. However, if you choose a regional bank or credit union, you may need to reside in their service area.

How long does the verification process take?

Typically 24‑48 hours, though some institutions finish within a few minutes if you have all documents ready.

Are there any minimum balance requirements?

It varies. Some neobanks have none, while traditional banks may require $500‑$1,000 to avoid monthly fees.

Can I upgrade to a premium business account later?

Absolutely. Most banks let you transition to a higher‑tier account as your revenue grows or as you need additional services like lines of credit.

Whether you’re launching a freelance consulting practice, a home‑based e‑commerce store, or a local service business, the ability to open sole proprietorship bank account online empowers you to manage cash flow efficiently and present a professional front to clients.

Take the time to research your options, gather the necessary paperwork, and follow the step‑by‑step guide outlined above. In just a few clicks, you’ll have a dedicated business account ready to handle deposits, pay vendors, and keep your finances crystal clear. Happy banking, and here’s to the success of your solo venture!