Table of Contents

- Opening a Joint Bank Account Wells Fargo: Requirements and Eligibility

- Opening a Joint Bank Account Wells Fargo: Step‑by‑Step Process

- Benefits of a Joint Account at Wells Fargo

- Things to Consider Before Opening a Joint Account Wells Fargo

- Legal and Financial Implications

- Impact on Credit and Debt

- Account Closure and Ownership Changes

- Frequently Asked Questions About Opening a Joint Bank Account Wells Fargo

- Tips for Managing a Joint Account Effectively

- Alternative Options When a Joint Account Isn’t the Best Fit

Sharing finances with a partner, spouse, or business associate can simplify budgeting, bill payments, and savings goals. One of the most popular ways to do this in the United States is by opening a joint bank account. Among the many banks offering joint accounts, Wells Fargo stands out with its extensive network, robust online tools, and a variety of account options that cater to different needs.

Whether you’re a newlywed looking to combine expenses, roommates managing household costs, or business partners seeking a transparent way to handle cash flow, understanding the process of opening a joint bank account Wells Fargo is essential. This guide walks you through everything from eligibility and required documents to the pros and cons of joint ownership, helping you make an informed decision.

We’ll also sprinkle in practical tips, common pitfalls to avoid, and links to related resources that can deepen your banking knowledge. By the end, you’ll feel confident about taking the next step toward shared financial management.

Opening a Joint Bank Account Wells Fargo: Requirements and Eligibility

Before you head to a branch or start the online application, it’s important to confirm that you and your co‑owner meet Wells Fargo’s criteria. The bank’s joint account policies are designed to protect both parties while ensuring smooth operation.

- Age Requirement: All co‑owners must be at least 18 years old. Minors can be added as authorized users, but they cannot be primary signatories.

- Identification: Valid government‑issued ID such as a driver’s license, state ID, or passport is mandatory for each applicant.

- Social Security Number (SSN) or Tax Identification Number (TIN): Required for tax reporting and credit checks.

- Residency: At least one co‑owner must be a U.S. resident. Non‑resident aliens can sometimes be added, but additional documentation may be needed.

- Credit Check (optional): While not always required for basic checking accounts, some premium accounts may run a soft credit inquiry.

Having these items ready will speed up the application, whether you’re applying online or in person. If you’re curious about opening other types of accounts, check out the guide on how to open a small business bank account online for a broader perspective.

Opening a Joint Bank Account Wells Fargo: Step‑by‑Step Process

Now that you know who can apply, let’s break down the actual steps. Wells Fargo offers both in‑branch and digital routes, giving you flexibility based on your comfort level.

- Choose the Right Account Type: Wells Fargo provides several joint account options, including Everyday Checking, Preferred Checking, and Portfolio by Wells Fargo. Compare fees, interest rates, and perks to pick the best fit.

- Gather Documentation: Assemble IDs, SSNs, proof of address (like a utility bill), and any additional paperwork required for the chosen account.

- Start the Application:

- Online: Visit the Wells Fargo website, select “Open an Account,” and choose “Joint Account.” Follow the prompts to fill out personal information for both owners.

- In‑Branch: Schedule an appointment or walk in. A representative will guide you through the paperwork and answer any questions.

- Set Up Funding: You’ll need an initial deposit, which varies by account type (often $25–$100). Transfer funds from an existing account, use a check, or fund it with cash at a branch.

- Configure Account Features: Decide on overdraft protection, online banking access, debit cards for each owner, and any additional services like mobile alerts.

- Review and Sign: Both parties must sign the agreement. If you’re applying online, each person will receive a verification link to complete the electronic signature.

- Activate Your Account: Once approved, set up online banking, download the Wells Fargo Mobile app, and order checks if needed.

Pro tip: If you already have a personal Wells Fargo account, the joint account setup can be linked to your existing login, making management easier. For a deeper dive into linking accounts, see the article on how to add bank account to E*TRADE.

Benefits of a Joint Account at Wells Fargo

Joint accounts aren’t just about convenience; they also bring tangible financial advantages, especially when you choose a reputable institution like Wells Fargo.

- Shared Access: Both owners can deposit, withdraw, and manage funds, eliminating the need for constant reimbursements.

- Transparency: All transactions are visible to each party, fostering trust and clear communication about spending habits.

- Potential Fee Savings: Many Wells Fargo joint accounts waive monthly fees if combined balances meet a threshold, which can be easier to achieve together.

- Enhanced Credit Opportunities: Consistently positive activity on a joint checking account can improve the credit profiles of both owners, especially when paired with a Wells Fargo credit card.

- Estate Planning Simplicity: Upon the death of one owner, the surviving co‑owner typically retains full access without probate delays, depending on state laws.

Things to Consider Before Opening a Joint Account Wells Fargo

While the perks are appealing, shared accounts also come with responsibilities and potential drawbacks. Here’s what you should weigh before signing the dotted line.

Legal and Financial Implications

Both owners have equal rights to the funds, meaning either person can withdraw the entire balance without the other’s consent. This level of trust is crucial; if one party mismanages money, the other may face the consequences, including overdraft fees or negative impacts on credit.

Impact on Credit and Debt

Although checking accounts don’t directly affect credit scores, associated services—like overdraft protection linked to a credit line—can. If one owner defaults on an overdraft, the other’s credit could be affected. Review the terms of any linked credit products carefully.

Account Closure and Ownership Changes

Should the relationship end, dividing the balance can become complicated. Wells Fargo requires both parties to agree on closure or a change of ownership, which may involve legal steps if disputes arise. Keeping records of contributions can help smooth this process.

Frequently Asked Questions About Opening a Joint Bank Account Wells Fargo

- Can I add a third person to a joint account? Wells Fargo allows “joint with right of survivorship” for two owners. Adding a third person typically requires opening a separate account or using a “business account” structure.

- Do joint accounts have separate account numbers? No, the joint account shares a single account number and routing number, though each owner can receive individual debit cards.

- What happens if one owner passes away? The surviving owner generally retains full access, but you should file a death certificate with the bank to remove the deceased’s name from the account.

- Are there any special fees for joint accounts? Wells Fargo does not charge extra fees solely for having a joint account. However, standard account fees (monthly maintenance, overdraft) still apply unless waived by balance or activity criteria.

- Can I set spending limits for each co‑owner? The bank does not provide built-in per‑owner limits, but you can use budgeting apps or set up alerts to monitor activity.

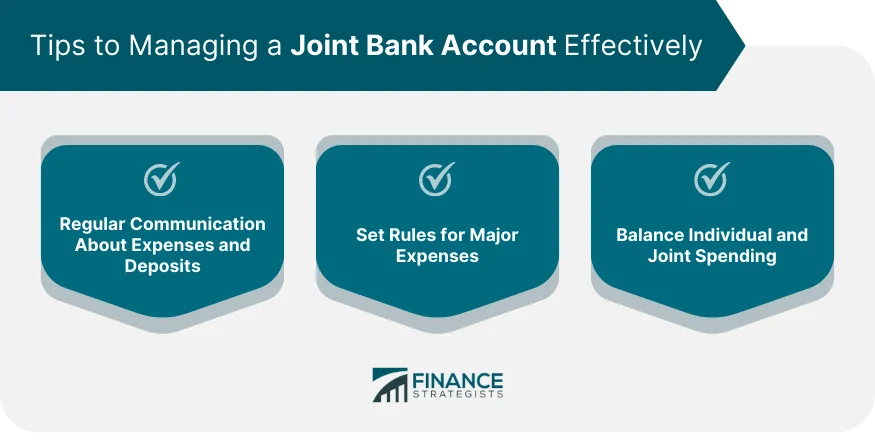

Tips for Managing a Joint Account Effectively

Successful joint account management hinges on communication and clear guidelines. Here are some best practices to keep the partnership healthy.

- Establish Shared Goals: Define what the account will be used for—monthly bills, savings, travel fund—and agree on contribution amounts.

- Set Up Alerts: Use Wells Fargo’s mobile app to receive real‑time notifications for deposits, withdrawals, and low balances.

- Maintain Separate Personal Accounts: Keep a personal account for discretionary spending to avoid friction over “personal” purchases.

- Schedule Regular Check‑Ins: Review statements together monthly to discuss any unusual activity or upcoming expenses.

- Document Large Transactions: For transparency, note the purpose of sizable withdrawals or deposits in a shared spreadsheet or note‑keeping app.

By following these strategies, you’ll reduce the risk of misunderstandings and make the most of the convenience a joint account offers.

Alternative Options When a Joint Account Isn’t the Best Fit

If the idea of shared ownership feels too risky, consider alternatives that still provide collaborative financial management without full joint responsibility.

- Authorized User Access: One person holds the primary account while the other is added as an authorized user, granting debit card access but not ownership.

- Shared Money Apps: Services like Venmo, Zelle, or PayPal enable easy transfers and split bills without a joint account.

- Separate Accounts with Automatic Transfers: Each person maintains their own account and sets up recurring transfers to a shared “expense” account for bills.

These options can be particularly useful for couples or roommates who prefer to keep individual financial autonomy while still collaborating on shared expenses.

Opening a joint bank account Wells Fargo can be a straightforward and rewarding process when you enter it with a clear understanding of the steps, benefits, and responsibilities involved. By preparing the required documentation, selecting the right account type, and establishing solid communication habits, you set the stage for smoother financial cooperation.

Remember, the key to any shared financial venture is trust, transparency, and regular check‑ins. Whether you’re budgeting for a new home, planning a vacation, or simply managing day‑to‑day expenses, a joint Wells Fargo account can become a powerful tool in your financial toolbox.