Table of Contents

- wells fargo bank minimum opening deposit – Checking Accounts Overview

- wells fargo bank minimum opening deposit – Savings Accounts Explained

- Why the Minimum Deposit Matters and How It Impacts Fees

- Tips to Meet the Wells Fargo Bank Minimum Opening Deposit

- How the Minimum Deposit Differs for Business Accounts

- Online vs. In‑Branch: Does the Deposit Requirement Change?

- Special Cases: Student and Senior Accounts

- Frequently Asked Questions About the Minimum Deposit

- Bottom Line: Planning Your First Deposit Wisely

Thinking about opening a new checking or savings account with Wells Fargo? You’re not alone—millions of Americans turn to this big‑name bank for its extensive branch network, solid reputation, and a variety of account choices. Yet, before you sign that application, one of the first questions on most people’s minds is the minimum opening deposit. How much cash do you actually need to get started, and what does that amount unlock in terms of features and fees?

In this guide we’ll break down the exact figures for each major Wells Fargo account, explore the nuances that can affect the required deposit, and share practical tips to help you meet the threshold without stretching your budget. Whether you’re a student, a recent graduate, or someone looking to switch banks, understanding the Wells Fargo bank minimum opening deposit will save you time and prevent any surprise fees down the line.

wells fargo bank minimum opening deposit – Checking Accounts Overview

Wells Fargo offers several checking options, each geared toward a different customer segment. The most popular is the Everyday Checking account, which is designed for everyday transactions with no monthly service fee if you meet certain criteria. The minimum opening deposit for this account is **$25**, a relatively low barrier compared to some competitors. However, other checking products have different requirements:

- Clear Access Banking: Geared toward customers who may have limited banking history, this account requires a $0 opening deposit, but it does charge a modest monthly fee of $5 unless you meet balance or direct deposit conditions.

- Premium Checking: Ideal for high‑balance clients, this account demands a $10,000 opening deposit to unlock premium benefits such as interest earnings, waived fees, and personalized service.

If you’re wondering how the Free Checking option fits into this picture, the answer is that the Everyday Checking can become fee‑free with a $500 average daily balance, making the $25 deposit merely a starting point.

wells fargo bank minimum opening deposit – Savings Accounts Explained

Savings accounts at Wells Fargo also vary in their opening deposit requirements. The standard Way2Save Savings account, which is a solid choice for building an emergency fund, asks for a **$25** minimum deposit. The more interest‑bearing Platinum Savings, however, requires a $100 opening deposit to qualify for higher yields.

For those who prefer a high‑yield, no‑maintenance-fee option, the Wells Fargo online savings account also starts at a $0 minimum deposit, but you’ll need to maintain a $300 minimum daily balance to avoid the $5 monthly fee.

Why the Minimum Deposit Matters and How It Impacts Fees

Understanding the Wells Fargo bank minimum opening deposit is more than just a number—it directly influences the fee structure and benefits you’ll receive. Most accounts waive monthly maintenance fees if you maintain a certain balance, which often aligns with the opening deposit amount. For example, the Everyday Checking account’s $25 opening deposit can be seen as a stepping stone: if you quickly grow that balance to $500, you’ll enjoy a fee‑free experience.

Conversely, failing to meet the required minimum can trigger monthly fees that eat into your earnings. A $5 fee on a $25 balance is a 20% hit each month—hardly ideal for anyone trying to save. That’s why many customers choose to deposit a little extra beyond the minimum, just to create a buffer.

Tips to Meet the Wells Fargo Bank Minimum Opening Deposit

- Leverage Direct Deposit: Set up your paycheck to be directly deposited into your new Wells Fargo account. Some accounts waive fees with a recurring direct deposit of $500 or more.

- Combine Accounts: Opening both a checking and a savings account simultaneously can sometimes allow you to meet combined balance requirements, reducing overall fees.

- Use an Existing Account Transfer: Transfer funds from an existing bank or a friend’s account to satisfy the minimum quickly and avoid cash‑handling hassles.

- Take Advantage of Promotions: Wells Fargo occasionally runs promotional offers that waive the opening deposit or provide bonus cash for new customers.

These strategies are especially handy if you’re juggling a tight budget but still want the security and convenience that a big‑bank like Wells Fargo provides.

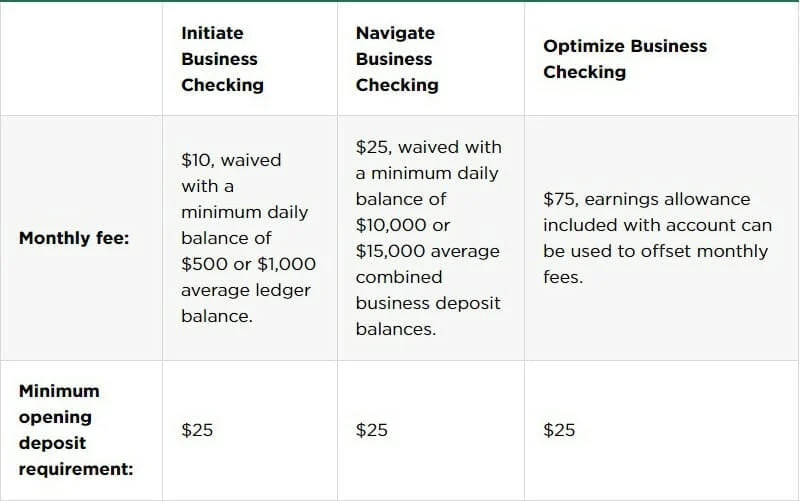

How the Minimum Deposit Differs for Business Accounts

If you’re a small business owner, the Wells Fargo bank minimum opening deposit takes on a slightly different shape. For most business checking products, the required opening deposit is **$100**, which is modest compared to many regional banks that ask for $500 or more. However, the Premium Business Checking account—tailored for high‑volume businesses—requires a $10,000 minimum deposit, mirroring the premium personal checking tier.

Opening a business account can also be streamlined if you’ve already opened a personal account with Wells Fargo. Existing relationships often lead to reduced paperwork and sometimes a waiver of the opening deposit, especially if you maintain a combined balance above a certain threshold.

For a deeper dive into opening a business account, you might find the article Easiest Bank to Open a Business Account – Your Complete Guide useful.

Online vs. In‑Branch: Does the Deposit Requirement Change?

One common misconception is that opening an account online might have a higher minimum deposit than doing it in a branch. With Wells Fargo, the answer is generally no. Whether you apply through the website, mobile app, or walk into a local branch, the Wells Fargo bank minimum opening deposit remains consistent across channels for the same product.

That said, the online application process can make it easier to fund your new account instantly via an ACH transfer from another bank. This quick funding helps you meet the minimum deposit requirement without waiting for a mailed check or a cash deposit.

Special Cases: Student and Senior Accounts

Wells Fargo also offers tailored accounts for students and seniors, often with relaxed minimum deposit rules. The Student Checking account, for instance, requires only a $5 opening deposit, while the Senior Savings account may waive the $25 minimum if you’re over 65 and meet certain income criteria.

These specialized products illustrate how the Wells Fargo bank minimum opening deposit can be flexible, adapting to the life stage and financial situation of the customer.

Frequently Asked Questions About the Minimum Deposit

- Can I open an account with less than the required minimum? Technically, you can start the application, but the account will either be declined or immediately flagged for a fee if the minimum isn’t met within a few days.

- Do I get a refund if I close the account early? If you close the account before the minimum balance period ends and there are no fees, Wells Fargo will return your remaining funds, but any accrued fees will be deducted.

- Is the minimum deposit the same for joint accounts? Yes, the minimum deposit applies per account, regardless of the number of owners.

- What happens if I fall below the minimum after opening? Falling below the minimum typically triggers a monthly maintenance fee unless you quickly bring the balance back up.

Bottom Line: Planning Your First Deposit Wisely

When you sit down to open a new account with Wells Fargo, the key takeaway is that the Wells Fargo bank minimum opening deposit is designed to be accessible yet purposeful. With $25 to start a basic checking or savings account, most consumers can get on board without a big upfront outlay. However, the real advantage lies in using that initial deposit as a foundation for meeting ongoing balance requirements, thereby avoiding fees and unlocking extra perks.

By planning ahead—setting up direct deposit, bundling accounts, or taking advantage of promotional offers—you can not only meet the minimum but also set yourself up for a healthier banking relationship. Whether you’re opening a personal account, a student account, or a business account, the strategies outlined here will help you navigate the Wells Fargo bank minimum opening deposit with confidence and clarity.

Ready to take the next step? Head over to Wells Fargo’s website, compare the account options, and decide which minimum deposit aligns with your financial goals. A small deposit today can lead to big financial benefits tomorrow.