Table of Contents

- Business Bank Accounts with No Credit Check: What to Look For

- How Business Bank Accounts with No Credit Check Work

- Top Providers Offering Business Bank Accounts with No Credit Check

- 1. Azlo (Now Part of BBVA USA)

- 2. Novo

- 3. BlueVine Business Checking

- 4. Mercury (For Tech Startups)

- Step‑by‑Step Guide to Open a Business Bank Account with No Credit Check

- Common Myths About No‑Credit‑Check Business Accounts

- Myth 1: No Credit Check Means No Security

- Myth 2: You Can’t Get a Loan Later

- Myth 3: These Accounts Are Only for Very Small Businesses

- Tips to Maximize the Benefits of a No‑Credit‑Check Account

- When to Consider a Traditional Credit‑Check Account Instead

- Future Trends: Will No‑Credit‑Check Accounts Stay Around?

Starting a business is exciting, but the paperwork that comes with it can feel like a maze. One of the first hurdles many founders hit is opening a business bank account—especially when they have a less‑than‑perfect credit history. The good news is that you don’t always need a spotless credit score to get your finances in order. In recent years, a growing number of banks and fintechs have rolled out business bank accounts with no credit check, making it easier for startups, freelancers, and small‑scale enterprises to separate personal and business money without the usual red tape.

Why does this matter? For many entrepreneurs, a traditional credit check can be a deal‑breaker. It might delay cash flow, force you to use a personal account, or even push you to seek expensive alternatives. By choosing an account that skips the credit review, you keep your options open, preserve your credit line for other uses, and get access to essential banking tools faster. In this guide we’ll walk through the landscape of business bank accounts with no credit check, highlight the top providers, and share actionable tips to pick the right one for your needs.

Whether you’re a solo consultant, a growing e‑commerce store, or a nonprofit looking to formalize its finances, the right banking partner can make a huge difference. Let’s dive into the fundamentals, explore the best “no‑credit‑check” options, and give you a roadmap to get started without the usual hassle.

Business Bank Accounts with No Credit Check: What to Look For

Not every “no credit check” account is created equal. Below are the core features you should evaluate before committing:

- Fees and Minimum Balances – Some providers waive monthly fees but require a minimum balance; others keep it free regardless of activity.

- Deposit & Withdrawal Options – Look for unlimited ACH transfers, mobile check deposits, and easy access to cash via partner ATMs.

- Integration Capabilities – If you use accounting software like QuickBooks or Xero, ensure the bank syncs smoothly.

- Customer Support – 24/7 chat or phone support can be a lifesaver when you’re juggling invoices and payroll.

- Security Measures – FDIC insurance, two‑factor authentication, and fraud monitoring are non‑negotiable.

Understanding these criteria helps you narrow down the field and avoid accounts that look good on paper but fall short in everyday use. Below we break down the most popular providers that explicitly advertise business bank accounts with no credit check.

How Business Bank Accounts with No Credit Check Work

When a bank says it won’t run a credit check, it’s typically relying on alternative verification methods. Instead of pulling your personal or business credit report, they’ll ask for:

- Business formation documents (LLC operating agreement, articles of incorporation).

- Employer Identification Number (EIN) issued by the IRS.

- Proof of address (utility bill, lease, or a recent bank statement).

- A short questionnaire about expected monthly transaction volume.

These data points give the bank enough confidence to open the account while keeping the process quick and low‑cost. Some fintechs even let you complete the entire onboarding via a mobile app, uploading documents with your phone’s camera.

Top Providers Offering Business Bank Accounts with No Credit Check

Below is a snapshot of the most reputable banks and fintech platforms that currently offer business bank accounts with no credit check. Each comes with its own set of perks, so match the features to your business model.

1. Azlo (Now Part of BBVA USA)

Azlo was a pioneer in the “no‑credit‑check” space, and its integration into BBVA USA kept many of its original benefits. Highlights include:

- No monthly maintenance fees.

- Unlimited ACH transfers.

- Free online invoicing tools.

- Full FDIC insurance through BBVA USA.

Because the platform is fully digital, you can open an account in under ten minutes—perfect for solo entrepreneurs who need to get moving fast.

2. Novo

Novo positions itself as a “bank for the modern business.” It skips credit checks entirely and focuses on simplicity:

- No minimum balance, no hidden fees.

- Integrated with Stripe, PayPal, and other payment processors.

- Free transfers to other banks via ACH.

- 24/7 chat support with real‑time help.

If you run an online store or a subscription‑based service, Novo’s seamless connection to payment gateways can shave hours off your bookkeeping each month.

3. BlueVine Business Checking

BlueVine offers a high‑interest checking account without a credit pull. Its standout features are:

- Up to 1.0% APY on balances up to $100,000.

- Unlimited transactions and no monthly fees.

- Easy integration with popular accounting software.

- Access to a line of credit (optional, separate credit check).

For businesses that keep a healthy cash reserve, the interest‑earning component can add a nice boost to your bottom line.

4. Mercury (For Tech Startups)

Mercury targets venture‑backed startups but is open to any tech‑focused company. While it doesn’t require a credit check, it does ask for a detailed business plan and funding source:

- Free domestic and international wires.

- API access for custom integrations.

- Dedicated account managers for high‑growth companies.

- Robust security with multi‑factor authentication.

Mercury’s “no‑credit‑check” policy makes it attractive for early‑stage startups that haven’t built a credit history yet.

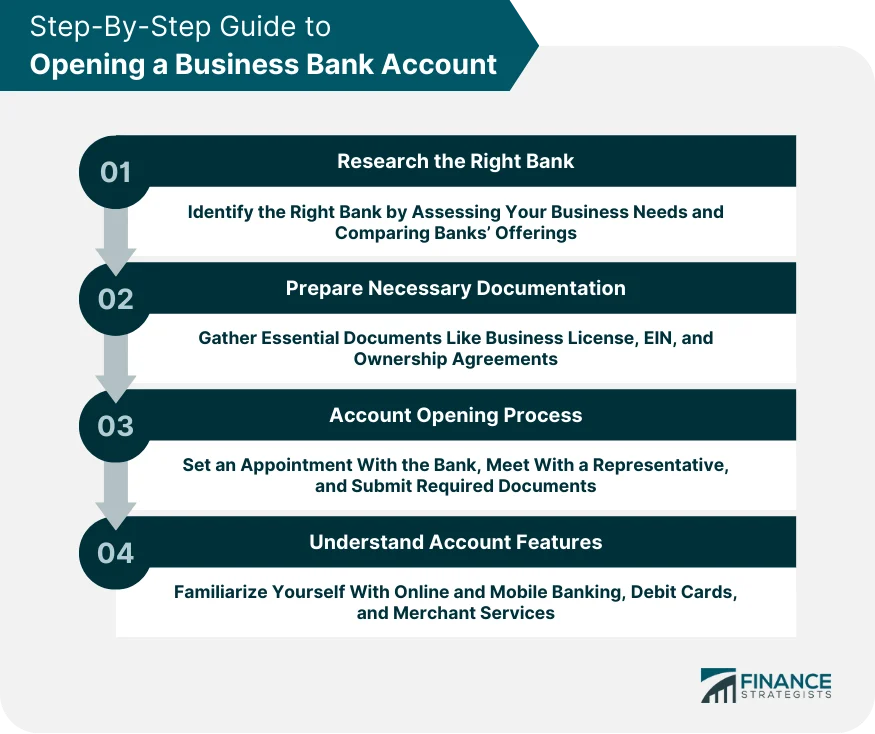

Step‑by‑Step Guide to Open a Business Bank Account with No Credit Check

Even though the process is streamlined, it’s still helpful to follow a checklist. Here’s a practical roadmap you can adapt:

- Gather Your Documentation – Have your EIN, formation documents, and a proof‑of‑address ready. A digital copy works for most online banks.

- Choose the Right Provider – Match the features discussed above to your business needs. If you’re unsure, start with a free‑fee option like Novo.

- Complete the Online Application – Fill out the basic info, upload your documents, and answer any transaction‑volume questions.

- Verify Your Identity – Expect a quick video call or a selfie with your ID, especially for fintechs that need to meet KYC regulations.

- Fund the Account (If Required) – Some banks ask for a small opening deposit; others, like BlueVine, let you start with $0.

- Set Up Integrations – Connect your new account to accounting tools, payment processors, or payroll services.

- Order Debit Cards & Checks – Most providers ship a debit card within a week; check ordering may take longer.

For a real‑world example, you can read how to open a joint bank account at Wells Fargo in the How to Open a Joint Bank Account at Wells Fargo – Complete Guide article, which outlines similar verification steps that apply to many business accounts.

Common Myths About No‑Credit‑Check Business Accounts

When you start hearing about business bank accounts with no credit check, a few misconceptions pop up. Let’s debunk the most persistent ones:

Myth 1: No Credit Check Means No Security

All FDIC‑insured banks must follow strict security protocols, regardless of credit check policies. You’ll still get fraud monitoring, encryption, and two‑factor authentication. The “no credit check” label simply refers to the underwriting process, not to the safety of your funds.

Myth 2: You Can’t Get a Loan Later

While a credit‑free account won’t automatically grant you a line of credit, many providers (like BlueVine) offer optional credit products that involve a separate credit assessment. Having a well‑managed checking account can actually improve your eligibility when you decide to apply for a loan.

Myth 3: These Accounts Are Only for Very Small Businesses

It’s true that many fintechs target freelancers and micro‑businesses, but larger entities can also benefit. For instance, Mercury’s API and international wire capabilities make it a solid choice for tech firms scaling globally.

Tips to Maximize the Benefits of a No‑Credit‑Check Account

Opening a business bank account with no credit check is just the first step. To get the most out of it, keep these strategies in mind:

- Maintain Consistent Transaction Volume – Regular deposits and withdrawals signal healthy cash flow and can unlock higher limits or additional features.

- Use Integrated Accounting – Sync your account to QuickBooks, Xero, or Wave to automate reconciliation and reduce manual errors.

- Leverage Free International Payments – If you sell abroad, choose a provider that offers low‑cost or free wire transfers (Mercury excels here).

- Monitor Fees Closely – Some “no‑credit‑check” accounts have hidden costs for out‑of‑network ATM usage or excess transactions. Set alerts to avoid surprise charges.

- Keep Personal and Business Finances Separate – Even if you’re the only employee, a dedicated business account protects you from liability and simplifies tax reporting.

For a deeper dive into fee structures, the US Bank Silver Business Checking Minimum Balance – What You Need to Know article outlines how minimum balance requirements can affect your bottom line.

When to Consider a Traditional Credit‑Check Account Instead

Even though business bank accounts with no credit check are convenient, there are scenarios where a traditional account might be a better fit:

- High‑Volume Cash Transactions – Some brick‑and‑mortar banks offer better cash‑handling services and higher deposit limits.

- Established Credit History – If you already have a strong personal or business credit score, a traditional account may provide higher credit lines and better loan rates.

- Complex Banking Needs – Services like merchant cash advances, escrow accounts, or sophisticated treasury management often require a full‑service bank.

In such cases, you could maintain both a no‑credit‑check account for day‑to‑day operations and a traditional account for larger, specialized transactions.

Future Trends: Will No‑Credit‑Check Accounts Stay Around?

The demand for frictionless banking experiences isn’t going away. As more entrepreneurs launch with limited credit history, fintechs will continue to innovate around alternative underwriting models. Expect to see:

- AI‑Driven Risk Assessment – Real‑time cash‑flow analysis could replace credit scores entirely.

- Embedded Banking Services – Platforms like Shopify and Square may embed full banking suites directly into their ecosystems.

- Increased Regulatory Support – Regulators are paying close attention to consumer protection, which could standardize “no‑credit‑check” offerings across the industry.

Staying informed about these trends ensures you can adapt your banking strategy as the landscape evolves.

Choosing a business bank account with no credit check can be a game‑changer for entrepreneurs who need speed, flexibility, and low barriers to entry. By understanding the key features, vetting providers carefully, and following a clear onboarding checklist, you’ll set up a solid financial foundation without the usual credit‑score anxiety. Remember to keep an eye on fees, integrate your accounting tools, and stay open to upgrading as your business grows. With the right account in place, you can focus on what truly matters—building your brand, serving your customers, and scaling your venture.