Table of Contents

- Understanding Credit Card and Debit Card Processing

- Key Players in Credit Card and Debit Card Processing

- How Fees Are Calculated in Credit Card and Debit Card Processing

- Differences Between Credit Card and Debit Card Processing

- Tips to Optimize Your Credit Card and Debit Card Processing Costs

- Security Measures in Credit Card and Debit Card Processing

- Understanding Chargebacks and Their Impact

- Emerging Trends Shaping the Future of Credit Card and Debit Card Processing

- Choosing the Right Processor for Your Business

In today’s cash‑less world, the phrase “credit card and debit card processing” pops up every time you swipe, tap, or click “pay now.” Whether you’re a small café owner watching the register tick or a tech‑savvy shopper ordering the latest gadget, understanding the machinery behind that transaction can save you money, protect your data, and boost confidence in digital payments.

Behind every smooth checkout lies a complex dance of networks, encryption protocols, and fee structures. It’s not just about a plastic card; it’s about a whole ecosystem that includes the cardholder, the merchant, the acquiring bank, the issuing bank, and the payment processor. When these pieces work together seamlessly, you barely notice the transaction. When something goes wrong, you might see a declined payment, a mysterious charge, or an unexpected fee.

This article unpacks the entire journey of a payment, from the moment a consumer inserts a card to the final settlement in a merchant’s account. We’ll break down the types of processors, compare credit card and debit card processing nuances, and share practical tips to keep costs low and security high. By the end, you’ll have a clear picture of how the system operates and what you can do to optimize it for your business or personal use.

Understanding Credit Card and Debit Card Processing

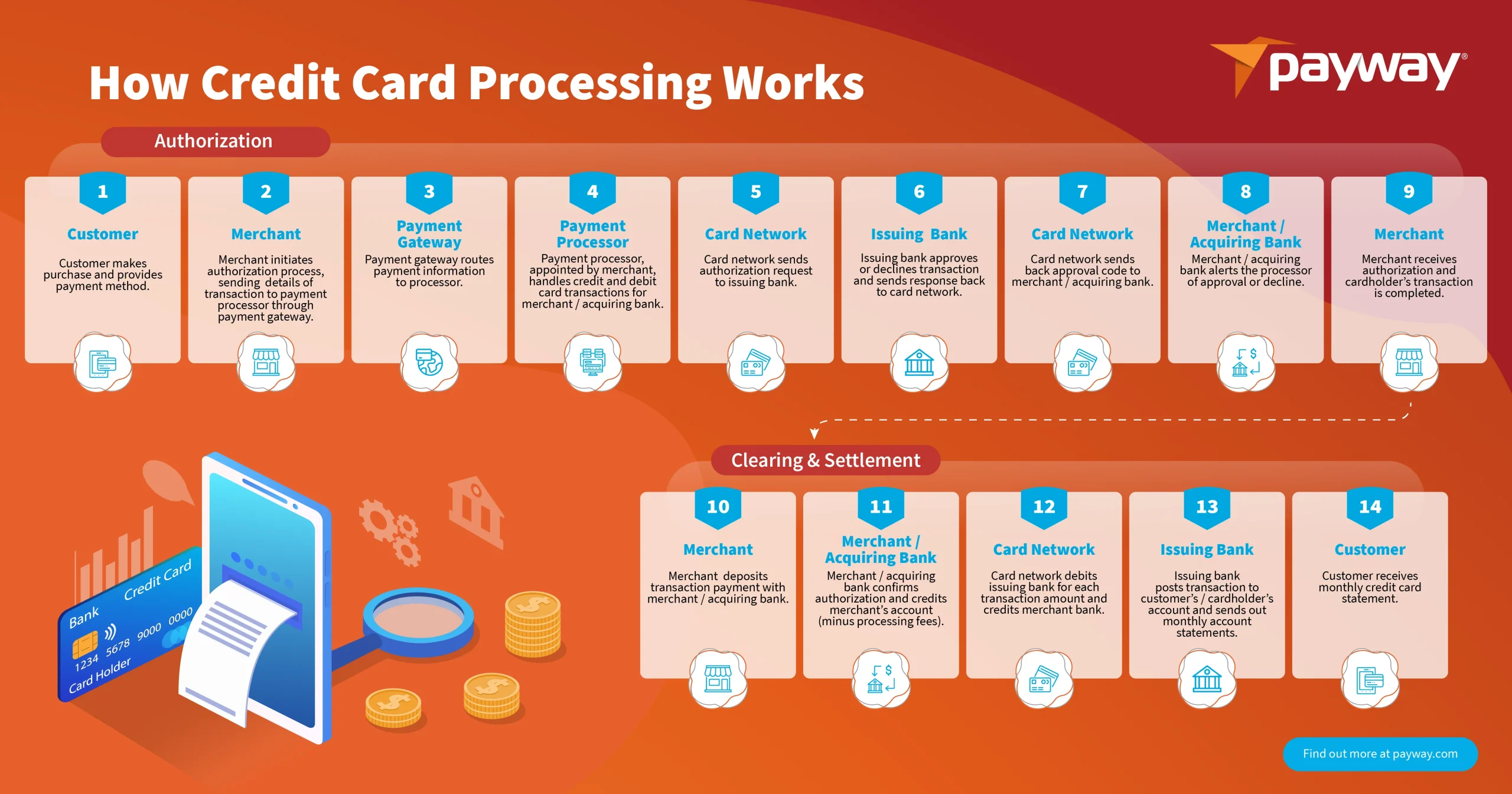

At its core, credit card and debit card processing is the electronic movement of funds from a consumer’s bank to a merchant’s account. While both use similar technology—magnetic stripes, EMV chips, or contactless NFC—the underlying financial relationships differ. Credit cards pull from a revolving line of credit offered by the issuing bank, whereas debit cards draw directly from the cardholder’s checking or savings account.

The process can be divided into several key stages:

- Authorization: The merchant sends a transaction request to the processor, which forwards it to the card network (Visa, Mastercard, etc.) and then to the issuing bank. The bank checks for sufficient funds or credit limit and returns an approval or decline.

- Authentication: Especially for online purchases, additional security steps—like 3‑D Secure (Verified by Visa, Mastercard SecureCode)—confirm the cardholder’s identity.

- Batching: Throughout the day, approved transactions are grouped into a “batch” and submitted for settlement.

- Clearing and Settlement: The card network routes the transaction details to the issuing bank, which transfers the funds (minus interchange fees) to the acquiring bank. The merchant finally receives the net amount, usually within 1–3 business days.

Understanding each phase helps you spot where fees are added, where delays can happen, and where security vulnerabilities might arise.

Key Players in Credit Card and Debit Card Processing

Think of the ecosystem as a relay race, with each participant passing the baton smoothly to the next:

- Cardholder: The consumer who initiates the purchase.

- Merchant: The business that accepts the card and provides goods or services.

- Acquirer (Acquiring Bank): The financial institution that processes the merchant’s transactions and deposits the funds.

- Issuer (Issuing Bank): The bank that issued the card to the consumer and ultimately pays the merchant.

- Payment Processor: The technology platform that routes transaction data between the merchant, acquirer, and card networks.

- Card Networks: Visa, Mastercard, American Express, Discover, and regional networks that set the rules and fees for moving money.

For businesses looking to streamline costs, exploring different processors can be as valuable as negotiating better merchant accounts. Check out Credit Card Processing for High Risk – A Complete Guide for insights on selecting a processor that matches your risk profile.

How Fees Are Calculated in Credit Card and Debit Card Processing

Every time a payment is processed, a series of fees get deducted before the merchant sees the final amount. The most common fee components include:

- Interchange Fee: Set by the card networks, this is the bulk of the cost—typically 1%–3% of the transaction plus a fixed amount (e.g., $0.10). Credit cards generally carry higher interchange rates than debit cards because of the credit risk.

- Assessment Fee: Charged by the card network itself, usually a small percentage (0.13%–0.15%).

- Processor Markup: The processor adds a surcharge—either a flat fee per transaction, a percentage, or a blend of both.

- Monthly/Annual Fees: Some processors charge account maintenance fees, gateway fees, or PCI compliance fees.

To keep expenses down, many merchants negotiate a “blended rate” or switch to a “tiered pricing” model that aligns fees with transaction volume. If your business is credit‑heavy, consider a Corporate Credit Card Without Personal Guarantee that may offer lower processing costs through volume discounts.

Differences Between Credit Card and Debit Card Processing

While the technical steps look almost identical, the financial implications vary considerably:

- Funding Source: Credit cards pull from a line of credit; debit cards pull from deposited cash.

- Interchange Rates: Debit transactions typically enjoy lower interchange fees (often under 1%) compared to credit cards.

- Risk Profile: Credit card transactions involve higher fraud risk, leading to more robust authentication requirements.

- Consumer Protections: Credit cards usually provide stronger charge‑back rights, which can affect merchant liability.

- Settlement Speed: Debit transactions can settle faster (often same‑day) because the funds are already in the consumer’s bank.

For merchants, offering both options widens the customer base, but it also means juggling two fee structures. Some processors provide a “dual‑processing” solution that aggregates data, making reconciliation easier.

Tips to Optimize Your Credit Card and Debit Card Processing Costs

- Analyze Your Transaction Mix: If debit makes up a large portion of sales, negotiate lower debit rates or consider a debit‑only terminal.

- Choose the Right Pricing Model: High‑volume merchants often benefit from interchange‑plus pricing, while low‑volume shops may prefer flat‑rate plans.

- Reduce Card‑Not‑Present (CNP) Fraud: Implement 3‑D Secure, tokenization, and address verification (AVS) to lower charge‑back risk.

- Leverage Batch Timing: Submit batches at the end of each business day rather than multiple times, which can reduce per‑batch fees.

- Stay PCI Compliant: Non‑compliance can lead to hefty fines. Use tokenization or point‑to‑point encryption (P2PE) to protect data.

If you run a high‑risk business—think travel agencies, nutraceuticals, or subscription services—explore specialized solutions. The Interest Free Credit Cards for Business: A Complete Guide outlines options that combine low‑interest financing with tailored processing rates.

Security Measures in Credit Card and Debit Card Processing

Security is the backbone of any payment system. A single breach can damage reputation, trigger regulatory penalties, and cost millions. Modern processors employ multiple layers of protection:

- EMV Chip Technology: Physical cards with chips generate unique transaction codes, making counterfeit fraud much harder.

- Tokenization: Replaces sensitive card data with a non‑recoverable token, especially useful for recurring billing.

- End‑to‑End Encryption (E2EE): Encrypts data from the point of capture (card reader) to the processor, preventing interception.

- Fraud Detection Algorithms: Machine learning models flag anomalous patterns—such as sudden high‑value purchases from new locations.

Businesses should also enforce strong password policies, regular software updates, and employee training on phishing. The cost of a data breach far outweighs the modest investment in robust security tools.

Understanding Chargebacks and Their Impact

When a cardholder disputes a transaction, the issuing bank initiates a chargeback. This reverses the payment and may impose a fee on the merchant. Common reasons include:

- Fraudulent transaction (card not present)

- Product not received or significantly not as described

- Technical errors (duplicate billing, processing errors)

To minimize chargebacks, keep clear records, provide accurate product descriptions, and use reliable shipping methods with tracking. A well‑documented dispute response can often reverse the chargeback in your favor.

Emerging Trends Shaping the Future of Credit Card and Debit Card Processing

Technology evolves faster than most regulatory frameworks, and payment processing is no exception. Here are a few trends that are already influencing the market:

- Contactless Payments: NFC‑enabled cards and smartphones (Apple Pay, Google Pay) are growing at double‑digit rates, especially post‑pandemic.

- Buy‑Now‑Pay‑Later (BNPL): Services like Klarna and Afterpay sit on top of traditional processing, adding new fee structures and consumer credit considerations.

- Open Banking APIs: Direct bank‑to‑bank transfers (e.g., ACH, Faster Payments) are emerging as low‑cost alternatives to card payments, especially for large B2B invoices.

- Artificial Intelligence: AI-driven fraud detection reduces false declines and improves approval rates.

- Regulatory Changes: Initiatives like the European PSD2 and US’s Durbin Amendment reshape interchange fees and data sharing rules.

Staying ahead means regularly reviewing your processor’s roadmap and ensuring your payment stack can integrate new methods without friction.

Choosing the Right Processor for Your Business

When evaluating providers, consider the following checklist:

- Transparency of fee structure (interchange‑plus vs. flat‑rate)

- Integration capabilities with your POS, e‑commerce platform, and accounting software

- Support for emerging payment methods (contactless, BNPL, crypto)

- Security certifications (PCI DSS Level 1, tokenization, P2PE)

- Customer support responsiveness and SLA guarantees

Many businesses start with a “all‑in‑one” solution—think Square or Stripe—but as volume grows, a dedicated merchant account with a specialized processor can yield better rates.

In summary, credit card and debit card processing is far more than a simple swipe. It’s an intricate web of technology, finance, and compliance that directly impacts your bottom line and customer experience. By understanding the fee breakdown, security protocols, and emerging trends, you can make informed decisions—whether you’re a budding entrepreneur setting up your first online store or a seasoned CFO optimizing a multinational payment strategy.

Remember, the goal isn’t just to accept payments; it’s to do so efficiently, securely, and profitably. Keep an eye on your processing statements, renegotiate terms when possible, and stay updated on new payment innovations. Your diligence today translates into smoother transactions and healthier margins tomorrow.