Table of Contents

- chase business credit card pre approval

- chase business credit card pre approval: What You Need to Know

- How to Request a Pre‑Approval From Chase

- 1. Gather Your Business Documentation

- 2. Check Your Personal Credit Score

- 3. Log Into Your Chase Online Account

- 4. Complete the Soft Pull Form

- 5. Review Your Options

- Choosing the Right Chase Business Card After Pre‑Approval

- Tips to Turn Pre‑Approval Into a Full Approval

- 1. Keep Your Credit Utilization Low

- 2. Strengthen the Business Banking Relationship

- 3. Highlight Consistent Revenue

- 4. Provide a Personal Guarantee with Confidence

- 5. Use the Right Timing

- Benefits of a Chase Business Credit Card

- Common Misconceptions About Pre‑Approval

- Myth 1: Pre‑Approval Guarantees a Card

- Myth 2: Pre‑Approval Means No Credit Check

- Myst 3: You Can Get Unlimited Credit

- What to Do If You’re Not Pre‑Approved

- Final Thoughts

When you run a small business, cash flow is the lifeblood that keeps everything moving. One of the fastest ways to give that flow a boost is by securing a business credit card that not only offers a solid credit line but also comes with perks tailored for entrepreneurs. That’s where chase business credit card pre approval steps onto the stage. Instead of diving straight into a full application that could affect your credit score, a pre‑approval gives you a sneak peek at the limits and terms you’re likely to qualify for.

But pre‑approval isn’t a magic wand. It’s a signal from Chase that, based on the data they already have, you’re a good candidate for one of their business cards. Understanding how that signal works, what you need to line up before you start, and how to translate a pre‑approval into a fully funded card can make the difference between a smooth onboarding and a frustrating dead‑end.

In this guide we’ll break down the whole process: the eligibility checklist, the steps to request a pre‑approval, the most popular Chase business cards that offer it, and some pro tips to maximize your chances. By the end you’ll have a clear roadmap to get that coveted business credit line without unnecessary hiccups.

chase business credit card pre approval

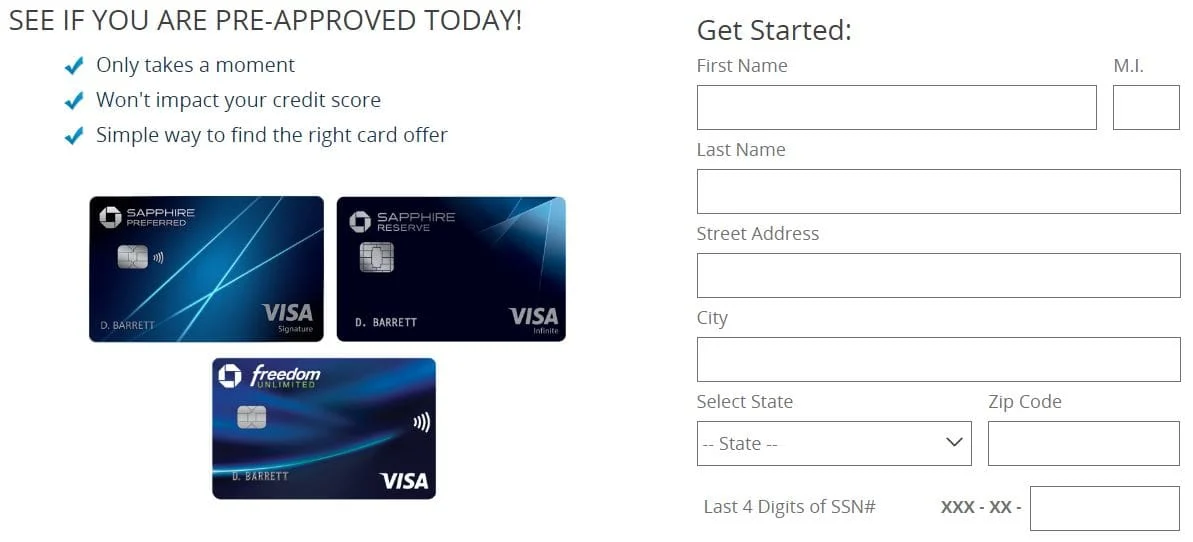

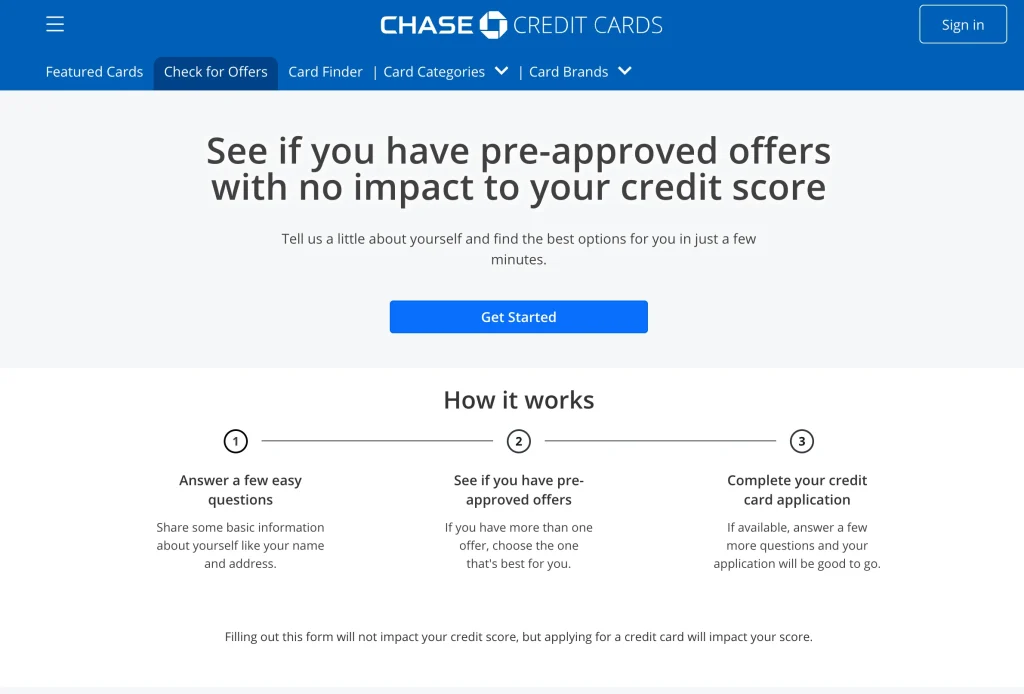

Chase offers a quick “soft pull” pre‑approval tool on its website and through the mobile app. A soft pull checks your credit profile without leaving a hard inquiry on your credit report, meaning your score stays untouched while you gauge eligibility. If you’re pre‑approved, Chase will typically show you a range of possible credit limits and the card options that fit your profile.

chase business credit card pre approval: What You Need to Know

Below are the core components that Chase looks at when deciding whether to give you a pre‑approval:

- Business Revenue & Cash Flow: Consistent monthly income demonstrates repayment ability.

- Personal Credit Score: Since most business cards still require a personal guarantee, a score of 680+ is usually the sweet spot.

- Time in Business: Companies that have operated for at least 12 months are viewed more favorably.

- Existing Relationship with Chase: Having a personal or business checking account, or previous credit products, can boost your odds.

- Debt‑to‑Income Ratio: Lower ratios signal that you’re not over‑leveraged.

Meeting these criteria doesn’t guarantee a pre‑approval, but it puts you in a strong position. If you’re unsure where you stand, a quick review of your personal credit report and a glance at your business financial statements can give you a solid baseline.

How to Request a Pre‑Approval From Chase

The process is straightforward, but a few preparatory steps can smooth the path:

1. Gather Your Business Documentation

Even though a soft pull doesn’t need a full application, having the following on hand will help you answer any follow‑up questions quickly:

- Employer Identification Number (EIN)

- Last two years of tax returns (personal and business)

- Recent bank statements showing cash flow

- Business plan or a brief description of your operations

2. Check Your Personal Credit Score

Use a free credit monitoring service to see where you stand. If you’re below 680, consider taking a few months to improve your score before you hit the pre‑approval button. Paying down revolving balances and correcting any errors on your report are fast wins.

3. Log Into Your Chase Online Account

If you already have a personal account, sign in and navigate to the “Credit Cards” section. Look for the “See If You’re Pre‑Approved” banner. If you’re a new customer, you can still start the process by creating a basic online profile – Chase will ask for minimal personal info before showing you the pre‑approval result.

4. Complete the Soft Pull Form

The form asks for basic details: name, address, SSN (or EIN for the business), and an estimate of annual revenue. Once you submit, the system runs a soft inquiry and instantly displays whether you’re pre‑approved, along with the likely credit limit range.

5. Review Your Options

Chase typically offers a handful of business cards under the pre‑approval umbrella, such as the Chase Ink Business Preferred® Credit Card, Chase Ink Business Unlimited®, and the newer Chase Sapphire Business cards. Each card has a different rewards structure, so pick the one that aligns with your spending patterns.

Choosing the Right Chase Business Card After Pre‑Approval

Not all business cards are created equal. Here’s a quick rundown of the most popular Chase options you might see after a pre‑approval:

- Ink Business Preferred®: 3X points on travel, shipping, internet, and advertising. Great for businesses that spend heavily on marketing.

- Ink Business Unlimited®: 1.5X points on every purchase. Simpler rewards, ideal for diverse spend.

- Sapphire Business Card: Premium travel perks, higher point values on dining and travel. Best for frequent travelers.

When you compare these, think about where your money goes each month. If most of your expenses are fuel and vehicle maintenance, you might even consider pairing a business fuel card (see our Fuel Credit Cards for Small Business: A Complete Guide) with a Chase card to maximize category bonuses.

Tips to Turn Pre‑Approval Into a Full Approval

Getting a pre‑approval is only half the battle. Chase will still run a hard inquiry when you submit the final application, and they’ll verify the details you provided. Here are five proven tactics to improve your odds of moving from pre‑approved to fully approved:

1. Keep Your Credit Utilization Low

Before you apply, aim for a utilization rate under 30 %. Paying down existing balances on personal cards shows lenders you can manage revolving credit responsibly.

2. Strengthen the Business Banking Relationship

If you already have a Chase business checking or savings account, keep a healthy balance and consider setting up recurring deposits. A robust banking relationship can serve as an informal endorsement.

3. Highlight Consistent Revenue

When you fill out the final application, attach a recent profit and loss statement that illustrates steady or growing revenue. A clear upward trend reassures the underwriter.

4. Provide a Personal Guarantee with Confidence

Most Chase business cards require a personal guarantee, meaning you’re personally liable for the debt. If you have strong personal credit and can comfortably back the business, make that clear in the application notes.

5. Use the Right Timing

Applying shortly after a major credit‑worthy event—like a successful loan payoff or a substantial increase in business income—can improve your profile. Avoid applying during a dip in cash flow.

Benefits of a Chase Business Credit Card

Beyond the immediate credit line, Chase business cards bring a suite of perks that can translate into real savings:

- Sign‑up Bonuses: Many cards offer 50,000‑100,000 points after meeting a modest spend threshold within the first three months.

- Travel Protections: Trip cancellation insurance, lost luggage coverage, and primary rental car insurance can save you thousands on business trips.

- Expense Management Tools: Integrated online dashboards let you track employee spending, set limits, and download CSV files for accounting software.

- Purchase Protection: Extended warranties and price protection on eligible purchases add an extra layer of security.

These benefits become even more valuable when you pair them with a robust payment processing solution. For instance, our guide on Credit Card Merchant Services for Small Business – A Complete Guide explains how to integrate your Chase card with merchant services to streamline cash flow.

Common Misconceptions About Pre‑Approval

It’s easy to get tangled up in myths surrounding pre‑approval. Let’s clear a few of them:

Myth 1: Pre‑Approval Guarantees a Card

False. Pre‑approval means you’re a strong candidate based on current data, but a hard pull will still be performed. If your financial situation changes drastically between the soft pull and the hard pull, the final decision could differ.

Myth 2: Pre‑Approval Means No Credit Check

Incorrect. A soft pull is still a credit check, just one that doesn’t affect your score. It’s a behind‑the‑scenes look at your creditworthiness.

Myst 3: You Can Get Unlimited Credit

Not true. The pre‑approval will show a range, often $5,000‑$50,000 depending on revenue, credit score, and other factors. The final limit is set after the full application review.

What to Do If You’re Not Pre‑Approved

Being denied a pre‑approval isn’t the end of the road. Here’s how to bounce back:

- Review Your Credit Report: Look for errors or negative items that can be disputed.

- Boost Your Business Revenue: Consider short‑term contracts or new sales channels to increase monthly income.

- Strengthen Your Personal Credit: Pay down existing balances, avoid new hard inquiries, and keep old accounts open.

- Explore Alternative Cards: Other issuers like American Express or Capital One may have lower thresholds for small businesses.

Sometimes, waiting six months and re‑applying after you’ve addressed the weak points yields a better result.

Final Thoughts

Chase’s chase business credit card pre approval process is a handy shortcut for entrepreneurs who want to test the waters before committing to a full application. By understanding the eligibility factors, preparing your documentation, and following the step‑by‑step request flow, you can unlock a credit line that fuels growth, simplifies expense tracking, and adds valuable rewards to your business toolkit.

Remember, a pre‑approval is a promise—not a guarantee. Treat it as a valuable data point, not a final verdict. Strengthen both your personal and business financial profiles, choose the card that aligns with your spend habits, and use the perks wisely. With a bit of patience and strategic planning, that pre‑approved status can quickly turn into a fully funded Chase business credit card that powers your company forward.