Table of Contents

- is discover a good first credit card? Core Benefits That Matter

- is discover a good first credit card? How the Rewards Structure Helps New Users

- Assessing the Drawbacks: When “is discover a good first credit card” Might Not Be the Answer

- How to Leverage Discover as Your First Credit Card Wisely

- 1. Pay Your Balance in Full Every Month

- 2. Activate Quarterly Categories Promptly

- 3. Use the Free FICO Score Tool

- 4. Take Advantage of the Cashback Match

- 5. Keep an Eye on Fees and Penalties

- Comparing Discover to Other First‑Card Options

- Real‑World Experiences: What New Cardholders Say

- Tips for Transitioning from Your First Card to a More Advanced Card

Choosing the very first credit card can feel like stepping onto a tightrope. One wrong move and you could find yourself tangled in high interest rates, hidden fees, or a credit score that never climbs. That’s why many first‑time borrowers spend hours scrolling through offers, comparing rewards, APRs, and the fine print. Among the sea of options, Discover often pops up with its well‑known cash‑back program and a reputation for being consumer‑friendly. But the real question many newcomers ask is: is discover a good first credit card?

In this article we’ll break down the essential features of Discover’s entry‑level cards, weigh the pros and cons, and help you decide if it fits your financial goals. Whether you’re a college student, a recent graduate, or simply someone looking to build credit from scratch, understanding the nuances of Discover’s offerings can save you time, money, and stress.

We’ll also sprinkle in some practical tips on how to use your new card responsibly, avoid common pitfalls, and make the most of the rewards program. By the end, you’ll have a clear picture of whether the answer to “is discover a good first credit card” is a confident “yes,” a cautious “maybe,” or a gentle “look elsewhere.”

is discover a good first credit card? Core Benefits That Matter

Discover’s flagship card, the Discover it® Cash Back, is often touted as a go‑to for beginners. Here’s why many financial advisors and seasoned users consider it a solid starter card:

- Zero annual fee: No hidden yearly costs means every dollar you earn stays in your pocket.

- Cash‑back matching: For new cardholders, Discover doubles all cash‑back earned in the first year – a sweet boost for anyone just starting to build credit.

- Flexible rewards categories: Every quarter, you can earn 5% cash back on rotating categories like groceries, gas, or online shopping (up to a $1,500 limit).

- Upright APR: While the standard APR ranges from 13.99% to 23.99%, Discover often provides an introductory 0% APR on purchases for the first 14 months for qualifying applicants.

- Robust security: Free alerts, a virtual card number for online purchases, and no foreign transaction fees make it safe for both domestic and occasional international use.

is discover a good first credit card? How the Rewards Structure Helps New Users

The cash‑back matching program is a standout feature for newcomers. Imagine you spend $500 on groceries in your first quarter; you’d normally earn $25 (5% of $500). Discover then matches that amount, giving you $50 cash back – effectively a 10% return on that spending. This boost can be especially motivating for students or recent graduates who are learning to manage a budget.

Beyond cash back, Discover offers a comprehensive online account portal that makes tracking purchases and payments a breeze. The mobile app sends real‑time notifications, helping you stay on top of spending and avoid accidental over‑limits – a common mistake among first‑time cardholders.

Assessing the Drawbacks: When “is discover a good first credit card” Might Not Be the Answer

No credit card is perfect, and Discover is no exception. Here are a few considerations that could sway your decision:

- Limited acceptance abroad: While Discover is widely accepted in the U.S., its merchant network overseas is smaller compared to Visa or Mastercard. Frequent travelers might face inconvenience.

- Higher standard APR: If you carry a balance beyond the introductory period, the APR can be on the higher side, potentially eroding the value of cash‑back rewards.

- Rotating categories require attention: To maximize the 5% cash‑back, you must activate new categories each quarter. Forgetting to do so can reduce the card’s effective rewards.

- Credit limit caps for new users: Initial credit limits may be modest (often $500–$1,000), which can affect your credit utilization ratio if you have larger spending needs.

If any of these points raise red flags for you, it might be worth exploring alternatives like a secured Visa or Mastercard that enjoy broader international acceptance. However, for most domestic, everyday spenders, the benefits often outweigh the downsides.

How to Leverage Discover as Your First Credit Card Wisely

Assuming you’ve decided that is discover a good first credit card for you, the next step is to use it strategically. Below are actionable steps that can set you up for credit success:

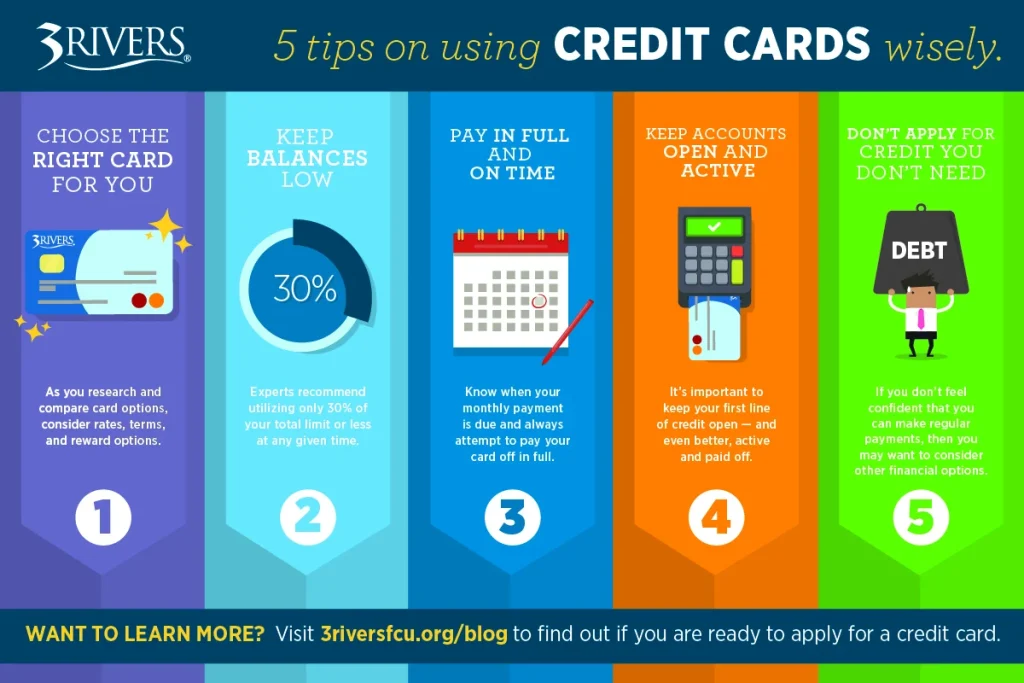

1. Pay Your Balance in Full Every Month

Even with a low introductory APR, interest charges can quickly negate cash‑back earnings. By paying the full statement balance before the due date, you avoid interest altogether and keep your credit utilization low – both crucial for a healthy credit score.

2. Activate Quarterly Categories Promptly

Log into your Discover account at the start of each quarter and enable the 5% cash‑back categories that align with your spending habits. Set a calendar reminder so you never miss the activation window.

3. Use the Free FICO Score Tool

Discover provides a free FICO Score that updates monthly. Monitoring this score can help you gauge how your new card affects your credit health, allowing you to adjust usage patterns as needed.

4. Take Advantage of the Cashback Match

Plan larger purchases (like back‑to‑school supplies) early in the first year to maximize the cash‑back match. The more you spend on eligible categories, the larger the match amount you’ll receive at year‑end.

5. Keep an Eye on Fees and Penalties

While there’s no annual fee, late payment fees ($40) and over‑limit fees (if you opt in) can appear. Set up automatic payments for at least the minimum due to avoid these extra costs.

Comparing Discover to Other First‑Card Options

It’s helpful to see how Discover stacks up against other popular starter cards. Below is a quick snapshot:

| Feature | Discover it® Cash Back | Capital One Quicksilver | Chase Freedom Flex |

|---|---|---|---|

| Annual Fee | $0 | $0 | $0 |

| Intro APR (Purchases) | 0% 14 months | 0% 15 months | 0% 15 months |

| Cash‑Back Rate | 5% quarterly (capped) + 1% standard | 1.5% flat | 5% quarterly + 1% standard |

| Cash‑Back Match | Yes, first year | No | No |

| Foreign Transaction Fees | None | None | None |

| International Acceptance | Moderate | Wide (Visa network) | Wide (Visa network) |

From this comparison, Discover stands out for its cash‑back match and strong domestic rewards, while Visa‑based cards may win for global acceptance. Your personal travel habits and spending patterns will dictate which edge matters most.

Real‑World Experiences: What New Cardholders Say

Feedback from first‑time users often highlights two recurring themes: ease of use and the excitement of seeing cash‑back appear on the statement. One college sophomore shared, “I opened the Discover it® after reading about the cash‑back match. By the end of the first year, I earned $120 in rewards—more than I expected from a card I barely used.”

Conversely, another new cardholder noted, “I wish Discover accepted more places when I traveled to Europe. I had to carry a backup Visa card for a few weeks.” This anecdote underscores the importance of evaluating the “is discover a good first credit card” question in light of your own travel frequency.

Tips for Transitioning from Your First Card to a More Advanced Card

Once you’ve built a solid credit history (usually after 6‑12 months of on‑time payments and low utilization), you might consider upgrading to a card with higher rewards or travel perks. Here’s how to make that move smoothly:

- Check your credit score: Aim for at least a 680 FICO score before applying for premium cards.

- Maintain low utilization: Keep balances under 30% of your total credit limit across all cards.

- Leverage pre‑approval tools: Many issuers, including Discover, provide pre‑approval checks that won’t affect your credit. For a deeper dive on pre‑approval strategies, see the guide on Chase Business Credit Card Pre Approval – How to Get It & Why It Matters.

- Plan the timing: Apply for a new card after your current statement closes to minimize hard inquiries.

By following these steps, you can transition from a starter card like Discover to a higher‑tier card without jeopardizing the credit foundation you’ve built.

In summary, the question is discover a good first credit card largely depends on your personal circumstances, but for many U.S. residents looking for a fee‑free card with generous introductory rewards, the answer leans toward a confident “yes.” Its cash‑back match, user‑friendly portal, and lack of annual fees make it a compelling entry point into the world of credit. Just stay mindful of the rotating categories, keep an eye on the APR after the intro period, and use the built‑in tools to monitor your credit health.

As you embark on your credit‑building journey, remember that the first card is only the beginning. Treat it as a learning tool, pay on time, and you’ll set the stage for more sophisticated financial products down the line.