Table of Contents

- is discover a good credit card? A comprehensive evaluation

- Rewards program and cash‑back rates

- Fees and interest rates

- Credit score requirements and approval odds

- Customer service and security features

- How Discover stacks up against other popular cards

- Discover vs. Chase Freedom Flex

- Discover vs. Citi Double Cash

- Discover as a first credit card

- Practical tips to get the most out of your Discover card

- Activate the cash‑back match

- Pay balances in full

- Monitor your credit score

- Leverage no foreign transaction fees

- Potential drawbacks to consider

- Limited acceptance outside the U.S.

- Rotating categories require attention

- APR can be higher than some competitors

- Bottom line: Should you pick Discover?

When you start thinking about adding a credit card to your wallet, the market can feel overwhelming. From cash‑back giants to travel‑focused powerhouses, each card promises something slightly different. Amid this sea of options, the question that often pops up is simple yet crucial: is discover a good credit card for your needs?

In this article we’ll walk through the key features of Discover cards, compare them to competitors, and help you decide if they fit your financial goals. Whether you’re a first‑time cardholder looking for a friendly introduction to credit or a seasoned spender hunting for solid cash‑back, you’ll find the details you need.

We’ll also sprinkle in some practical tips—like how your credit score influences approval odds and what hidden fees to watch for—so you can make a well‑rounded decision without the guesswork.

is discover a good credit card? A comprehensive evaluation

Discover isn’t just another name on the credit‑card aisle; it’s a brand that has built a reputation around transparent fees, generous rewards, and customer‑centric service. Below we break down the most important aspects that answer the core question.

Rewards program and cash‑back rates

One of the standout features of Discover cards is the cash‑back match for new cardmembers. In many cases, Discover will double your cash back earned in the first year, up to $500. This “first‑year match” effectively turns a 5% cash‑back rate on rotating categories into a 10% boost—an enticing perk for anyone asking, “is discover a good credit card for cash‑back?”

- 5% rotating categories: Each quarter, Discover highlights a set of categories (e.g., grocery stores, gas stations, restaurants) where you earn 5% cash back on up to $1,500 in purchases.

- 1% everyday purchases: Anything that doesn’t fall into the rotating categories automatically earns 1% cash back.

- No caps after the first year: Once the match period ends, you still keep the 5%/1% structure, which remains competitive against many flat‑rate cards.

Fees and interest rates

When evaluating “is discover a good credit card” you inevitably look at the fee structure. Discover’s approach is refreshingly simple:

- No annual fee: Most Discover cards, including the popular Discover it® Cash Back, come with zero annual cost.

- Foreign transaction fees: For travelers, Discover does not charge foreign transaction fees—a rarity among U.S. issuers.

- APR range: Variable APRs typically sit between 13% and 24% depending on creditworthiness. While not the lowest in the market, the absence of hidden fees balances the equation for many users.

Credit score requirements and approval odds

For many readers, the underlying question is not just “is discover a good credit card,” but also “will I qualify?” Discover tends to be more flexible than premium travel cards, often approving applicants with a good (690‑749) or even fair (630‑689) credit score. If you’re unsure where you stand, check out our guide on credit score required for Citi Simplicity Card for a benchmark on similar credit‑score thresholds.

Customer service and security features

Discover consistently ranks high in customer satisfaction surveys. Their 24/7 phone support, free Social Security number alerts, and “freeze it” feature let you lock your card instantly via the mobile app. These tools reinforce the perception that is discover a good credit card when you value responsive service and strong security.

How Discover stacks up against other popular cards

To truly answer the central question, let’s compare Discover to a few other cards that often vie for the same audience.

Discover vs. Chase Freedom Flex

Both cards offer rotating 5% categories, but Chase adds a 3% on dining and drugstores year‑round, plus a 1% base rate. However, Chase charges a $0 annual fee but does not match cash back in the first year. If the “cash‑back match” is a decisive factor for you—i.e., “is discover a good credit card for maximizing early rewards”—Discover takes the lead.

Discover vs. Citi Double Cash

The Citi Double Cash card provides a flat 2% cash back (1% on purchase, 1% on payment). It’s simple, but lacks the quarterly 5% boost and the first‑year match that make Discover stand out for those who enjoy rotating categories. If you prefer a set‑and‑forget approach, Citi may suit you, but for maximizing cash back across varied spending, Discover often wins.

Discover as a first credit card

Many first‑time borrowers ask, “is discover a good credit card for beginners?” The answer is a resounding yes for several reasons:

- Zero annual fee reduces the risk of unnecessary costs.

- The cash‑back match provides an early “win” that encourages responsible use.

- Tools like free credit score monitoring help new users track progress.

For a deeper dive into this specific scenario, check out our article Is Discover a Good First Credit Card? An In‑Depth Look.

Practical tips to get the most out of your Discover card

Even if you’ve decided that is discover a good credit card for you, using it wisely maximizes benefits and protects your credit health.

Activate the cash‑back match

Make sure you register your new Discover card within the first 90 days to claim the match. Then, focus on hitting the $1,500 quarterly spend cap on the 5% categories to fully leverage the boost.

Pay balances in full

Since Discover’s APR can climb into the mid‑20s, avoid interest charges by paying the statement balance each month. Setting up automatic payments for the full amount can simplify this habit.

Monitor your credit score

Discover offers a free FICO® Score on your monthly statement and through the app. Use this tool to watch how your utilization ratio (ideally below 30%) and payment history affect your score over time.

Leverage no foreign transaction fees

If you travel abroad, use your Discover card for purchases to avoid the typical 3%‑5% foreign fees other cards impose. This can be a decisive factor for frequent travelers asking, “is discover a good credit card for overseas spending?”

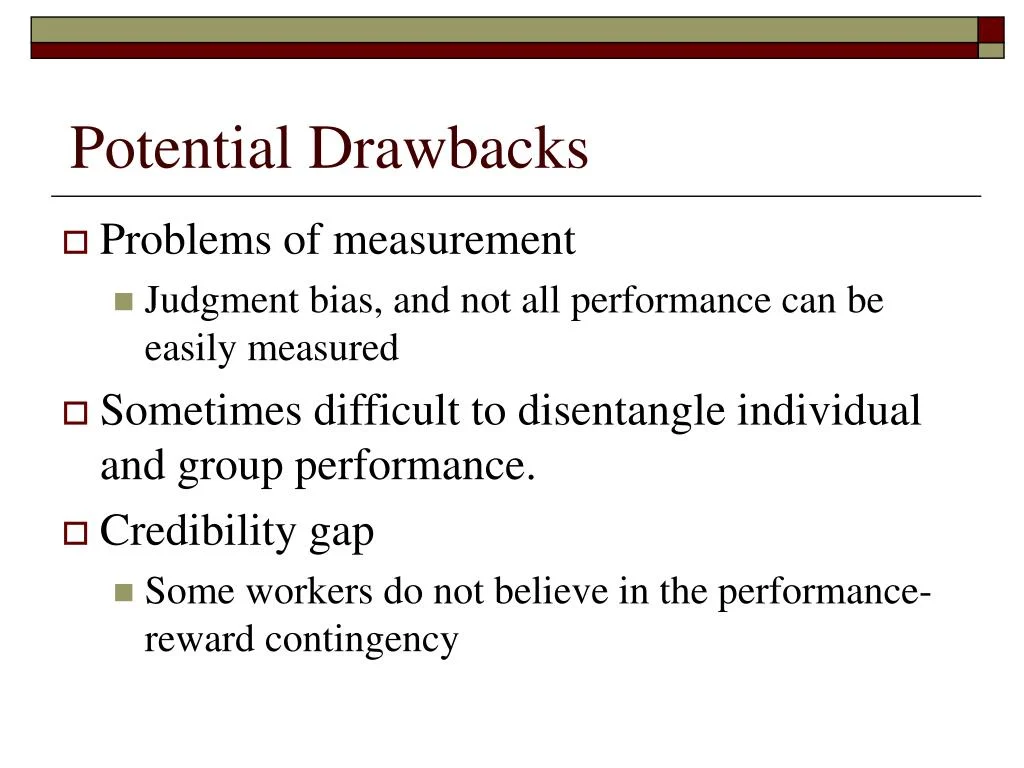

Potential drawbacks to consider

No card is perfect, and it’s important to weigh the cons alongside the pros when answering the main question.

Limited acceptance outside the U.S.

While Discover has expanded its network, it’s still accepted at fewer merchants internationally compared to Visa or Mastercard. If you travel to regions where Discover isn’t widely used, you might need a backup card.

Rotating categories require attention

The 5% categories change every quarter, and you must activate them in your online account to earn the higher rate. Forgetting to do so can mean you earn only the base 1% on purchases you assumed would be 5%.

APR can be higher than some competitors

If you tend to carry a balance, a card with a lower APR—like a balance‑transfer offer from a different issuer—might be more cost‑effective. Discover’s strength lies in rewards and fee‑friendliness rather than low‑interest financing.

Bottom line: Should you pick Discover?

After dissecting rewards, fees, credit impact, and user experience, the answer to “is discover a good credit card” largely depends on your personal spending habits and credit goals.

If you value a straightforward cash‑back program, love the idea of a first‑year match, and appreciate a no‑annual‑fee card with solid customer service, Discover is an excellent choice. It shines for new cardholders, travelers who avoid foreign fees, and anyone who enjoys the occasional quarterly bonus.

Conversely, if you need a card accepted worldwide without the occasional “I’m sorry, we don’t take Discover” at foreign merchants, or you carry a balance and need the lowest possible APR, you might look elsewhere.

Ultimately, the decision hinges on matching the card’s strengths to your lifestyle. By understanding the nuances laid out here, you can confidently answer the question for yourself and move forward with a credit card that supports your financial journey.

Ready to explore the full details? Dive into our Discover Credit Card Is It Good? Full Review & Insights for an even deeper look at numbers, user experiences, and side‑by‑side comparisons.

Happy card hunting, and may your cash‑back be plentiful!