Table of Contents

- Why You Should Process Credit Cards Online for Small Business

- Understanding the Core Components of Online Card Processing

- Step‑by‑Step Guide to Process Credit Cards Online for Small Business

- Choosing the Right Payment Gateway: What to Look For

- Keeping Transactions Secure: PCI‑DSS and Beyond

- Common Security Mistakes to Avoid When You Process Credit Cards Online for Small Business

- Understanding Fees: What You’ll Pay When You Process Credit Cards Online for Small Business

- Integrating Card Processing Into Your Existing Workflow

- Boosting Sales with Smart Payment Features

- Handling Chargebacks and Disputes Effectively

- Future Trends: What’s Next for Online Card Processing?

Running a small business today means you can’t afford to turn away customers who prefer to pay with a card. Whether you’re a boutique coffee shop, a freelance designer, or an e‑commerce store, the ability to process credit cards online for small business is no longer a luxury—it’s a necessity. But diving into the world of digital payments can feel overwhelming, especially when you’re juggling inventory, marketing, and day‑to‑day operations.

In this article we’ll break down the entire process, from the basics of how a transaction works to the nitty‑gritty of choosing a payment gateway, keeping data safe, and optimizing costs. You’ll walk away with a clear roadmap that lets you set up online card processing quickly, avoid common pitfalls, and keep both your customers and your bottom line happy.

Think of this as your cheat sheet for turning a simple “tap or swipe” into a smooth, revenue‑generating experience. Ready to get started? Let’s dive in.

Why You Should Process Credit Cards Online for Small Business

First, let’s talk about the “why.” Customers expect flexibility. According to recent surveys, over 70 % of shoppers abandon a purchase if they can’t pay with a card. By offering online credit card processing, you:

- Expand your market reach beyond foot traffic.

- Accelerate cash flow with faster settlement times.

- Reduce the friction that often leads to abandoned carts.

- Gain valuable data on purchasing patterns for smarter marketing.

All of these benefits translate into higher revenue, which is exactly what every small business owner is aiming for.

Understanding the Core Components of Online Card Processing

Before you sign any contracts, it helps to know the moving parts that make up the ecosystem for processing credit cards online for small business:

- Payment Gateway: The technology that securely transmits card data from your website or app to the acquiring bank.

- Merchant Account (Acquiring Bank): The account where funds are deposited after the transaction is approved.

- Payment Processor: The service that handles the communication between the gateway, card networks (Visa, MasterCard, etc.), and the acquiring bank.

- PCI‑DSS Compliance: A set of security standards that protect cardholder data.

Think of the gateway as the front desk, the processor as the back‑office clerk, and the merchant account as the cash register where the money lands.

Step‑by‑Step Guide to Process Credit Cards Online for Small Business

- Assess Your Business Needs: Do you need a simple “Buy Now” button, a full shopping cart, or recurring billing? Your answer will shape the gateway you choose.

- Choose a Payment Gateway: Look for features like easy integration, transparent pricing, and solid customer support. Popular options for small businesses include Stripe, Square, and PayPal.

- Set Up a Merchant Account: Some gateways bundle this service (Stripe does), while others require a separate acquiring bank. Compare fees and settlement times.

- Integrate the Gateway: Use plugins for platforms like Shopify, WooCommerce, or custom APIs if you have a developer on hand.

- Test Transactions: Run a few test payments in sandbox mode to ensure everything works smoothly before you go live.

- Go Live and Monitor: Once live, keep an eye on transaction reports, chargeback alerts, and customer feedback.

If you’re looking for a deeper dive into each of these stages, the online credit card processing guide walks you through real‑world examples and screenshots.

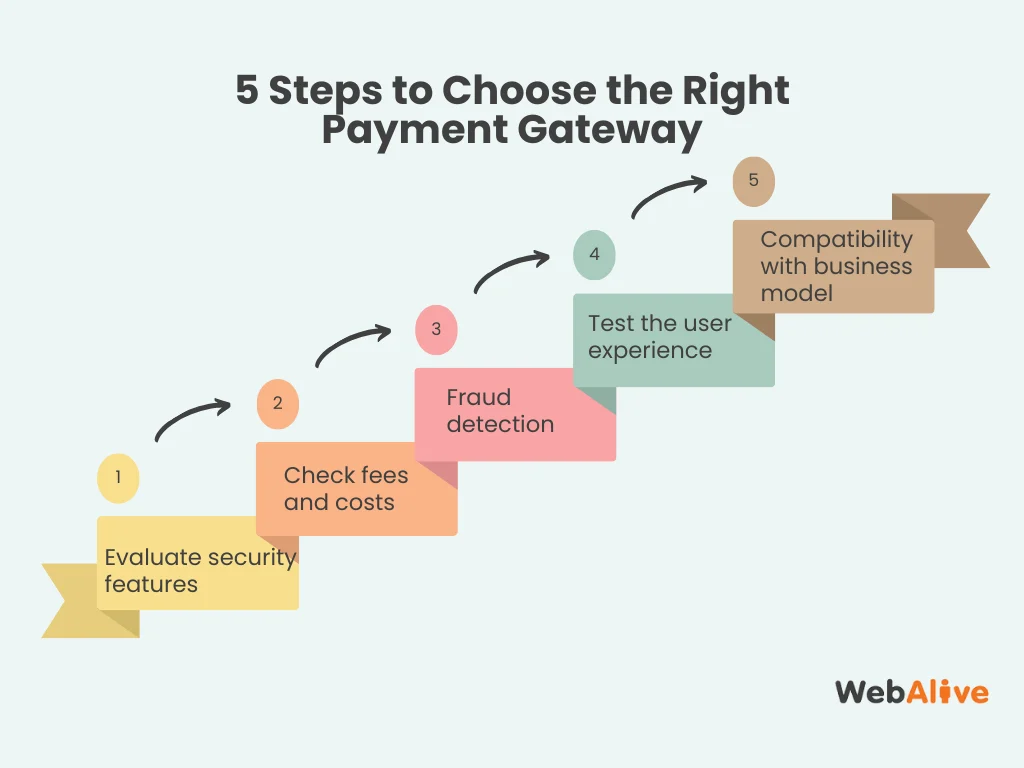

Choosing the Right Payment Gateway: What to Look For

Not all gateways are created equal, and picking the wrong one can eat into your profits with hidden fees or cause headaches with poor integration. Here’s a quick checklist to keep handy while you compare options:

- Pricing Structure: Look for transparent transaction fees (e.g., 2.9 % + 30¢) and beware of monthly minimums.

- Integration Ease: Does the gateway provide a ready‑made plugin for your platform? If you need a custom solution, check the quality of the API documentation.

- Security Features: Tokenization, 3‑D Secure, and built‑in fraud detection can lower your risk.

- Settlement Speed: Some processors deposit funds in 24 hours, while others take up to 5 business days.

- Customer Support: A responsive support team can be a lifesaver when you face a sudden payment glitch.

For a practical comparison of top providers, the Credit Card Processing Online for Small Business: A Practical Guide offers side‑by‑side tables that simplify the decision‑making process.

Keeping Transactions Secure: PCI‑DSS and Beyond

Security is a non‑negotiable part of the journey to process credit cards online for small business. Failure to comply with PCI‑DSS can result in hefty fines and loss of customer trust. Here are the basics you need to master:

- Tokenization: Replaces the card number with a random token, so the sensitive data never touches your servers.

- End‑to‑End Encryption (E2EE): Encrypts data from the moment it’s entered until it reaches the processor.

- 3‑D Secure (Verified by Visa, MasterCard SecureCode): Adds an extra authentication step for the cardholder, reducing fraud.

- Regular Vulnerability Scans: Conduct quarterly scans to identify any weak points in your system.

Many modern gateways (Stripe, Square) handle tokenization and E2EE for you, meaning you can stay PCI‑DSS compliant with minimal technical overhead.

Common Security Mistakes to Avoid When You Process Credit Cards Online for Small Business

- Storing raw card numbers on your servers.

- Using outdated SSL certificates.

- Neglecting software updates for your e‑commerce platform.

- Overlooking multi‑factor authentication for admin accounts.

By fixing these issues early, you’ll protect both your brand and your customers’ wallets.

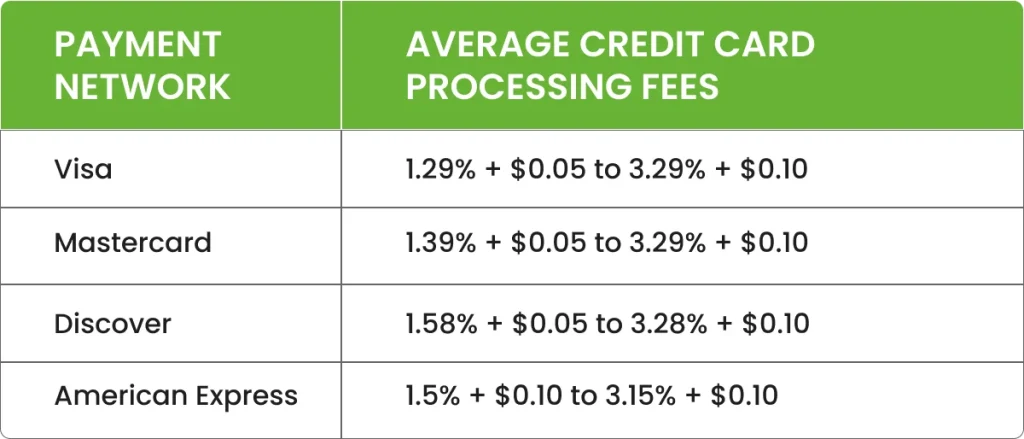

Understanding Fees: What You’ll Pay When You Process Credit Cards Online for Small Business

Fees can be the most confusing part of the equation. Below is a quick breakdown of the most common charges you’ll encounter:

- Transaction Fee: Usually a percentage of the sale plus a fixed amount (e.g., 2.9 % + 30¢).

- Monthly Gateway Fee: Some providers charge a flat monthly fee for access to the platform.

- Chargeback Fee: If a customer disputes a charge, you’ll pay a fee (typically $15‑$25) per dispute.

- Refund Fee: Most processors keep the original transaction fee even when you refund a sale.

To keep costs under control, regularly audit your statements, negotiate rates once your volume grows, and consider a flat‑rate pricing model if you have high‑ticket items.

Integrating Card Processing Into Your Existing Workflow

Now that you understand the technical and financial landscape, the next step is seamless integration. Here’s how you can embed payment processing without disrupting your day‑to‑day operations:

- Use Platform Plugins: If you run on Shopify, WooCommerce, or Squarespace, install the official gateway plugin and configure it in minutes.

- Leverage Hosted Checkout Pages: Redirect customers to a secure, PCI‑compliant page hosted by the gateway (ideal for small teams without dev resources).

- Custom API Integration: For unique checkout experiences, hire a developer to connect directly to the gateway’s API.

Whichever route you choose, always run a few real‑world test orders before announcing the new payment option to your customers.

Boosting Sales with Smart Payment Features

Processing credit cards online for small business isn’t just about acceptance; it’s also about conversion. Add these features to turn a simple payment into a revenue‑boosting opportunity:

- One‑Click Checkout: Store tokenized cards for returning customers, reducing friction on repeat purchases.

- Saved Cards & Subscriptions: Perfect for service‑based businesses that bill monthly.

- Dynamic Currency Conversion: Let international shoppers pay in their local currency, increasing trust.

- Instant Payment Confirmation Emails: Builds confidence and reduces post‑purchase support tickets.

These enhancements not only improve the customer experience but also provide valuable data for future marketing campaigns.

Handling Chargebacks and Disputes Effectively

Even with the best security, chargebacks happen. When you process credit cards online for small business, a proactive strategy can minimize loss:

- Collect Detailed Receipts: Include product description, price, and contact info on every invoice.

- Use Fraud Detection Tools: Leverage the gateway’s built‑in risk scoring.

- Respond Promptly: Most processors give you 7‑10 days to submit evidence. Delays can lead to automatic loss.

- Monitor Trends: High chargeback rates can trigger higher fees or account termination.

By staying organized and responding quickly, you protect both your revenue and your reputation.

Future Trends: What’s Next for Online Card Processing?

The payment landscape evolves fast. Here are a few trends that small businesses should keep an eye on:

- Buy‑Now‑Pay‑Later (BNPL): Services like Klarna and Afterpay are becoming mainstream, offering customers flexible financing.

- Contactless Mobile Wallets: Apple Pay, Google Pay, and Samsung Pay are gaining market share, especially among younger shoppers.

- Cryptocurrency Payments: While still niche, some gateways now let you accept Bitcoin or stablecoins.

- AI‑Driven Fraud Prevention: Machine‑learning models that adapt to new fraud patterns in real time.

Staying adaptable and experimenting with these options can give your business a competitive edge as consumer preferences shift.

In the end, the ability to process credit cards online for small business is a blend of choosing the right partners, securing the transaction flow, and constantly optimizing costs and user experience. With the steps outlined above, you’re well equipped to launch a reliable payment system that fuels growth rather than hinders it. Remember, the journey doesn’t stop at “live”—regularly review your statements, update security settings, and explore new features to keep your checkout smooth and profitable.