Table of Contents

- chase ink business cash credit card: Overview and Core Benefits

- How the Reward Structure Works in Real‑World Scenarios

- Scenario 1: Office‑Supply Heavy Business

- Scenario 2: Service‑Heavy Business

- Scenario 3: Mixed Spend Business

- Eligibility and Application Tips for the chase ink business cash credit card

- chase ink business cash credit card: Eligibility Requirements

- Fees, APR, and Other Costs

- Maximizing Cash Back: Strategies & Pro Tips

- Consolidate Office‑Supply Purchases

- Bundle Telecom Services

- Leverage Employee Cards Wisely

- Combine with Chase’s “Ultimate Rewards” Portal

- Cash‑Back Redemption Options

- How It Stacks Up Against Competitors

- Real‑World User Experiences

- Application Process: Step‑by‑Step

- Potential Drawbacks to Consider

- Integrating the Card with Your Business Accounting

- What Happens If You Miss a Payment?

- Renewal and Ongoing Management

Running a small business means juggling a million tasks at once, and every dollar you keep in the bank can make a big difference. That’s why many entrepreneurs are constantly on the hunt for financial tools that not only simplify expenses but also give back. Enter the Chase Ink Business Cash Credit Card, a card that promises generous cash‑back rewards, low fees, and a suite of perks tailored for business owners. In this deep dive, we’ll walk through what makes this card tick, who it’s best suited for, and how you can squeeze the most out of its reward structure.

Whether you’re a freelancer managing client meals, a retail shop restocking inventory, or a tech startup paying for software subscriptions, the right credit card can turn ordinary spending into a steady stream of cash back. The Chase Ink Business Cash Credit Card positions itself as a middle‑ground option—offering more rewards than a basic corporate card, but without the high annual fee that often comes with premium cards. Let’s unpack the details and see if it lives up to the hype.

Before we jump into the nitty‑gritty, it’s worth noting that this card sits comfortably within Chase’s broader Ink suite, which includes the Ink Business Preferred and Ink Business Unlimited cards. Each serves a different business profile, but the Ink Business Cash card shines for those who want solid cash‑back on everyday purchases without paying an annual fee.

chase ink business cash credit card: Overview and Core Benefits

The Chase Ink Business Cash Credit Card is designed with a straightforward cash‑back model. Here are the headline features:

- Earn Rate: 5% cash back on the first $25,000 spent each year on combined purchases at office supply stores and on internet, cable, and phone services.

- 3% cash back on the first $25,000 spent each year at gas stations and restaurants.

- 1% cash back on all other purchases.

- Annual Fee: $0.

- Intro APR: 0% for the first 12 months on purchases (variable APR after).

- Free employee cards with customizable spending limits.

- Access to Chase’s powerful online dashboard and expense‑tracking tools.

These rates make the card a strong contender for businesses that have recurring office‑supply needs or rely heavily on telecommunications—think a design studio buying ink cartridges or a consulting firm paying for broadband.

How the Reward Structure Works in Real‑World Scenarios

Understanding the reward tiers is essential to maximizing cash back. Let’s break down a few typical monthly expense patterns:

Scenario 1: Office‑Supply Heavy Business

If you spend $2,000 a month at Office Depot, Staples, or a similar vendor, you’ll earn 5% cash back, translating to $100 per month or $1,200 annually. That’s a tidy chunk of cash that can be reinvested into inventory or marketing.

Scenario 2: Service‑Heavy Business

For a business that spends $1,500 monthly on internet, phone, and cable, the 5% rate also applies, yielding $75 cash back each month.

Scenario 3: Mixed Spend Business

A boutique that spends $800 on gas for deliveries, $600 on meals with clients, and $600 on miscellaneous purchases will earn:

- 3% on $800 gas = $24

- 3% on $600 meals = $18

- 1% on $600 other = $6

Total cash back for that month: $48, or $576 annually—a respectable sum for a small operation.

Eligibility and Application Tips for the chase ink business cash credit card

Before you apply, make sure you meet the basic criteria. While Chase doesn’t publicly list a strict credit score threshold, successful applicants typically have a personal credit score of 680 or higher and a solid business credit profile.

chase ink business cash credit card: Eligibility Requirements

- Business Structure: Available to corporations, LLCs, partnerships, and sole proprietorships.

- Revenue: No explicit minimum, but a steady cash flow helps demonstrate the ability to repay.

- Personal Credit: A good to excellent personal credit score improves approval odds.

- U.S. Presence: Must have a U.S. address and a Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN).

Tip: If your personal credit isn’t perfect, consider bolstering it before applying. Paying down existing balances, correcting any errors on your credit report, and limiting new credit inquiries can all help.

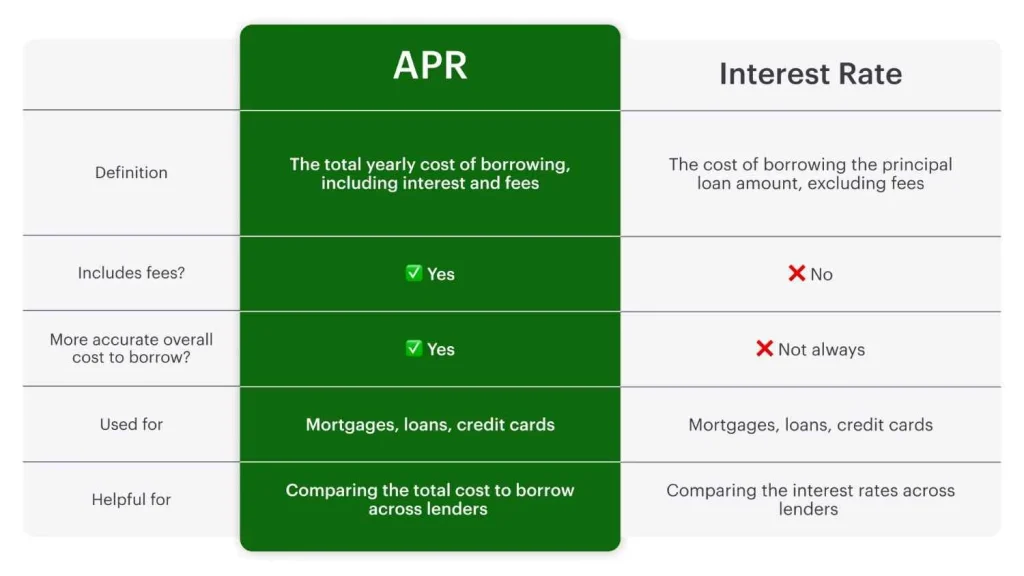

Fees, APR, and Other Costs

One of the card’s biggest draws is its $0 annual fee, which means every cash‑back dollar truly stays in your pocket. However, you should still be aware of other potential costs:

- Late Payment Fee: Up to $40.

- Foreign Transaction Fee: 3% on purchases made outside the U.S.

- Balance Transfer Fee: Either $5 or 5% of the transferred amount, whichever is greater.

- APR: Variable 13.99% – 23.99% based on creditworthiness.

Keeping an eye on these fees, especially the foreign transaction fee, can prevent surprise expenses when you travel for business.

Maximizing Cash Back: Strategies & Pro Tips

Even with solid base rates, savvy entrepreneurs can push their earnings higher by aligning spending patterns with the card’s sweet spots. Here are some actionable tips:

Consolidate Office‑Supply Purchases

Instead of spreading orders across multiple vendors, channel all office‑supply purchases through a single retailer that qualifies for the 5% rate. This ensures you stay under the $25,000 cap while capturing the maximum cash back.

Bundle Telecom Services

If you have separate contracts for internet, phone, and cable, see if you can negotiate a bundled package. Not only can you save on monthly fees, but you also keep the entire spend in one line item, feeding the 5% cash‑back tier.

Leverage Employee Cards Wisely

Give employees cards for travel and client meals. Since the card offers 3% cash back on gas and restaurants, this can generate a steady flow of rewards. Just set clear spending limits to avoid runaway expenses.

Combine with Chase’s “Ultimate Rewards” Portal

Even though the Ink Business Cash card earns cash back, you can still redeem points earned via other Chase cards for travel or gift cards through the Ultimate Rewards portal, effectively increasing your overall reward value.

Cash‑Back Redemption Options

Cash back earned with the Chase Ink Business Cash Credit Card is automatically deposited into your Chase account as a statement credit, or you can opt to receive it as a direct deposit to a checking or savings account. The flexibility means you can use the funds immediately for inventory, payroll, or any other business need.

How It Stacks Up Against Competitors

When comparing the chase ink business cash credit card to other business cash‑back cards on the market, a few key differentiators emerge:

- American Express Blue Business Cash™ Card: Offers 2% cash back on all purchases up to $50,000 per year, then 1%. No annual fee, but the reward rate is lower on high‑spend categories.

- Capital One Spark Cash Select: Flat 1.5% cash back on everything, with a $0 annual fee. Simpler, but doesn’t match the 5% spikes for office supplies and telecom.

- CitiBusiness/AAdvantage Platinum Select Mastercard: 2% on eligible purchases, with travel perks. Higher annual fee and lower cash‑back potential for core business spend.

Overall, the Ink Business Cash card wins for businesses that can concentrate spending in its high‑cash‑back categories.

Real‑World User Experiences

Many small‑business owners share positive feedback about the card’s simplicity and lack of an annual fee. A boutique marketing firm reported earning over $1,000 in cash back during its first year, mainly from office supplies and client lunches. Conversely, a freelancer who rarely spent on the qualifying categories found the 1% base rate less compelling than a flat‑rate 2% card.

If you’re curious about deeper insights, check out the Business Credit Card for Small Businesses – A Complete Guide for broader comparisons and decision‑making tips.

Application Process: Step‑by‑Step

Applying for the chase ink business cash credit card is a straightforward online process:

- Visit Chase’s official website and navigate to the Ink Business Cash card page.

- Click “Apply Now” and fill out business information, including legal name, address, and EIN (Employer Identification Number).

- Provide personal details for the primary applicant—SSN, income, and housing costs.

- Review and submit supporting documents if requested (e.g., recent bank statements).

- Await instant decision or a follow‑up call; most approvals happen within minutes.

Remember to have your business financials handy; a quick look at recent cash flow statements can streamline verification.

Potential Drawbacks to Consider

No product is perfect. Here are a few caveats to keep in mind:

- Spending Cap on High‑Rate Categories: The 5% cash back is limited to $25,000 per year across office supplies and telecom. Once you hit that ceiling, the rate drops to 1%.

- Variable APR: If you carry a balance, interest charges can erode reward gains.

- No Travel Perks: Unlike the Ink Business Preferred, this card doesn’t offer travel insurance or airport lounge access.

If your business spends heavily beyond the capped categories or you travel frequently, you might explore the Ink Business Preferred or another travel‑focused card.

Integrating the Card with Your Business Accounting

One of the underrated benefits of the Chase Ink suite is its integration with popular accounting software like QuickBooks and Xero. By linking your chase ink business cash credit card to these platforms, you can automatically import transactions, categorize expenses, and generate reports—saving time and reducing manual entry errors.

For businesses that still process payments manually, consider reading our Credit Card Processing Services for Small Business – A Complete Guide to understand how to streamline payment acceptance and reconcile statements efficiently.

What Happens If You Miss a Payment?

Missing a payment triggers a late fee and potentially raises your APR. Chase typically offers a 30‑day grace period, but it’s best to set up automatic payments to avoid any slip‑ups. If you anticipate cash‑flow issues, contact Chase’s customer service early—they may be able to arrange a temporary payment plan.

Renewal and Ongoing Management

Since the Ink Business Cash card carries a $0 annual fee, there’s no renewal cost to worry about. However, keep an eye on the yearly spending cap. At the start of each calendar year, the 5% and 3% categories reset, giving you a fresh opportunity to maximize cash back again.

Also, periodically review your spending patterns. If your business evolves—say, you start spending more on travel—you might want to consider adding another Chase Ink card (like the Ink Business Preferred) to capture travel rewards while keeping the Cash card for everyday expenses.

In short, the chase ink business cash credit card can be a powerful cash‑back engine for the right kind of business. Its zero annual fee, high‑rate categories, and integration with Chase’s digital tools make it a compelling choice for small‑to‑mid‑size firms that have predictable office‑supply and telecom expenses.

Ready to take the next step? Apply online, set up your employee cards, and start watching the cash‑back roll in. And if you’re curious about other options that offer instant funding, the Business Credit Cards with Instant Approval: Fast Funding for Your Company guide can help you compare alternatives.

Ultimately, the best credit card is the one that aligns with your business’s spending habits, cash‑flow needs, and growth plans. With thoughtful use, the Chase Ink Business Cash Credit Card can become a silent profit booster—turning routine purchases into a steady stream of cash that fuels further success.