Table of Contents

- credit card processing companies for small business: What to Look For

- Choosing the right credit card processing companies for small business

- Top Credit Card Processing Companies for Small Business in 2024

- Square

- Stripe

- PayPal Zettle

- Helcim

- Shopify Payments

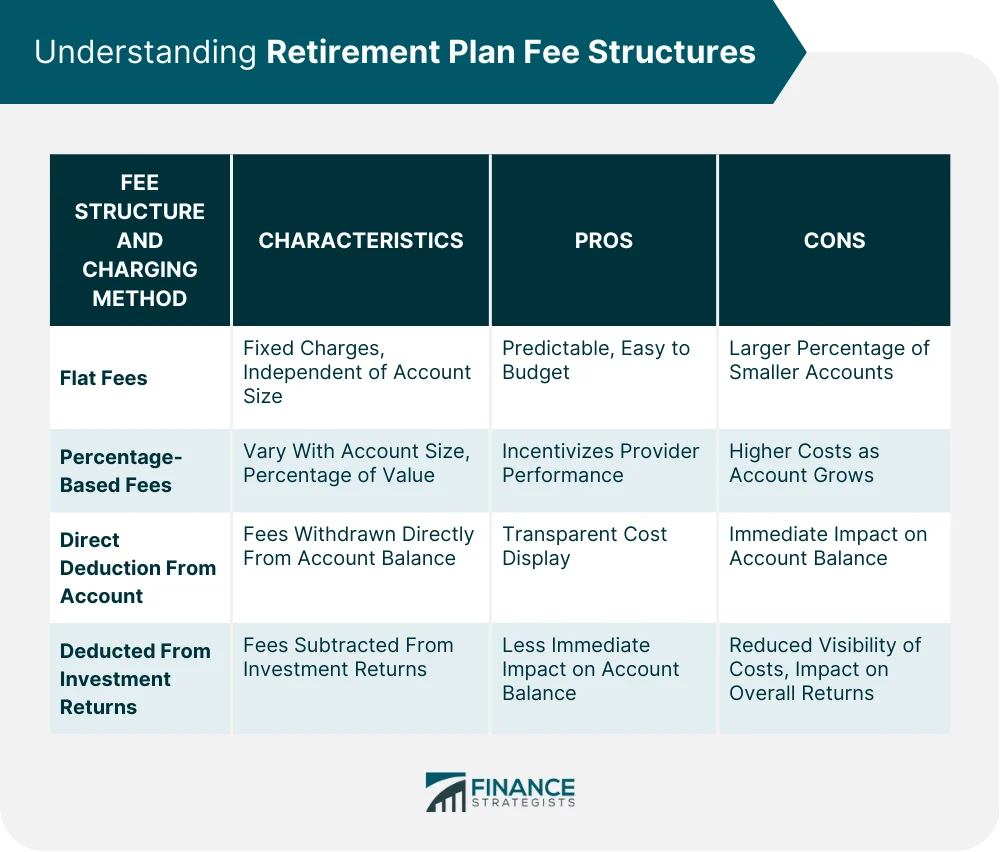

- Understanding the Fee Structure

- Security and Compliance: Not Optional

- Integration Tips for Small Business Owners

- 1. Map Your Workflow First

- 2. Test in a Sandbox Environment

- 3. Leverage Built‑In Apps

- Customer Service: The Unsung Hero

- Future‑Proofing Your Payment Strategy

- Bottom Line: Making the Right Choice

Running a small business today means juggling inventory, marketing, staff, and, of course, payments. When a customer pulls out a plastic card or taps a phone, you need a reliable system that captures that sale fast, securely, and without eating too much into your margin. That’s where credit card processing companies for small business step onto the stage. They act as the bridge between the buyer’s bank, your bank, and the transaction network, turning a swipe into cash (or a bank deposit) in minutes.

But the market is crowded. From legacy processors that have been around since the dial‑up era to sleek, cloud‑native platforms that promise “no‑code” setup, the choices can feel overwhelming. This guide cuts through the noise, outlines the key factors you should evaluate, and highlights a handful of providers that consistently earn high marks among entrepreneurs.

credit card processing companies for small business: What to Look For

Before you sign a contract, take a step back and ask yourself what matters most for your operation. Below are the pillars that should shape your decision‑making.

Choosing the right credit card processing companies for small business

- Transparent pricing: Look for clear breakdowns of transaction fees, monthly fees, and any hidden costs. Flat‑rate pricing (e.g., 2.9% + 30¢ per swipe) is easy to predict, while interchange‑plus can be cheaper if you have high ticket values.

- Integration ease: Does the processor plug into your point‑of‑sale (POS) system, e‑commerce platform, or accounting software without a developer? Seamless API connections save time and reduce errors.

- Security & compliance: PCI‑DSS compliance, tokenization, and EMV support protect both you and your customers from data breaches.

- Customer support: A 24/7 help line, live chat, or dedicated account manager can be a lifesaver during peak sales periods.

- Feature set: Look for recurring billing, mobile wallets (Apple Pay, Google Pay), multi‑currency support, and advanced reporting.

If you’re already exploring other credit‑related products, you might have stumbled upon articles like How to Apply for 0 Interest Credit Card – A Complete Walk‑through. While that guide focuses on consumer cards, the same principles of fee transparency and security apply when you evaluate business processors.

Top Credit Card Processing Companies for Small Business in 2024

Below is a curated list of processors that consistently rank high among small‑business owners. Each entry includes a snapshot of pricing, standout features, and ideal business types.

Square

- Pricing: 2.6% + 10¢ per in‑person swipe; 2.9% + 30¢ for online transactions.

- Why it shines: No monthly fees, free POS hardware for basic setups, and an all‑in‑one dashboard that merges sales, inventory, and payroll.

- Best for: Retail shops, cafés, and service providers who need a quick‑start solution.

Stripe

- Pricing: 2.9% + 30¢ per successful card charge; no setup fees.

- Why it shines: Developer‑friendly APIs, robust support for subscription billing, and global payment methods.

- Best for: E‑commerce sites, SaaS businesses, and startups with custom checkout flows.

PayPal Zettle

- Pricing: 2.7% + 0¢ per in‑person swipe; 2.9% + 30¢ for online.

- Why it shines: Leverages the massive PayPal ecosystem, easy QR‑code payments, and built‑in invoicing.

- Best for: Small vendors, pop‑up shops, and businesses already using PayPal for online sales.

Helcim

- Pricing: Interchange‑plus starting at 0.9% + 10¢ per transaction; monthly fee optional.

- Why it shines: Transparent pricing, multi‑currency support, and a powerful back‑office portal for analytics.

- Best for: Businesses with higher average ticket sizes or international sales.

Shopify Payments

- Pricing: 2.9% + 30¢ for online; 2.7% + 0¢ for in‑store (Shopify POS).

- Why it shines: Fully integrated with Shopify stores, automatic fraud protection, and unified reporting.

- Best for: Merchants already on the Shopify platform looking for a seamless payment experience.

Each of these providers offers a free trial or a “pay‑as‑you‑go” plan, which is perfect for testing the waters before committing to a long‑term contract.

Understanding the Fee Structure

Fees are the most scrutinized part of any processing agreement. While the headline “2.9% + 30¢ per swipe” looks simple, the reality includes several moving parts:

- Interchange fees: Set by card networks (Visa, Mastercard) and vary by card type, transaction method, and merchant category.

- Assessment fees: Small percentages charged by the network for maintaining the system.

- Markup: The processor’s profit layer added on top of interchange and assessment.

- Monthly/annual fees: Some processors charge a gateway fee, PCI compliance fee, or a flat monthly service charge.

- Chargeback fees: Cost incurred when a customer disputes a transaction.

To keep your margins healthy, calculate the effective rate based on your average ticket size. For example, a bakery with $15 orders will feel the impact of a 30¢ per‑transaction fee more than a boutique selling $200 dresses.

Security and Compliance: Not Optional

Data breaches make headlines for a reason—losing customer card data can cripple a small business both financially and reputationally. When evaluating credit card processing companies for small business, verify that they offer:

- End‑to‑end encryption (E2EE)

- Tokenization that replaces real card numbers with a unique identifier

- EMV chip support for physical cards

- PCI‑DSS Level 1 compliance (the highest standard)

Many processors now provide “point‑to‑point encryption” (P2PE) as a default, meaning the card data is encrypted the moment it touches the reader and never travels in plain text.

Integration Tips for Small Business Owners

Even the best processor can become a headache if it doesn’t play well with your existing tools. Here are three practical steps to ensure a smooth integration:

1. Map Your Workflow First

Sketch out how a sale moves from the POS terminal to your accounting software. Identify any manual data entry points—these are opportunities for automation.

2. Test in a Sandbox Environment

Most modern processors offer a developer sandbox where you can run test transactions without moving real money. Use this space to confirm that refunds, recurring billing, and multi‑currency conversions behave as expected.

3. Leverage Built‑In Apps

Platforms like Square and Stripe host a marketplace of pre‑built integrations (e.g., QuickBooks, Xero, Shopify). Installing an official app reduces the need for custom code and ensures ongoing support.

If you’re also interested in business credit options, the article Business Credit Card for Small Businesses – A Complete Guide walks you through how to pair a processing solution with a credit card that maximizes rewards on those very same transactions.

Customer Service: The Unsung Hero

Imagine a rush hour Saturday and your terminal freezes. A processor with a 24/7 live‑chat line can get you back in business within minutes, whereas a provider that only offers email support might leave you offline for hours. When speaking with sales reps, ask specific questions:

- “What is the average response time for urgent issues?”

- “Do you assign a dedicated account manager for small accounts?”

- “Is there a self‑service portal for dispute management?”

These answers often reveal more about the partnership quality than the fee schedule alone.

Future‑Proofing Your Payment Strategy

Payments technology evolves rapidly. Emerging trends you should keep on your radar include:

- Buy‑Now‑Pay‑Later (BNPL): Services like Afterpay and Klarna let customers split purchases, increasing average order value.

- Contactless and NFC payments: Even small coffee shops now accept tap‑to‑pay via phones or smartwatches.

- Cryptocurrency acceptance: While still niche, some processors enable crypto‑to‑fiat conversion at checkout.

- AI‑driven fraud detection: Machine‑learning models that flag suspicious patterns in real time.

Choosing a processor that already offers—or at least roadmap‑supports—these capabilities will save you the hassle of switching providers later.

Bottom Line: Making the Right Choice

Finding the perfect credit card processing companies for small business isn’t about picking the cheapest option; it’s about aligning pricing, features, security, and support with the unique rhythm of your operations. Start by listing your must‑have functionalities—whether it’s seamless e‑commerce integration, in‑store mobile POS, or multi‑currency billing. Then, compare the top contenders, run a few test transactions, and read the fine print on fees and contracts.

Remember, the best processor will grow with you. As sales volumes rise and your product line expands, the same platform should handle higher transaction counts, support new payment methods, and provide deeper analytics without a painful migration.

Take the time to evaluate, test, and ask the right questions. In the end, a well‑chosen payment partner not only safeguards your revenue but also frees you to focus on what truly matters: delighting customers and scaling your business.

[ CATEGORY ]: Finance