Table of Contents

- errors and omissions insurance New York: Core Concepts and Why It Matters

- How errors and omissions insurance New York differs from other states

- Who Needs errors and omissions insurance New York?

- Key Legal Requirements in New York

- How to Choose the Right errors and omissions insurance New York Policy

- 1. Assess Your Risk Profile

- 2. Understand Policy Language

- 3. Compare Coverage Limits and Deductibles

- 4. Look for Value‑Added Services

- 5. Get Multiple Quotes

- 6. Review the Insurer’s Reputation

- Cost Factors: What Drives the Premium for errors and omissions insurance New York?

- Common Exclusions to Watch Out For

- Filing a Claim: Step‑by‑Step Process

- Tips for Reducing Your Risk and Premiums

- When to Review or Update Your Policy

Running a professional service in the Empire State comes with its own set of risks. Whether you’re a real‑estate broker, a financial advisor, a software developer, or a healthcare consultant, a single mistake—intentional or not—can snowball into a costly lawsuit. That’s where errors and omissions (E&O) insurance steps in, acting like a safety net that catches you when a client claims you didn’t deliver what was promised.

New York’s unique regulatory environment makes understanding errors and omissions insurance New York especially important. The state’s consumer protection laws are among the strictest in the country, and courts often lean in favor of plaintiffs. In this landscape, a well‑crafted E&O policy isn’t just a nice‑to‑have; it’s a must‑have for anyone offering professional advice or services.

In the sections that follow, we’ll break down the fundamentals of E&O coverage, explore the specific requirements that New York imposes, and share practical tips for finding the right policy without overpaying. By the end, you’ll have a clear roadmap to protect your reputation, finances, and peace of mind.

errors and omissions insurance New York: Core Concepts and Why It Matters

At its core, errors and omissions insurance New York is a form of professional liability insurance. It protects you against claims alleging negligence, mistakes, or failure to deliver services as promised. Unlike general liability insurance, which covers bodily injury or property damage, E&O focuses on the intangible damage caused by advice or professional actions.

Key elements of an E&O policy include:

- Coverage limits: The maximum amount the insurer will pay per claim and in total during the policy period.

- Deductibles: The amount you pay out‑of‑pocket before the insurance kicks in.

- Defense costs: Legal fees and expenses covered in addition to any settlement.

- Exclusions: Specific situations the policy won’t cover, such as intentional wrongdoing.

Because New York courts can award substantial damages—sometimes in the millions—having a robust limit is crucial. Many small firms underestimate their exposure, thinking a single mistake is unlikely to result in a lawsuit. History, however, shows otherwise; even a minor misstatement in a contract can trigger a cascade of legal action.

How errors and omissions insurance New York differs from other states

While the basic structure of an E&O policy is similar nationwide, New York adds a few twists:

- Higher statutory caps: Certain professions, like architects and engineers, face higher minimum coverage requirements set by state law.

- Mandatory disclosures: Professionals must disclose their E&O coverage to clients in writing in many industries, including real estate and finance.

- Regulatory oversight: Agencies such as the New York Department of Financial Services (DFS) may require proof of coverage before issuing licenses.

Understanding these nuances helps you avoid costly compliance missteps that could void your policy when you need it most.

Who Needs errors and omissions insurance New York?

Almost any business that provides advice, design, or professional services should consider E&O coverage. Below is a snapshot of typical candidates:

- Real‑estate brokers and agents

- Financial planners and investment advisors

- Lawyers, accountants, and tax preparers

- Healthcare consultants and medical billing services

- IT consultants, software developers, and SaaS providers

- Architects, engineers, and construction managers

Even freelancers and solo practitioners are not exempt. A single client complaint can lead to a lawsuit that threatens both personal assets and professional reputation. If you’re unsure whether your line of work warrants E&O, think about the potential impact of a mistake: could it cost a client a million dollars? If the answer is yes, you need coverage.

Key Legal Requirements in New York

New York doesn’t impose a blanket legal requirement for all professionals to carry E&O insurance, but many licensing boards do. For example:

- Real Estate: The New York Department of State requires brokers to maintain a minimum of $500,000 in E&O coverage.

- Financial Services: The DFS mandates that registered investment advisers hold at least $1 million in professional liability coverage.

- Legal Professionals: While the State Bar does not require E&O, most law firms purchase it to satisfy client expectations.

Failure to meet these mandates can result in license suspension, fines, or even the loss of the ability to practice. Always verify the specific requirement for your profession before finalizing a policy.

How to Choose the Right errors and omissions insurance New York Policy

Selecting a policy involves more than just comparing price tags. Here’s a step‑by‑step approach to help you land a plan that balances protection and cost:

1. Assess Your Risk Profile

Start by mapping out the types of claims that could arise in your business. Consider the value of contracts you handle, the sensitivity of data you manage, and the regulatory environment you operate in. A higher risk profile justifies higher coverage limits.

2. Understand Policy Language

Insurance documents are notorious for jargon. Pay close attention to:

- “Claims‑Made” vs. “Occurrence” policies: Most E&O policies in New York are claims‑made, meaning they cover incidents reported while the policy is active.

- Retroactive dates: The date from which incidents are covered. If you switch carriers, ensure the new policy’s retroactive date matches or predates your previous one.

3. Compare Coverage Limits and Deductibles

Typical limits range from $250,000 to $5 million. Higher limits increase premiums but provide peace of mind. Pair this with a deductible you can comfortably afford—usually between $1,000 and $10,000.

4. Look for Value‑Added Services

Many insurers bundle risk‑management resources, legal hotlines, or claims‑handling support. These extras can reduce the likelihood of a claim and speed up resolution if one occurs.

5. Get Multiple Quotes

Just like you would when shopping for auto or home insurance, request quotes from at least three carriers. Comparing them side‑by‑side helps you spot hidden fees and understand market rates. For a quick start, you might want to compare auto and home insurance quotes for better savings—the same platforms often let you bundle professional policies for discounts.

6. Review the Insurer’s Reputation

Check financial strength ratings from agencies like A.M. Best or Standard & Poor’s. A carrier with a solid rating is more likely to honor claims even during economic downturns.

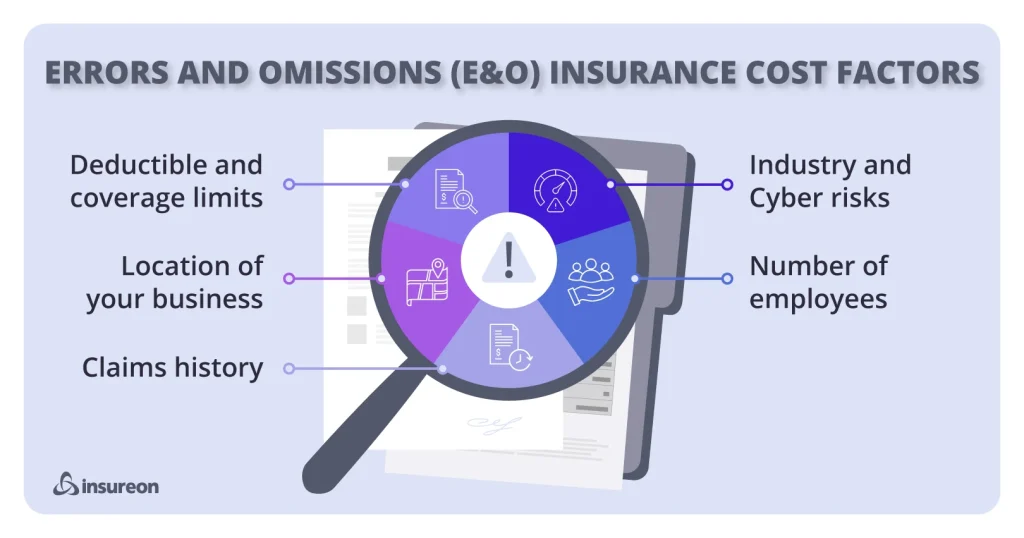

Cost Factors: What Drives the Premium for errors and omissions insurance New York?

Premiums for errors and omissions insurance New York depend on a blend of quantitative and qualitative factors:

- Industry Risk: High‑risk fields (e.g., medical consulting) command higher rates.

- Claims History: A clean record can earn discounts, while prior claims raise premiums.

- Policy Limits & Deductibles: Higher limits increase cost; higher deductibles lower it.

- Business Size: Revenue, number of employees, and contract values influence exposure.

- Geographic Scope: Coverage limited to New York may be cheaper than a multi‑state policy.

On average, a solo professional might pay $500–$1,200 annually, while a mid‑size firm could see premiums ranging from $2,000 to $10,000+. Remember, the cheapest policy may not provide adequate protection, so weigh price against coverage depth.

Common Exclusions to Watch Out For

Even the most comprehensive E&O policy contains exclusions—situations the insurer won’t cover. Typical exclusions include:

- Intentional fraud or criminal acts

- Claims arising from prior known incidents not disclosed during underwriting

- Professional services performed outside the policy’s geographic limits

- Claims related to bodily injury or property damage (covered by general liability)

Read the fine print carefully. If a particular exclusion could affect your practice, ask the insurer about endorsements or separate policies to fill the gap.

Filing a Claim: Step‑by‑Step Process

When a client alleges an error, the following steps help streamline the claim process:

- Notify Your Insurer Promptly: Most policies require immediate notice, often within 30 days of receiving the claim.

- Preserve Documentation: Gather contracts, emails, work product, and any communications related to the alleged mistake.

- Cooperate with the Adjuster: Provide requested information and answer questions honestly.

- Engage Legal Counsel: Many E&O policies include access to a defense attorney; use it.

- Review Settlement Options: Your insurer may recommend settlement; weigh it against potential trial costs.

Timely action not only satisfies policy conditions but also demonstrates good faith, which can influence the insurer’s willingness to defend aggressively.

Tips for Reducing Your Risk and Premiums

Beyond buying a policy, proactive risk management can lower the likelihood of a claim and may qualify you for premium discounts. Consider these strategies:

- Document Everything: Written contracts, scope‑of‑work statements, and client acknowledgments protect both parties.

- Implement Quality Controls: Peer reviews, checklists, and standard operating procedures catch errors before they reach the client.

- Continuous Education: Stay updated on industry regulations and best practices.

- Client Communication: Set realistic expectations and maintain transparent dialogue throughout the engagement.

- Bundle Policies: If you already have general liability or cyber insurance, ask about multi‑policy discounts. A good resource for bundling ideas is the guide on homeowners and auto insurance bundle quotes – how to save smart.

When to Review or Update Your Policy

Business environments evolve, and so should your coverage. Revisit your E&O policy at least annually or whenever any of the following occur:

- You add new services or expand into a different industry segment.

- Revenue or client size experiences significant growth.

- You move operations to additional states.

- Regulatory changes affect your licensing requirements.

A periodic review ensures you maintain adequate limits, avoid gaps, and capture any new discounts or endorsements that may be available.

In short, errors and omissions insurance New York is more than a regulatory checkbox—it’s a strategic investment in the longevity of your professional practice. By understanding the specific state requirements, assessing your risk, and choosing a policy that aligns with your business goals, you can focus on delivering top‑notch service without the constant fear of a costly lawsuit.

Whether you’re a seasoned consultant or just starting out, taking the time now to secure solid E&O coverage will pay dividends in peace of mind and financial security for years to come.