Table of Contents

- Why professional liability insurance for small business matters

- What does professional liability insurance for small business cover?

- Common claims small businesses face

- How to choose the right professional liability insurance for small business

- Assessing your risk profile

- Comparing quotes and coverage

- Cost factors and budgeting tips for professional liability insurance for small business

- Understanding premium drivers

- Ways to lower your premium

- Legal requirements and industry‑specific considerations

- When is it mandatory?

- Specialized professions and tailored policies

Running a small business is a thrilling ride—there’s the excitement of landing new clients, the satisfaction of delivering a service you’re proud of, and the constant hustle to keep everything afloat. Yet, amidst the daily grind, there’s a silent risk that can knock the wind out of your operation if you’re not prepared: a professional mistake that leads to a costly lawsuit. That’s where professional liability insurance for small business steps in, acting as a safety net that protects your reputation, finances, and peace of mind.

Imagine you’re a freelance graphic designer who accidentally uses a copyrighted image for a client’s marketing campaign. The client sues, claiming damages for the infringement. Without the right coverage, you could be forced to dip into personal savings or even risk bankruptcy. On the other hand, with professional liability insurance for small business, you have a dedicated policy that covers legal defense costs, settlements, and other expenses tied to such claims.

In this guide we’ll break down everything you need to know about professional liability insurance for small business—from what it actually covers, to how you pick the right policy, and clever ways to keep premiums affordable. Whether you’re a consultant, a tech start‑up, or a health‑care provider, the principles stay the same, and the insights will help you make an informed decision.

Why professional liability insurance for small business matters

Professional liability insurance for small business, sometimes called errors and omissions (E&O) insurance, is designed specifically for businesses that provide advice, services, or expertise. Unlike general liability policies that protect against bodily injury or property damage, this coverage focuses on claims arising from professional negligence, mistakes, or failure to deliver promised results.

Small businesses are especially vulnerable because they often lack the deep pockets that larger corporations use to fight legal battles. A single lawsuit can drain cash reserves, damage client relationships, and even force you to shut down. Having a professional liability policy means you’re not shouldering that risk alone; the insurer steps in to handle legal fees, settlements, and any court‑ordered damages.

What does professional liability insurance for small business cover?

- Legal defense costs: Attorney fees, court filing fees, and expert witness expenses can quickly climb into the tens of thousands.

- Settlements and judgments: If you’re found liable, the policy can pay out the awarded amount up to the policy limit.

- Claim investigation: Some insurers cover the cost of investigating a claim to determine its validity before it escalates.

- Regulatory fines: In certain professions, the policy may help cover penalties imposed by licensing boards.

It’s crucial to read the fine print. Not every policy includes the same per‑occurrence limit, aggregate limit, or specific exclusions. For instance, a policy might exclude claims related to intentional wrongdoing or certain types of services. Understanding the scope ensures you’re not caught off guard when a claim lands on your desk.

Common claims small businesses face

While the exact nature of a claim varies by industry, some recurring themes pop up across the board:

- Misrepresentation: A consultant promises a specific outcome that doesn’t materialize, leading the client to claim lost revenue.

- Negligence: An IT service provider fails to secure a client’s data, resulting in a breach and associated damages.

- Breach of confidentiality: A therapist inadvertently discloses patient information, violating privacy laws.

- Intellectual property infringement: A marketing agency uses copyrighted material without proper licensing.

Each of these scenarios can trigger a lawsuit, and without professional liability insurance for small business, the financial fallout can be devastating.

How to choose the right professional liability insurance for small business

Selecting a policy isn’t just about picking the cheapest premium. You need to align coverage with the specific risks your business faces, while also ensuring the insurer has a solid reputation for handling claims promptly.

Assessing your risk profile

Start by answering a few key questions:

- What services do you provide, and how complex are they?

- Do you handle sensitive data or regulated information?

- How many clients do you serve, and what’s the average contract value?

- What is your history of past claims, if any?

Mapping out these risk factors helps you determine the appropriate coverage limits. For a freelance writer charging $5,000 per project, a $250,000 per‑occurrence limit might be sufficient. In contrast, a software development firm with multi‑million‑dollar contracts may need $1 million or more.

Comparing quotes and coverage

Just as you would shop around for the best auto or home policy, it’s wise to compare multiple professional liability quotes. Look beyond the headline premium and examine:

- Deductibles: Higher deductibles can lower premiums but increase out‑of‑pocket costs when a claim arises.

- Exclusions: Ensure the policy doesn’t exclude core services you offer.

- Claims handling process: An insurer with a smooth, transparent claims process saves you time and stress.

For a broader perspective on insurance comparison, check out our guide on how to compare auto insurance policies – the complete guide. While it focuses on auto coverage, the same principles of evaluating deductibles, limits, and insurer reputation apply to professional liability insurance for small business.

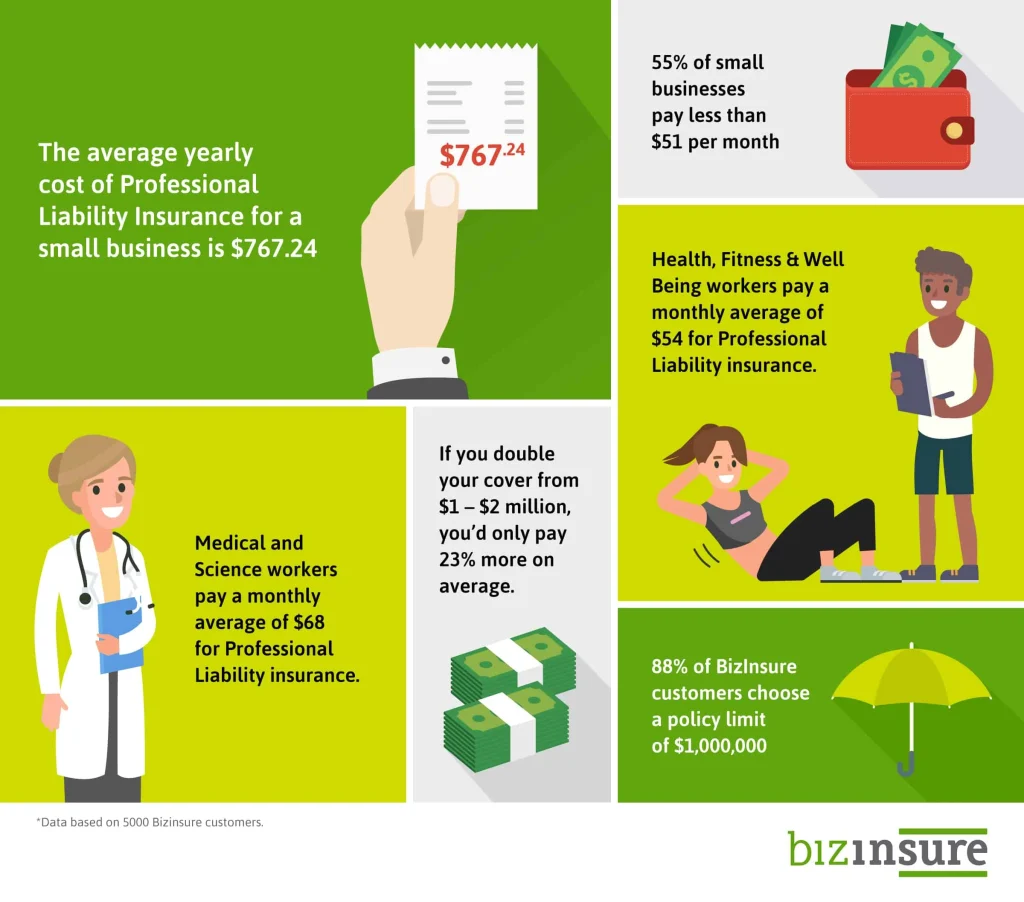

Cost factors and budgeting tips for professional liability insurance for small business

Premiums for professional liability insurance for small business are influenced by a mix of industry risk, claim history, coverage limits, and even the size of your client base. Understanding these drivers helps you control costs without sacrificing essential protection.

Understanding premium drivers

- Industry risk level: High‑risk professions (e.g., financial advisors, architects) typically pay more than low‑risk ones (e.g., consultants).

- Revenue and contract size: Bigger contracts mean higher potential liability, which drives up premiums.

- Claims history: A clean record can earn you discounts, while past claims may increase rates.

- Geographic location: Some states have higher litigation rates, influencing pricing.

Ways to lower your premium

Even small businesses can implement cost‑saving measures:

- Bundle policies: Pair professional liability with general liability or cyber insurance for a multi‑policy discount. Our article on home and car insurance bundle quotes – how to save big explains how bundling works for other lines of coverage.

- Increase deductibles: If your cash flow allows, a higher deductible can shave a few hundred dollars off your annual premium.

- Risk management training: Demonstrating proactive steps—like regular staff training or adopting industry‑standard best practices—can qualify you for lower rates.

- Review coverage annually: Business needs evolve; a policy that was perfect last year might be over‑insuring you today.

Remember, the cheapest policy isn’t always the best. Balance affordability with adequate limits to avoid being under‑insured when a claim hits.

Legal requirements and industry‑specific considerations

Not every small business is legally mandated to carry professional liability insurance for small business, but many professions face licensing requirements that make it essential—or even compulsory.

When is it mandatory?

Regulatory bodies often require certain professionals to maintain coverage:

- Healthcare providers: Physicians, therapists, and home‑care agencies may need malpractice or professional liability coverage to retain licensure.

- Financial services: Advisors, accountants, and insurance agents are frequently required to hold E&O policies.

- Legal professionals: Attorneys must have malpractice insurance in most jurisdictions.

If you fall into any of these categories, failing to secure professional liability insurance for small business could result in fines, loss of license, or suspension of operations.

Specialized professions and tailored policies

Some industries have unique risk exposures that standard policies don’t fully address. For example, a software development firm may need coverage for data breach liability, while an architectural practice might require protection for design errors that cause construction delays. Look for insurers that offer “tailored” endorsements or industry‑specific extensions.

One useful resource for niche coverage details is the Errors and Omissions Insurance New York – Your Complete Guide. Although focused on New York, the guide outlines how specialized endorsements work and can help you ask the right questions when negotiating a policy.

Finally, keep an eye on emerging trends. The rise of remote work and digital service delivery has introduced new liability considerations—such as cyber‑related professional errors. Adding a cyber‑risk endorsement to your professional liability policy can fill that gap without a separate policy.

In the end, professional liability insurance for small business isn’t a luxury; it’s a strategic investment that safeguards the very foundation of what you’ve built. By understanding the coverage, evaluating your specific risks, and shopping smart, you can secure peace of mind while keeping your budget in check. As you grow, revisit your policy annually, adjust limits, and stay abreast of industry changes. With the right protection in place, you’ll be free to focus on what you love—delivering outstanding service and watching your small business thrive.