Table of Contents

- Understanding Professional Liability Insurance for Small Businesses

- Why Small Businesses Can’t Afford to Ignore Professional Liability Insurance

- Assessing Your Risk: Do You Really Need Professional Liability Insurance?

- Professional Liability Insurance for Small Businesses – Risk Checklist

- Choosing the Right Policy: Tips for Small Business Owners

- Professional Liability Insurance for Small Businesses – How to Pick the Best Coverage

- Cost Factors: What Influences Premiums for Professional Liability Insurance?

- Steps to Secure Professional Liability Insurance for Small Businesses

- Maintaining Your Coverage: Best Practices Over Time

Running a small business is a juggling act—balancing cash flow, marketing, client relations, and the day‑to‑day operations that keep the doors open. Amid all that, one thing often slips through the cracks: professional liability insurance. Even if you’re a solo consultant, a boutique design studio, or a tech startup, the risk of a client lawsuit can be a financial nightmare.

Imagine a scenario where a client claims your advice caused them a loss, or a project you delivered didn’t meet the promised standards. The legal fees, settlement costs, and potential damage to your reputation can cripple a fledgling company. That’s where professional liability insurance for small businesses steps in, acting like a safety net that lets you focus on growth instead of worrying about “what‑if” lawsuits.

If you’re still unsure whether you need this coverage, you’re not alone. Many entrepreneurs think it’s only for big firms or lawyers, but the reality is far different. In the sections that follow, we’ll break down what professional liability insurance for small businesses actually covers, how to evaluate your risk, and practical steps to secure the right policy without breaking the bank.

Understanding Professional Liability Insurance for Small Businesses

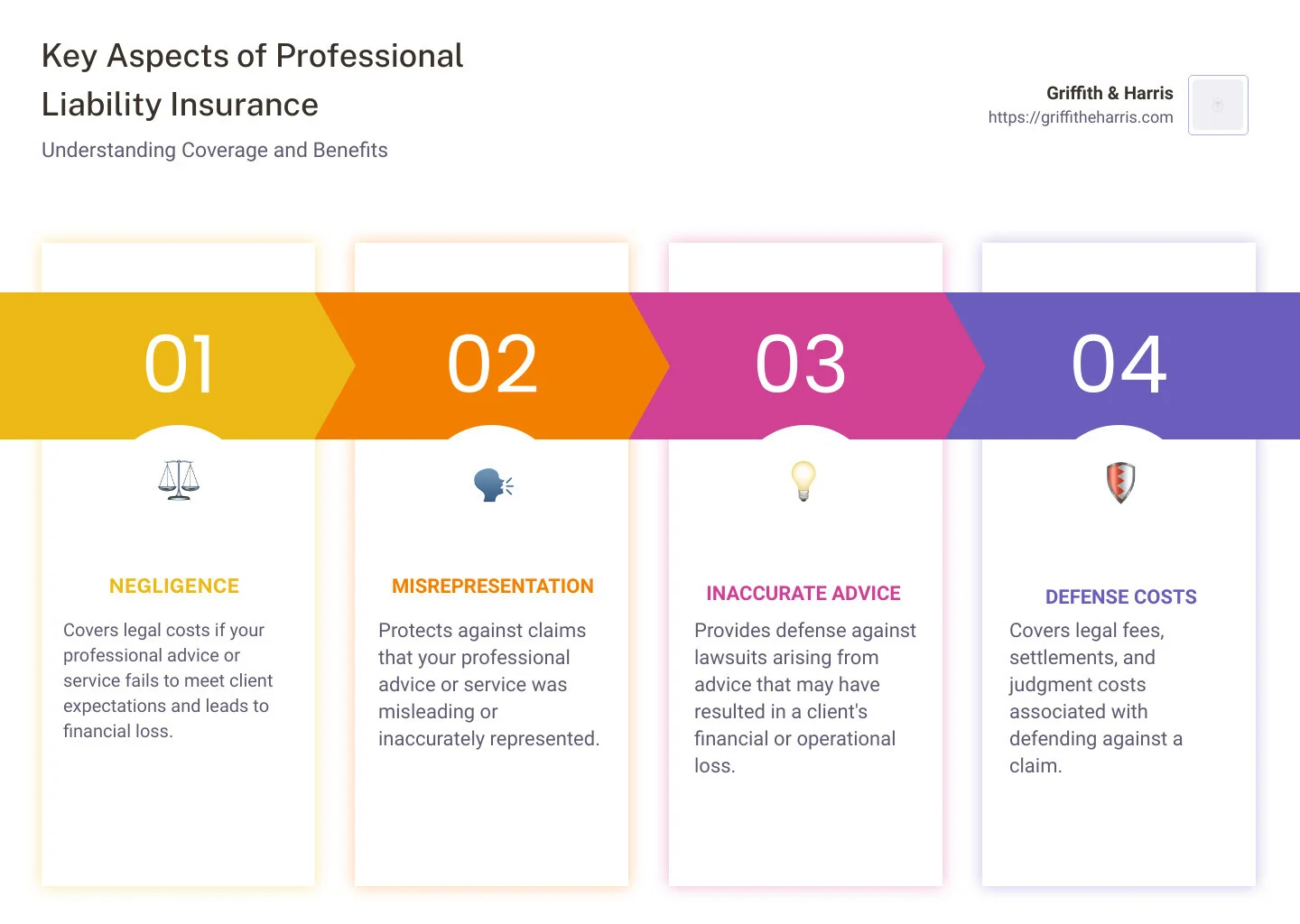

Professional liability insurance—sometimes called errors and omissions (E&O) insurance—protects you against claims of negligence, mistakes, or failure to deliver professional services as promised. Unlike general liability insurance, which covers bodily injury or property damage, professional liability focuses on the intangible damages that arise from the advice, expertise, or services you provide.

Key components of a typical policy include:

- Legal defense costs: Even if the claim is unfounded, attorney fees can add up quickly.

- Settlements or judgments: Covers the amount you’re ordered to pay the claimant.

- Claims-made vs. occurrence policies: Most small‑business policies are claims‑made, meaning they cover claims filed while the policy is active.

For a deeper dive into the mechanics of this coverage, check out our Professional Liability Insurance for Small Business – A Complete Guide. It walks you through the nuances of claims‑made policies and why they matter for startups.

Why Small Businesses Can’t Afford to Ignore Professional Liability Insurance

Small businesses often operate on thin margins, making a large, unexpected expense feel catastrophic. A single lawsuit can deplete cash reserves, force you to halt operations, or even lead to bankruptcy. Here are three common scenarios where professional liability insurance becomes a lifesaver:

- Consulting errors: A financial advisor gives a client a recommendation that results in a loss.

- Design flaws: An architect’s blueprint contains a mistake that leads to costly construction revisions.

- IT mishaps: A software developer’s code fails, causing a client’s system downtime and revenue loss.

In each case, the claim isn’t about a broken window or a slip‑and‑fall; it’s about professional judgment. That’s why a generic general liability policy won’t protect you, and why professional liability insurance for small businesses is a distinct, essential line of defense.

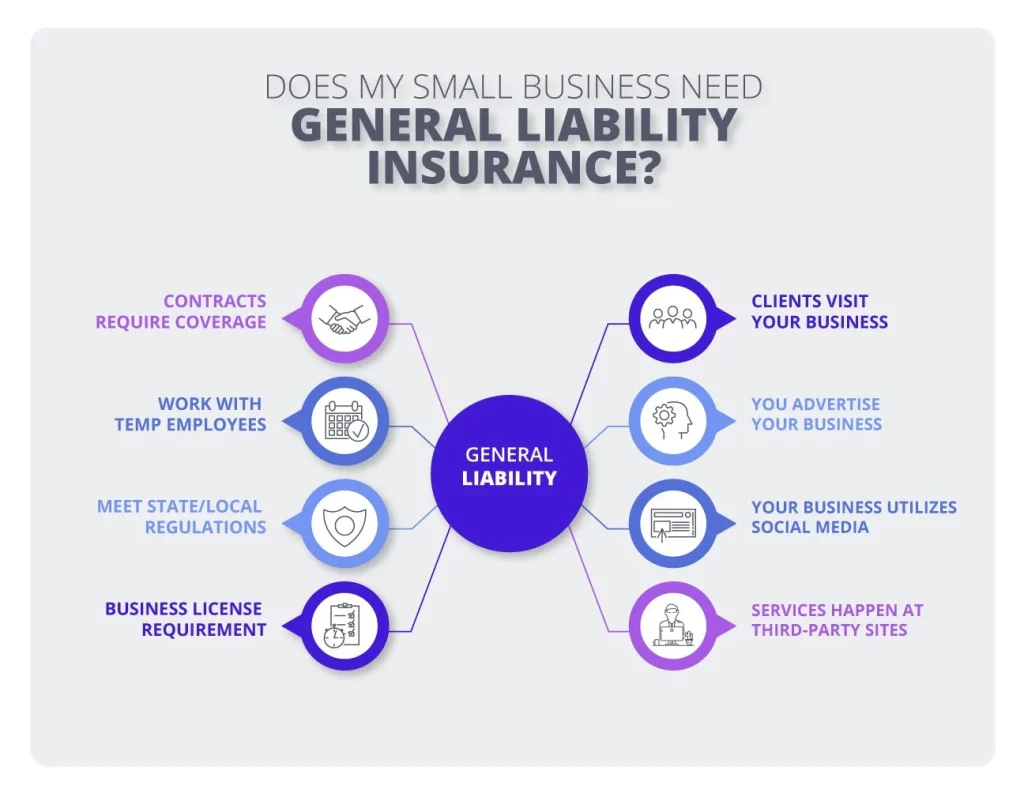

Assessing Your Risk: Do You Really Need Professional Liability Insurance?

Before you buy a policy, it helps to evaluate the specific risks tied to your industry and services. Use the following checklist to gauge your exposure:

Professional Liability Insurance for Small Businesses – Risk Checklist

- Do you provide advice, consulting, or expertise that clients rely on for financial or operational decisions?

- Is there a contract clause that limits your liability, or is it vague?

- How much would a single lawsuit cost your business (legal fees, settlements, lost revenue)?

- Do clients or partners require you to carry professional liability coverage as a condition of doing business?

If you answered “yes” to most of these, you’re likely in the high‑risk category and should prioritize obtaining professional liability insurance. Even low‑risk professions, such as freelance writers or photographers, can face copyright or plagiarism claims, making coverage worthwhile.

Choosing the Right Policy: Tips for Small Business Owners

Finding a policy that fits your budget and risk profile can feel overwhelming, but breaking the process into manageable steps makes it easier. Below are practical tips you can apply today.

Professional Liability Insurance for Small Businesses – How to Pick the Best Coverage

- Compare quotes: Reach out to at least three insurers. Use tools like The Ultimate Guide to Finding the Most Affordable Car and Home Insurance for ideas on how to evaluate cost‑effectiveness.

- Understand limits and deductibles: A higher limit protects you from large claims but may increase premiums. Balance this with a deductible you can comfortably pay.

- Check exclusions: Some policies won’t cover claims arising from prior incidents, certain types of work, or intentional wrongdoing.

- Look for industry‑specific endorsements: If you’re a healthcare consultant, a cyber‑risk endorsement may be crucial.

- Read reviews and financial ratings: An insurer’s ability to pay claims matters. Look at AM Best or Moody’s ratings.

If you operate in New York, you might also want to explore the state‑specific nuances covered in our Errors and Omissions Insurance New York – Your Complete Guide. It highlights local regulations and common pitfalls for professionals in the Empire State.

Cost Factors: What Influences Premiums for Professional Liability Insurance?

Premiums are not one‑size‑fits‑all; they depend on several variables:

- Industry risk level: High‑risk sectors like finance or engineering generally pay more.

- Revenue and payroll: Larger businesses with higher revenue may face higher premiums.

- Claims history: A clean record can earn discounts, while past claims raise rates.

- Policy limits: The higher the coverage limit, the higher the cost.

- Geographic location: Some states have higher litigation rates, affecting pricing.

To keep costs manageable, consider bundling professional liability with other policies (e.g., general liability or property insurance). Many insurers offer multi‑policy discounts that can shave 10‑20% off your total premium.

Steps to Secure Professional Liability Insurance for Small Businesses

Now that you understand the “why” and “what,” here’s a straightforward roadmap to get covered:

- Gather business information: Revenue, number of employees, services offered, and any existing contracts.

- Identify coverage needs: Determine the limit you need based on potential claim sizes in your industry.

- Request quotes: Contact at least three carriers or use an online broker.

- Review policy language: Pay close attention to exclusions, claims‑made vs. occurrence wording, and any required endorsements.

- Finalize and purchase: Sign the agreement, set up payment, and keep the certificate of insurance handy for clients.

Most insurers will provide a digital certificate within 24‑48 hours, making it easy to share with prospective clients who may request proof of coverage.

Maintaining Your Coverage: Best Practices Over Time

Getting a policy is just the beginning. To keep your protection robust, follow these maintenance habits:

- Annual policy review: Business changes—new services, larger contracts, or hiring—can affect risk.

- Update limits: As your revenue grows, consider raising your coverage limits.

- Document incidents: Even minor client complaints should be recorded; they can help defend against future claims.

- Stay informed on legal trends: New regulations or case law can shift what’s considered a covered claim.

Proactive risk management not only reduces the likelihood of a lawsuit but can also lead to lower premiums during renewal periods.

In summary, professional liability insurance for small businesses isn’t a luxury—it’s a strategic investment that shields your hard‑earned reputation and finances from the unpredictable world of client disputes. By understanding your risk, comparing quotes, and staying diligent with policy upkeep, you can secure peace of mind while you grow your venture.

Remember, the cost of a single claim can dwarf the annual premium you pay for coverage. Taking the time now to protect your business will pay dividends in stability, client confidence, and long‑term success.

[Finance]: Finance