Table of Contents

- errors and omissions insurance for accountants: What It Really Is

- Key components of errors and omissions insurance for accountants

- Why Every Accountant Needs Errors and Omissions Insurance

- Common Scenarios Covered by Errors and Omissions Insurance for Accountants

- How to Choose the Right Errors and Omissions Insurance for Accountants

- 1. Coverage limits and deductibles

- 2. Tail coverage

- 3. Industry‑specific endorsements

- 4. Reputation and claims handling

- 5. Cost considerations

- Typical Exclusions You Should Watch Out For

- How to Lower Your Premium Without Sacrificing Protection

- Steps to File a Claim Under Errors and Omissions Insurance for Accountants

- Real‑World Benefits: Success Stories from Accountants Who Were Protected

- Future Trends: How the Landscape of Errors and Omissions Insurance for Accountants Is Evolving

Working as an accountant isn’t just about crunching numbers; it’s about providing trusted advice that can shape a client’s financial future. One misstep—whether a simple calculation error or a misinterpreted tax rule—can turn a routine engagement into a costly lawsuit. That’s why many professionals turn to errors and omissions insurance for accountants. This type of coverage acts like a safety net, protecting you from the financial fallout of claims alleging negligence, mistakes, or inadequate work.

In today’s fast‑moving business environment, clients expect flawless service, and regulatory scrutiny is higher than ever. Even the most diligent accountant can fall prey to an unexpected audit, a software glitch, or an ambiguous regulation that leads to a claim. While you can’t eliminate the risk entirely, you can manage it smartly with the right insurance strategy. Below, we’ll unpack the nuts and bolts of errors and omissions insurance for accountants, explore what’s typically covered, and give you practical tips on picking a policy that fits your practice.

Ready to safeguard your reputation and bottom line? Let’s dive into the details of errors and omissions insurance for accountants and see how it can become a core part of your risk‑management toolkit.

errors and omissions insurance for accountants: What It Really Is

At its core, errors and omissions insurance for accountants—sometimes called professional liability insurance—covers legal costs and settlements arising from claims that you failed to perform your professional duties adequately. Unlike general liability insurance, which protects against bodily injury or property damage, this policy focuses on the intellectual and advisory side of your work.

Key components of errors and omissions insurance for accountants

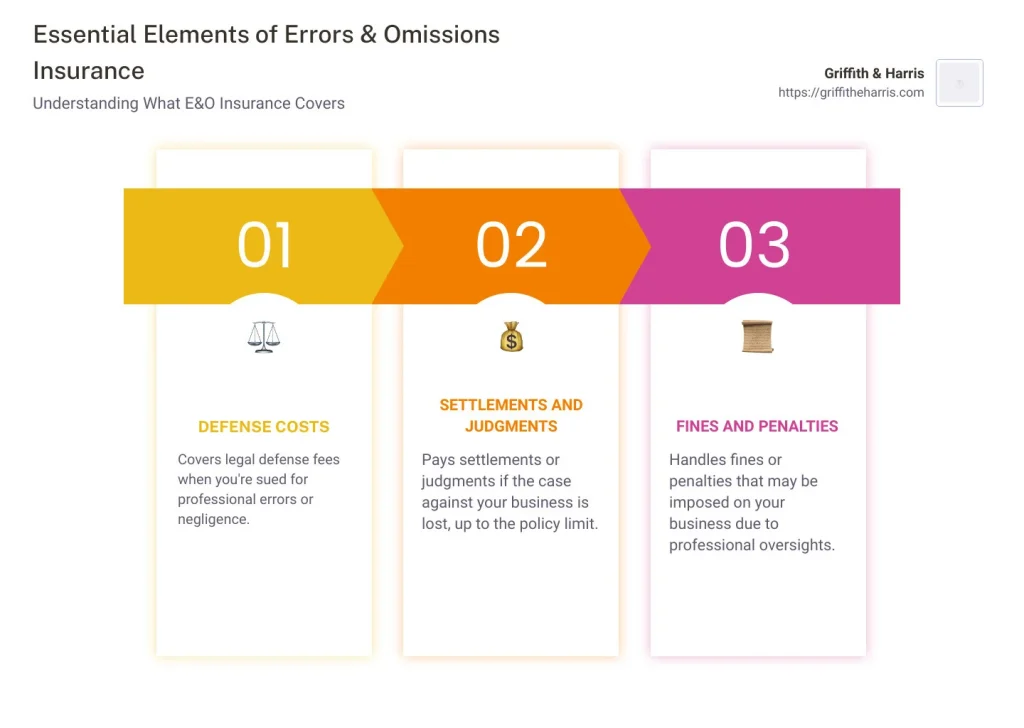

- Defense costs: Legal fees, expert witness charges, and court expenses, even if the claim is groundless.

- Settlements and judgments: Payments required to resolve a claim, up to the policy limit.

- Retroactive coverage:</ Protection for incidents that occurred before the policy start date, as long as the claim is filed while the policy is active.

- Claims‑made vs. occurrence policies: Most accountants opt for a claims‑made policy, meaning the claim must be made during the coverage period.

Because accountants often deal with confidential financial data, many insurers also include coverage for data breach expenses and privacy violations, though these may be subject to separate endorsements.

Why Every Accountant Needs Errors and Omissions Insurance

Even if you run a solo practice or a mid‑size firm, the potential financial exposure from a single lawsuit can be devastating. A single claim can run into hundreds of thousands of dollars, quickly draining cash reserves and jeopardizing your ability to operate. Errors and omissions insurance for accountants helps you:

- Maintain client confidence by showing you take risk management seriously.

- Protect personal assets, especially if you operate as a sole proprietor.

- Cover costs that aren’t deductible as business expenses, such as legal fees.

- Stay compliant with professional bodies that often require proof of coverage.

Think of it as an investment in peace of mind—allowing you to focus on delivering high‑quality service rather than worrying about the “what‑ifs.”

Common Scenarios Covered by Errors and Omissions Insurance for Accountants

Understanding the types of claims that trigger coverage can help you assess whether your current policy meets your needs. Here are a few real‑world examples:

- Tax preparation errors: Miscalculating a client’s tax liability, leading to penalties and interest.

- Audit defense failures: Providing inadequate support during an IRS audit, resulting in additional taxes.

- Advisory mishaps: Recommending a financial strategy that ultimately harms a client’s cash flow.

- Software glitches: Relying on accounting software that malfunctions, causing misstated financial statements.

- Conflict of interest accusations: Overlooking a potential conflict that leads to a breach of fiduciary duty claim.

For a broader look at how professional liability works in other fields, you might check out the errors and omissions insurance for consultants – What You Need to Know article, which shares many parallels with accounting practices.

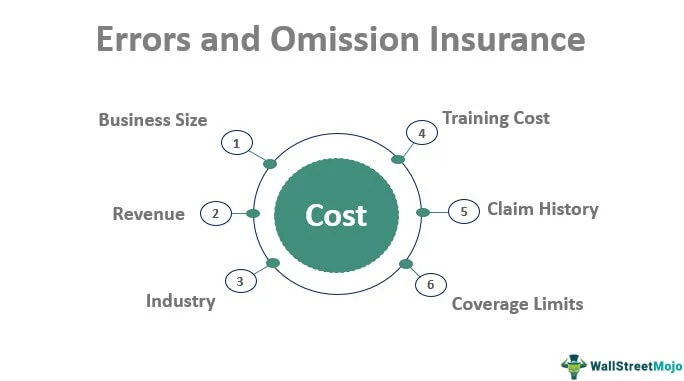

How to Choose the Right Errors and Omissions Insurance for Accountants

Selecting a policy isn’t just about picking the cheapest premium. You need to evaluate coverage limits, exclusions, and the insurer’s reputation for handling claims. Below are the main factors to weigh:

1. Coverage limits and deductibles

Typical limits range from $250,000 to $5 million, depending on the size of your firm and the complexity of services offered. Higher limits provide stronger protection but increase premiums. Pair that with a deductible that fits your cash flow—common deductibles sit between $1,000 and $10,000.

2. Tail coverage

If you’re on a claims‑made policy, consider purchasing “tail” coverage when you retire or switch insurers. Tail coverage protects you from claims filed after the policy ends for work performed while it was active.

3. Industry‑specific endorsements

Some insurers offer endorsements for niche services such as forensic accounting, international tax, or payroll processing. Make sure any extra services you provide are explicitly covered.

4. Reputation and claims handling

Read reviews, ask peers, and check the insurer’s track record for settling claims promptly. A fast, fair settlement process can make a huge difference during a stressful lawsuit.

5. Cost considerations

Premiums typically range from $500 to $2,500 per year for solo accountants, and can rise to $5,000 or more for larger firms. While cost is important, remember that a policy that saves you from a $100,000 lawsuit is a bargain.

If you’re exploring other insurance types that complement errors and omissions coverage, the Professional Liability Insurance for Small Businesses – What You Need to Know guide offers a solid overview of complementary policies.

Typical Exclusions You Should Watch Out For

No policy is all‑inclusive. Common exclusions in errors and omissions insurance for accountants include:

- Intentional wrongdoing or fraud.

- Claims arising from criminal acts.

- Disputes over unpaid fees (unless accompanied by a professional negligence claim).

- Contractual penalties that aren’t tied to negligence.

- Claims related to services performed before the policy’s retroactive date.

Understanding these gaps helps you decide whether you need supplemental coverage or stricter contract language with clients.

How to Lower Your Premium Without Sacrificing Protection

Insurance premiums can feel steep, especially for new practitioners. Here are some proven strategies to keep costs manageable:

- Maintain a clean claims history: Insurers reward firms with few or no past claims.

- Implement robust internal controls: Documented procedures and regular training reduce the likelihood of errors.

- Bundle policies: Many carriers offer discounts if you combine errors and omissions insurance with general liability or cyber liability policies.

- Choose a higher deductible: Raising your deductible can lower the premium, provided you have enough cash reserves.

- Stay up‑to‑date with certifications: Continuing professional education demonstrates competence, which insurers may view favorably.

Steps to File a Claim Under Errors and Omissions Insurance for Accountants

If you’re ever faced with a claim, act quickly. Here’s a step‑by‑step rundown:

- Notify your insurer: Most policies require prompt notification—usually within 30 days of receiving a claim.

- Gather documentation: Compile contracts, client communications, workpapers, and any relevant emails.

- Cooperate with the adjuster: Provide full access to records and answer questions honestly.

- Engage legal counsel: Many insurers have a network of attorneys experienced in professional liability defense.

- Monitor the process: Keep track of deadlines, settlement offers, and any required client communications.

Early involvement of your insurer can often lead to an out‑of‑court settlement, sparing both parties time and expense.

Real‑World Benefits: Success Stories from Accountants Who Were Protected

Consider the case of a mid‑size CPA firm that faced a $300,000 claim after a client alleged that a tax filing error led to a massive audit. The firm’s errors and omissions insurance for accountants covered legal fees and the settlement, preserving the firm’s cash flow and reputation. Without that coverage, the firm might have faced bankruptcy or been forced to sell assets.

Another solo practitioner was sued for providing faulty financial advice that resulted in a client’s lost investment. The policy’s defense coverage allowed the accountant to hire a top‑tier attorney and negotiate a settlement well below the claim amount, saving the practice from a career‑ending lawsuit.

Future Trends: How the Landscape of Errors and Omissions Insurance for Accountants Is Evolving

Technology is reshaping the accounting profession, and insurers are adapting:

- Automation risk: As AI and machine learning automate routine tasks, new liability exposures emerge—e.g., algorithmic errors.

- Cyber‑linked coverage: More policies now bundle cyber liability with errors and omissions protection, recognizing the overlap between data breaches and professional errors.

- Usage‑based pricing: Insurers are experimenting with premiums tied to the volume of transactions processed, offering more tailored pricing models.

Staying aware of these shifts can help you negotiate policies that reflect the modern realities of accounting work.

In the end, errors and omissions insurance for accountants isn’t just a regulatory checkbox—it’s a strategic investment in the longevity of your practice. By understanding the coverage, assessing your unique risk profile, and partnering with a reputable insurer, you can focus on what you do best: delivering accurate, insightful financial guidance. And when the inevitable hiccup occurs, you’ll have the backing you need to navigate the storm without losing sleep.