Table of Contents

- Understanding Home and Auto Bundle Insurance Quotes

- How to Compare Home and Auto Bundle Insurance Quotes Effectively

- Top Benefits of Bundling Your Home and Auto Policies

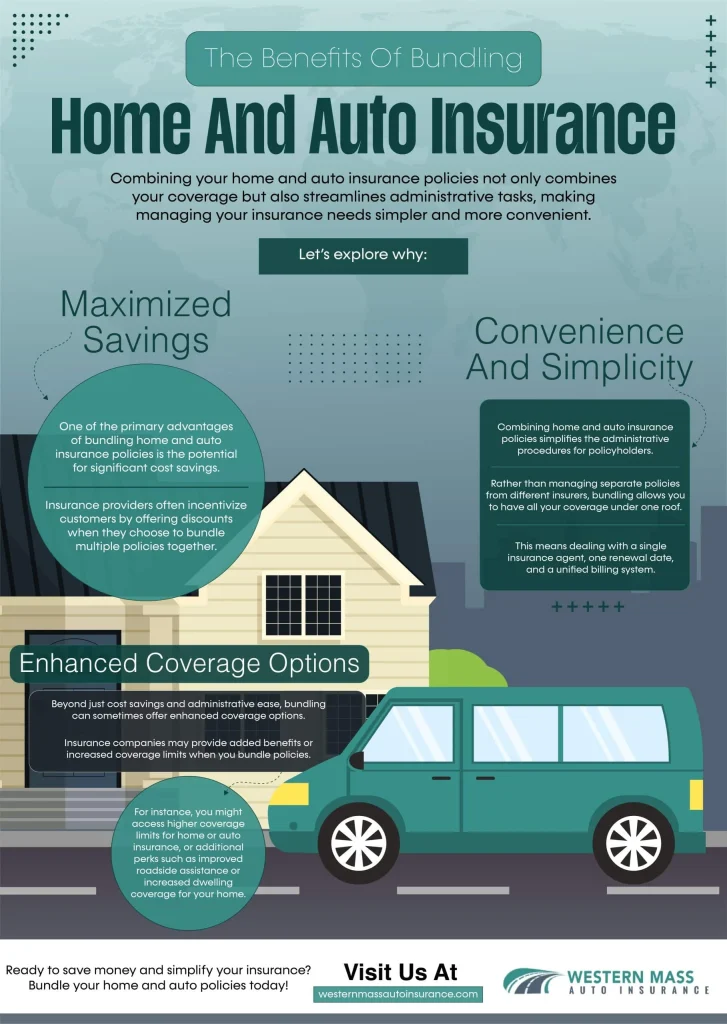

- 1. Tangible Cost Savings

- 2. Simplified Billing and Administration

- 3. Streamlined Claims Process

- 4. Additional Perks and Discounts

- Step‑by‑Step Guide to Getting Your First Home and Auto Bundle Insurance Quote

- Common Misconceptions About Bundling

- Myth 1: “Bundling Means I’ll Lose Coverage Options.”

- Myth 2: “I’m Already Getting the Best Rate on My Standalone Policies.”

- Myth 3: “If I Switch Insurers, I’ll Lose My Discount Forever.”

- When Bundling Might Not Be the Right Choice

- Tips for Maximizing Savings on Your Home and Auto Bundle Insurance Quotes

- Final Thoughts on Home and Auto Bundle Insurance Quotes

When it comes to protecting the places you live and the wheels you drive, most people treat home insurance and auto insurance as two completely separate contracts. That’s a habit that dates back to a time when insurers weren’t as flexible, and the idea of bundling was barely on anyone’s radar. Fast forward to today, and the market is flooded with options that let you combine both policies into a single, streamlined package.

Bundling isn’t just a marketing gimmick; it’s a genuine opportunity to trim premiums, reduce paperwork, and enjoy a more cohesive coverage experience. By pulling together your home and auto policies, you give the insurer a broader view of your risk profile, which often translates into lower rates and added perks.

If you’re curious about how to get the most out of this approach, you’ve landed in the right spot. Below we’ll walk through what home and auto bundle insurance quotes actually mean, why they matter, and how you can leverage them to keep more cash in your pocket while staying well protected.

Understanding Home and Auto Bundle Insurance Quotes

At its core, a home and auto bundle insurance quote is simply a price estimate that covers both your dwelling and your vehicle under one insurer. Instead of juggling two separate statements, you receive a single document that outlines the combined premium, deductible options, and any discounts you qualify for.

Most major carriers—State Farm, Allstate, Progressive, and the like—offer bundled packages, but the exact savings can vary widely depending on factors such as:

- Geographic location and local risk assessments

- Claims history for both home and auto

- Credit score and overall financial profile

- Coverage limits and deductible choices

- Eligibility for multi‑policy discounts

Getting a home and auto bundle insurance quote is typically as easy as filling out an online form or calling a local agent. The key is to provide accurate information for both properties so the insurer can calculate a realistic, competitive price.

How to Compare Home and Auto Bundle Insurance Quotes Effectively

Not all quotes are created equal. Here’s a quick checklist to make sure you’re comparing apples to apples:

- Coverage Scope: Verify that both the home and auto components include the same level of protection you’d expect from standalone policies.

- Discount Details: Some insurers stack discounts (e.g., safe driver + new home). Ensure you’re seeing the total discount amount.

- Deductible Flexibility: Higher deductibles usually mean lower premiums, but make sure you can afford the out‑of‑pocket cost if a claim arises.

- Policy Limits: Check that the limits meet or exceed your needs—especially for personal property, liability, and collision coverage.

- Customer Service Ratings: A lower price isn’t worth it if the insurer’s claim handling is subpar. Look at reviews and complaint ratios.

When you’re ready to start comparing, you might find it helpful to visit resources like Car and Home Insurance Bundle Quotes – How to Save Big and Simplify Coverage for a deeper dive into the savings mechanics.

Top Benefits of Bundling Your Home and Auto Policies

Below are the most compelling reasons why a home and auto bundle insurance quote should be on your radar.

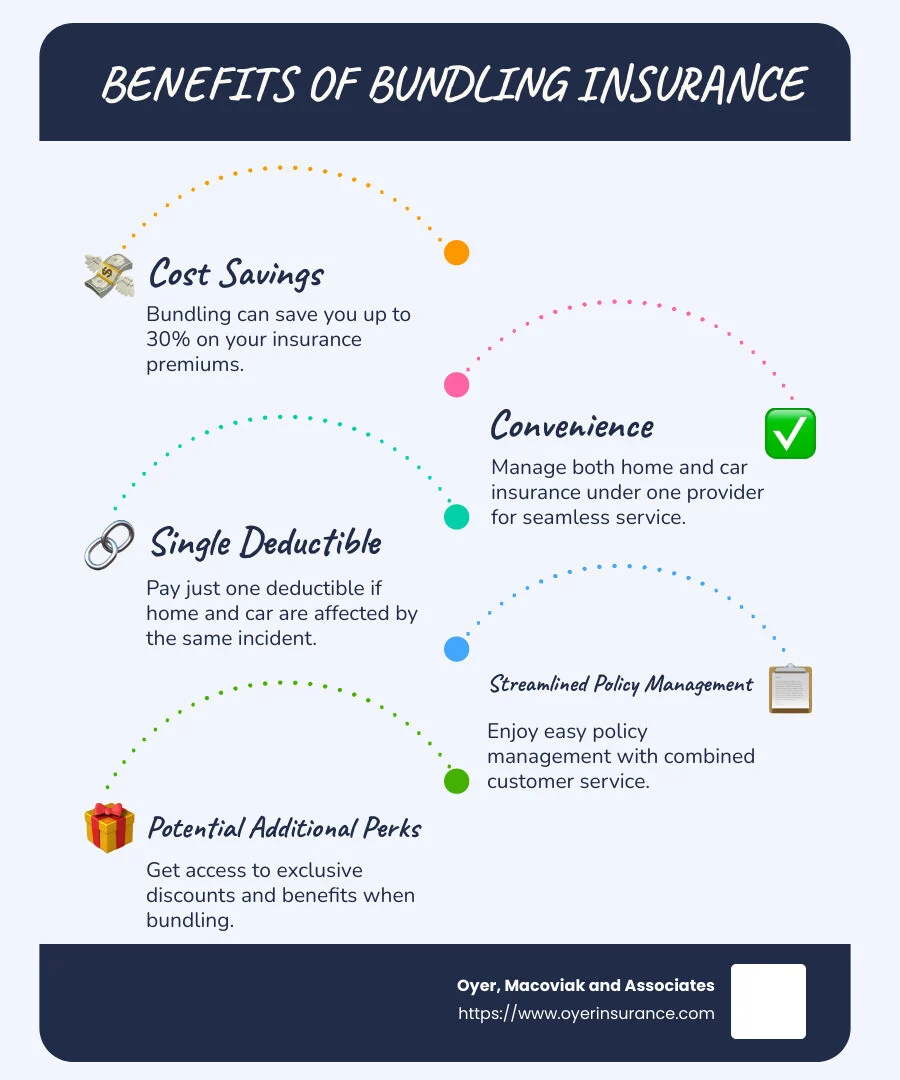

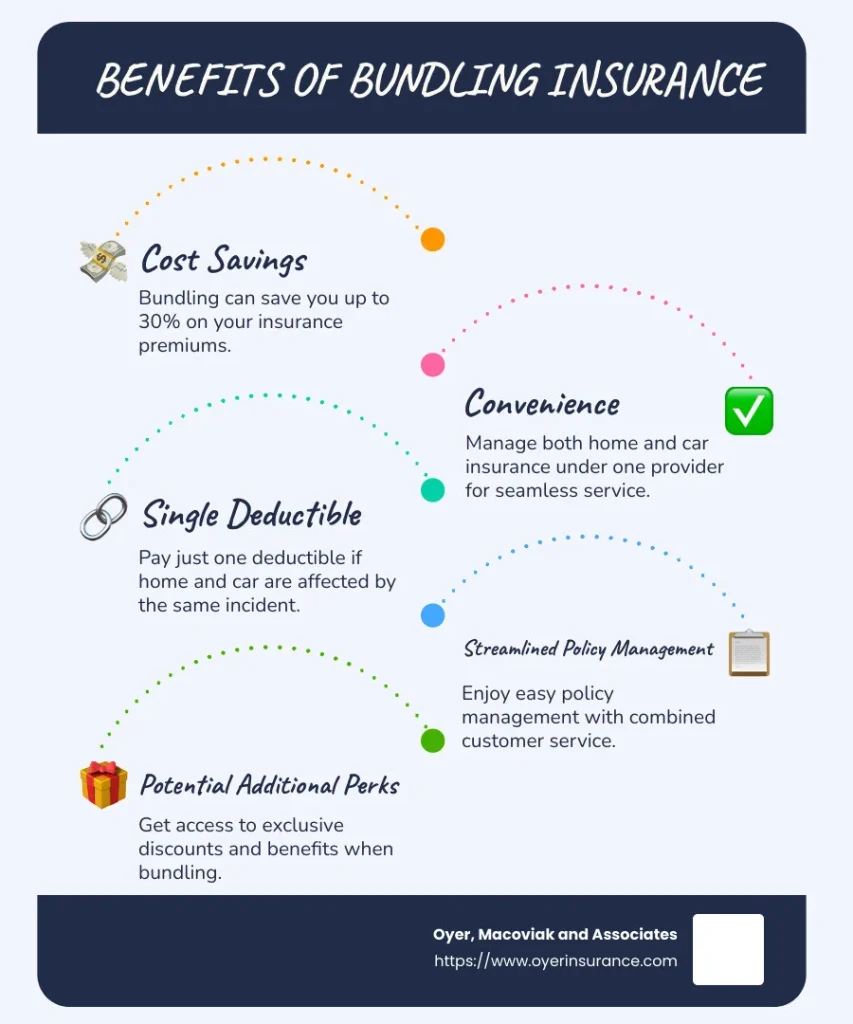

1. Tangible Cost Savings

Bundling can shave anywhere from 5% to 25% off your total premium. Insurers reward you for consolidating risk under one roof, which reduces administrative overhead and makes it easier for them to predict losses.

2. Simplified Billing and Administration

Instead of juggling two due dates, you’ll receive a single bill—often with the option to set up automatic payments. This cuts down on missed payments and the hassle of tracking multiple policies.

3. Streamlined Claims Process

When a mishap involves both your home and your car—think a storm that damages your driveway and knocks your car off the road—having one insurer can speed up the claims handling. You won’t need to coordinate between two separate companies, which can be a relief during stressful moments.

4. Additional Perks and Discounts

Many carriers offer loyalty bonuses, accident forgiveness, or home security discounts that are only available when you hold multiple policies. These can further lower your out‑of‑pocket costs over time.

Step‑by‑Step Guide to Getting Your First Home and Auto Bundle Insurance Quote

Ready to see the numbers for yourself? Follow this straightforward process:

- Gather Your Information: Have your current policy numbers, property details (square footage, construction type, year built), and vehicle info (make, model, VIN) on hand.

- Use an Online Quote Tool: Most insurers feature a bundled‑quote calculator on their website. Fill in the fields accurately for both home and auto.

- Contact an Agent: If you prefer a personal touch, call a licensed agent. They can often pull multiple carrier quotes in minutes.

- Compare the Numbers: Look at total premium, discounts, coverage limits, and deductible options.

- Ask About Customizations: Need extra coverage for flood, jewelry, or rideshare driving? Make sure the bundle can accommodate these add‑ons.

- Make a Decision: Choose the policy that offers the best blend of price, coverage, and service quality.

If you want a ready‑made comparison, the article Bundled Home and Auto Insurance Quotes – Save Money & Simplify Coverage provides a side‑by‑side look at several popular providers.

Common Misconceptions About Bundling

Even though bundling is widely promoted, some consumers hesitate due to lingering myths. Let’s debunk a few.

Myth 1: “Bundling Means I’ll Lose Coverage Options.”

False. Most insurers let you customize each part of the bundle. You can add flood insurance, roadside assistance, or higher liability limits without sacrificing the discount.

Myth 2: “I’m Already Getting the Best Rate on My Standalone Policies.”

Possibly, but you’ll rarely know until you request a bundled quote. Even a modest discount can add up over the life of a policy.

Myth 3: “If I Switch Insurers, I’ll Lose My Discount Forever.”

Many carriers offer “new‑customer” bundling discounts that are as generous as loyalty discounts. Switching can actually boost your savings if you shop around strategically.

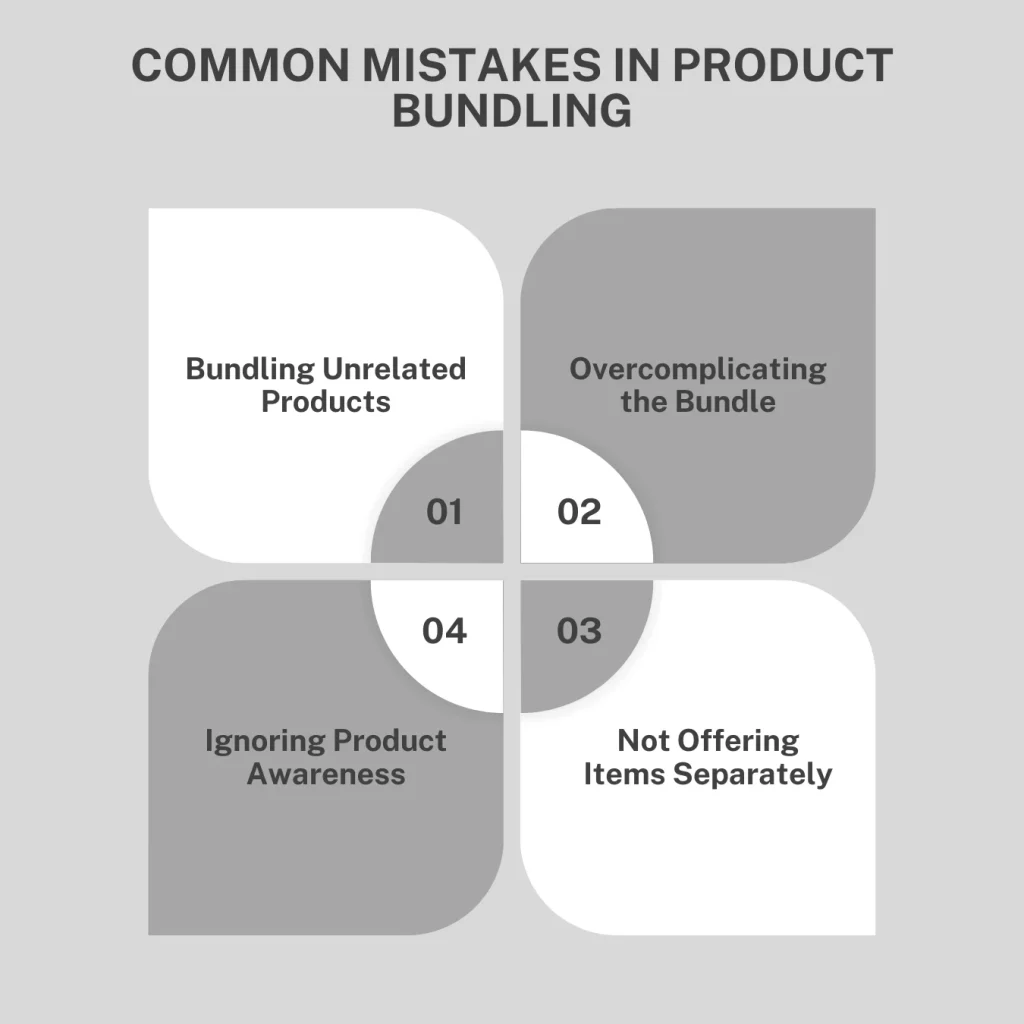

When Bundling Might Not Be the Right Choice

Bundling is powerful, but it isn’t a one‑size‑fits‑all solution. Consider these scenarios where staying separate could make sense:

- Specialized Coverage Needs: If your home is a historic property requiring a niche insurer, or you own a classic car that needs a specialist auto policy, separate policies might provide better tailored coverage.

- Significant Discount Gaps: Occasionally, an insurer may offer a deep discount on a standalone auto policy that outweighs the bundling benefit.

- Company Reputation Issues: If one carrier has poor claim‑handling reviews, you might prefer to keep the other policy with a higher‑rated insurer.

Tips for Maximizing Savings on Your Home and Auto Bundle Insurance Quotes

Even after you receive a bundled quote, there are ways to shave off extra dollars:

- Increase Your Deductibles: Raising both home and auto deductibles by $250–$500 can lower premiums substantially.

- Bundle Additional Policies: Some insurers extend discounts if you add renters, life, or umbrella insurance to the same account.

- Maintain a Good Credit Score: Many insurers factor credit into pricing; a better score usually translates to lower rates.

- Install Safety Devices: Smoke detectors, security systems, anti‑theft devices, and telematics (for safe driving) can all trigger extra discounts.

- Review Annually: Life changes—new home improvements, a new car, or a change in mileage—can affect your risk profile. Re‑quote each year to capture fresh savings.

For a comprehensive walk‑through of these tactics, the guide Auto and Home Insurance Bundle Quotes – Your Complete Guide dives deep into each strategy.

Final Thoughts on Home and Auto Bundle Insurance Quotes

In a world where every dollar counts, home and auto bundle insurance quotes present a practical, often underutilized avenue for both cost reduction and convenience. By consolidating coverage, you not only simplify billing and claims handling but also unlock a suite of discounts that can add up to significant savings over the life of your policies.

The process is straightforward: gather your details, request bundled estimates, compare the numbers, and adjust coverage to match your unique needs. Keep an eye out for myths that may discourage you, and remember that bundling isn’t a rigid contract—there’s flexibility to add endorsements, raise deductibles, or even switch carriers if a better deal emerges.

Ultimately, the decision to bundle should align with your financial goals and risk tolerance. If you value a streamlined experience and want to keep more money in your wallet, a well‑chosen bundle is likely the smarter choice. Take the first step today, request a few home and auto bundle insurance quotes, and see how much you could save while protecting what matters most.