Table of Contents

- Why car insurance and home insurance bundles make sense for most households

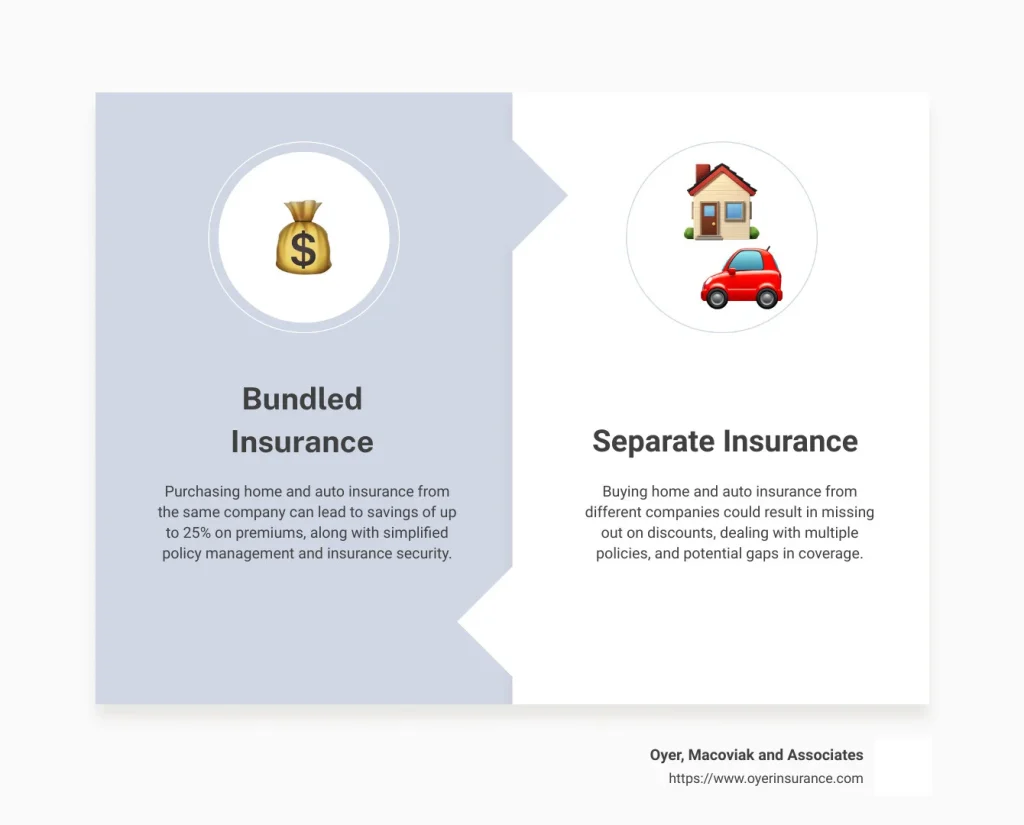

- Financial savings through multi‑policy discounts

- Convenient single billing and renewal cycle

- Potential for broader coverage options

- Key factors to consider before you bundle

- Assess your coverage needs independently first

- Check the insurer’s reputation and claim handling record

- Understand the bundling terms and renewal policies

- How to maximize savings with car insurance and home insurance bundles

- Shop around and compare multiple insurers

- Bundle only if you truly need both policies

- Leverage loyalty and bundling perks

- Take advantage of seasonal promotions

- Real‑world example: The Fort Collins home and auto insurance bundle

- Common myths about bundling and the truth behind them

- Myth #1: Bundling always guarantees the lowest price

- Myth #2: You must keep both policies with the same insurer forever

- Myth #3: Bundling reduces coverage quality

- Step‑by‑step guide to creating your own car insurance and home insurance bundles

When you own both a car and a house, you’re juggling two of the biggest financial responsibilities in everyday life. Managing two separate policies can feel like a juggling act—different renewal dates, separate premium payments, and a handful of insurers to keep track of. That’s where car insurance and home insurance bundles step in, offering a streamlined, cost‑effective solution for busy homeowners and drivers.

Bundling isn’t a new concept, but it’s often overlooked because many people assume that buying policies separately will give them more control or better coverage. In reality, the synergy between your auto and property policies can unlock discounts, simplify claims, and even improve your overall risk profile with insurers. In this deep dive, we’ll explore why bundling makes sense, how to evaluate bundle options, and practical tips to ensure you get the most out of your car insurance and home insurance bundles.

Why car insurance and home insurance bundles make sense for most households

Insurance companies love bundles because they encourage customer loyalty and reduce administrative overhead. For you, the benefits often translate into three core areas: savings, convenience, and enhanced coverage options.

Financial savings through multi‑policy discounts

Most insurers offer a multi‑policy discount that can range from 5% to 25% off each policy’s base premium. The exact percentage depends on factors such as your claim history, the insurer’s underwriting criteria, and the specific combination of coverages. For example, if you pay $1,200 annually for car insurance and $900 for home insurance, a 15% bundle discount could shave off $315 from your total out‑of‑pocket cost.

Convenient single billing and renewal cycle

Having one renewal date means you only need to remember a single payment deadline each year. It also simplifies paperwork: you receive one statement, one set of policy documents, and often a single online portal for managing both coverages. This reduces the chance of missed payments, which could otherwise lead to policy lapses and higher rates.

Potential for broader coverage options

When insurers see that you’re consolidating risk under one roof, they may be more willing to offer optional endorsements—like identity theft protection, roadside assistance, or home equipment breakdown coverage—at a discounted rate. This “cross‑selling” can provide a more comprehensive safety net without the hassle of shopping for each add‑on separately.

Key factors to consider before you bundle

While the advantages are clear, bundling isn’t a one‑size‑fits‑all solution. A careful analysis can prevent you from falling into a “discount trap” where you save on price but sacrifice essential coverage.

Assess your coverage needs independently first

Before you start comparing bundle offers, make sure you know exactly what each policy should cover. For auto, consider liability limits, collision, comprehensive, uninsured motorist, and medical payments. For home, think about dwelling coverage, personal property, liability, and additional living expenses (ALE). If you need higher limits in one area, a bundled policy that caps coverage may not be ideal.

Check the insurer’s reputation and claim handling record

Discounts are great, but they’re meaningless if the insurer is slow to pay legitimate claims. Look up consumer reviews, J.D. Power scores, and state insurance department complaint ratios. A reputable insurer will balance competitive pricing with reliable service—a crucial factor when you’re dealing with both car and property losses.

Understand the bundling terms and renewal policies

Some bundles lock you into a multi‑year contract with a fixed discount that may expire if you make a claim. Others allow you to keep the discount as long as both policies stay active. Read the fine print: Are there cancellation fees? Does the discount apply only to the first year? Knowing these details helps you avoid unpleasant surprises.

How to maximize savings with car insurance and home insurance bundles

Getting the best deal isn’t just about picking the highest discount. It’s a strategic process that involves shopping around, leveraging your existing relationships, and timing your purchases.

Shop around and compare multiple insurers

Even if you’re happy with your current insurer, it never hurts to get quotes from competitors. Use tools like the Getting a Quote on Car Insurance – Your Complete Guide to see how much you could save elsewhere. When you have a competitive quote, you can negotiate with your current provider for a better bundle rate.

Bundle only if you truly need both policies

If you own a car but live in a rented apartment, a renters insurance policy might make more sense than a full homeowners bundle. Conversely, if you have a mortgage with a lender‑required homeowner’s policy, you’ll likely need to keep that coverage, making a bundle with your auto policy a natural fit.

Leverage loyalty and bundling perks

Some insurers reward long‑term customers with additional discounts for each year you stay bundled. Others provide “loyalty credits” that can be applied toward deductible reductions or policy upgrades. Keep track of these incentives and ask your agent about them during renewal season.

Take advantage of seasonal promotions

Insurers often run limited‑time offers—especially in the spring or fall when many people are reviewing their policies. A temporary 10% discount on a bundle could combine with your existing multi‑policy discount for an even larger overall reduction.

Real‑world example: The Fort Collins home and auto insurance bundle

Let’s look at a case study from Fort Collins Home and Auto Insurance Bundle: Save More, Stress Less. A typical family in Fort Collins owned a 2019 sedan and a four‑bedroom house. Individually, their auto premium was $1,150 and their home premium was $1,200. By bundling with a local carrier, they received a 20% discount on each policy, bringing the combined annual cost down to $1,880—a $470 savings.

Beyond the dollar amount, the family appreciated the single online dashboard, which displayed both policies side by side. When a minor water leak caused damage to the kitchen, the claim process was seamless: the same claims adjuster handled both the property damage and the temporary loss of personal belongings, expediting the payout.

Common myths about bundling and the truth behind them

Myth #1: Bundling always guarantees the lowest price

Discounts can be appealing, but the base rates matter more. A bundle with a 10% discount on a higher‑priced policy could still cost more than a separate, lower‑priced policy from a different insurer. Always compare the total cost after discounts, not just the percentage saved.

Myth #2: You must keep both policies with the same insurer forever

Most insurers allow you to split coverage—keeping auto with one company and home with another—if that yields better value. The key is to ensure both policies are active, as many discounts apply only when the insurer sees both under one roof.

Myth #3: Bundling reduces coverage quality

In reality, bundling often improves coverage options because insurers can cross‑sell endorsements at reduced rates. However, you must verify that each policy meets the required limits for your state, mortgage lender, and personal risk tolerance.

Step‑by‑step guide to creating your own car insurance and home insurance bundles

- List your current policies and coverage details. Note premiums, deductibles, limits, and any endorsements.

- Identify potential bundling partners. Look at your current insurer, plus at least two competitors.

- Request bundled quotes. Use online quote tools or speak directly with agents. Ask for a breakdown of the discount applied to each policy.

- Compare total annual costs. Include any fees, discounts, and potential loyalty credits.

- Evaluate coverage quality. Ensure each policy still meets your needs and any lender requirements.

- Negotiate. If a competitor offers a better bundle, see if your current insurer can match or beat it.

- Finalize and set reminders. Once you choose a bundle, mark the renewal date in your calendar and set up automatic payments if possible.

Following these steps can help you avoid the trap of “just because it’s cheaper, it must be better.” Instead, you’ll make an informed decision that balances cost, coverage, and convenience.

Finally, remember that bundling is just one piece of a broader financial strategy. Regularly reviewing your insurance needs—especially after major life events like buying a new car, renovating your home, or adding a teen driver—ensures you stay protected without overpaying.

Whether you’re a first‑time homeowner, a seasoned driver, or both, exploring car insurance and home insurance bundles can lead to meaningful savings and a more manageable insurance experience. Take the time to shop around, ask the right questions, and align your coverage with your lifestyle. In the end, the right bundle can give you peace of mind, knowing you’ve secured both your wheels and your walls without breaking the bank.