Table of Contents

- Understanding Home and Auto Insurance in Texas

- Key Features of Home and Auto Insurance in Texas

- Why Bundling Home and Auto Insurance Makes Sense in Texas

- Choosing the Right Coverage for Your Texas Home

- Getting the Best Auto Insurance in the Lone Star State

- Factors That Influence Premiums in Texas

- Tips to Reduce Your Home and Auto Insurance Costs in Texas

- 1. Bundle Policies

- 2. Raise Your Deductibles

- 3. Install Safety Devices

- 4. Review Coverage Annually

- 5. Take Advantage of State Programs

- 6. Maintain a Clean Driving Record

- Special Considerations for Texas Residents

- How to File a Claim Effectively

- Future Trends in Texas Home and Auto Insurance

Living in the Lone Star State comes with its own set of joys and challenges. From the sprawling Hill Country to the bustling streets of Dallas, Texans enjoy a unique blend of lifestyle, climate, and community. With that diversity, however, comes a need for solid protection against the unexpected—whether it’s a summer tornado, a hailstorm that rattles your roof, or a fender‑bender on I‑35.

That’s where home and auto insurance in Texas steps in. While many residents think of these policies as separate purchases, the truth is they’re often intertwined, and understanding how they work together can save you both money and headaches. In this guide we’ll walk through the basics, explore the nuances specific to Texas, and give you practical tips for getting the best coverage without overpaying.

Before we dive into the nitty‑gritty, let’s set the stage with a quick look at why insurance matters in this state. Texas weather can be extreme—think scorching heat, sudden thunderstorms, and occasional winter freezes. Add in the high traffic volumes in major metros and the prevalence of mobile homes in rural areas, and you’ve got a landscape where comprehensive protection is not just smart, it’s essential.

Understanding Home and Auto Insurance in Texas

When you hear the phrase home and auto insurance in Texas, think of it as a two‑part shield. The home component protects your dwelling, personal belongings, and liability for injuries that occur on your property. The auto side covers vehicle damage, bodily injury, and liability for accidents you might cause. Both are regulated by the Texas Department of Insurance (TDI), which sets minimum standards and ensures companies stay financially sound.

Key Features of Home and Auto Insurance in Texas

- State Minimums: Texas requires a minimum liability coverage of 30/60/25 for auto policies (bodily injury per person, per accident, and property damage). For homeowners, there isn’t a statutory minimum, but lenders typically demand at least enough coverage to protect the mortgage amount.

- Windstorm and Hail Coverage: Because Texas sees frequent hail and wind events, many insurers offer optional “windstorm” endorsements. Without it, you could be left paying out‑of‑pocket for roof repairs.

- Flood Insurance: Standard homeowners policies don’t cover flood damage. Texans in flood‑prone zones should consider a separate NFIP policy.

- Liability Limits: Both home and auto policies allow you to raise liability limits for added peace of mind—especially important if you own a large property or drive a high‑value vehicle.

If you’re curious about why premiums differ from one policy to another, you might want to read Why Do Insurance Companies Charge Premiums? Understanding the Basics. That article breaks down the factors insurers consider, many of which apply directly to Texas homeowners and drivers.

Why Bundling Home and Auto Insurance Makes Sense in Texas

One of the smartest ways to lower costs while keeping coverage robust is to bundle your policies. Many carriers offer discounts of 10%–25% when you purchase both home and auto insurance from the same provider. This is especially valuable in Texas, where the risk of natural disasters can push premiums higher.

Bundling also simplifies claims handling. If a storm knocks down a tree that damages both your roof and your car, having a single point of contact can speed up the process and reduce paperwork. For a deeper dive into the benefits of bundling, check out Homeowners Insurance and Car Insurance Bundle: Save Money & Simplify Coverage.

Choosing the Right Coverage for Your Texas Home

Texas homes vary widely—from coastal ranches in Galveston to modern condos in Austin. Your coverage needs should reflect that diversity. Here are the core components to look for:

- Dwelling Coverage (Coverage A): Replaces the structure itself. Make sure the limit matches the cost to rebuild, not just market value.

- Personal Property (Coverage C): Protects belongings. Consider an “actual cash value” policy for lower premiums, or “replacement cost” for full reimbursement.

- Liability Protection (Coverage E): Covers legal costs if someone is injured on your property.

- Additional Living Expenses (ALE): Pays for temporary housing if your home becomes uninhabitable after a covered loss.

- Endorsements for Specific Risks: Windstorm, hail, and earthquake (rare but possible in West Texas) are optional add‑ons you might need.

Don’t forget to review your policy annually. Renovations, new purchases, or changes in local building codes can affect the amount of coverage you truly need.

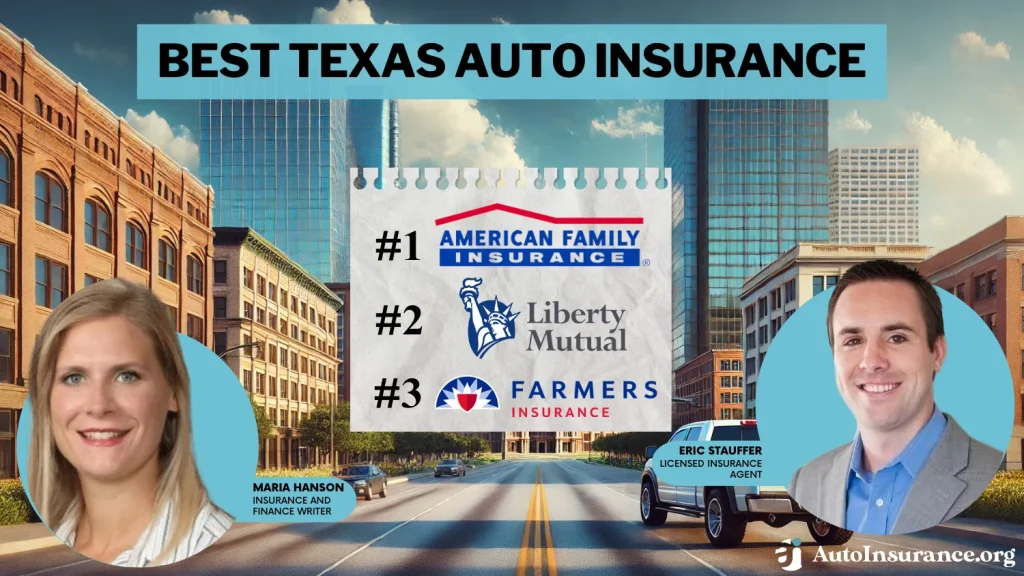

Getting the Best Auto Insurance in the Lone Star State

Texas drivers enjoy a relatively low cost of living, but auto insurance can still be pricey due to factors like high traffic density, a large uninsured driver population, and the state’s “no-fault” approach to certain claims. Here’s how to navigate the market:

- Shop Around: Use comparison tools to get at least three quotes. For a step‑by‑step approach, read How to Get Multiple Auto Insurance Quotes – A Step‑by‑Step Guide.

- Consider Usage‑Based Insurance: Telematics programs can lower rates for safe drivers, especially if you log low mileage.

- Leverage Discounts: Good driver, multi‑policy, anti‑theft device, and even military discounts are common.

- Review Liability Limits: While Texas’s minimum is 30/60/25, many experts recommend higher limits—especially if you have significant assets.

- Understand Uninsured/Underinsured Motorist Coverage: Texas has a high rate of uninsured drivers; this coverage protects you in case you’re hit by one.

If you own a business vehicle, there are special considerations. The article Cheap Car Insurance for Business Use: Save Money & Stay Covered explains how commercial policies differ and where you can save.

Factors That Influence Premiums in Texas

Understanding why your premium looks the way it does can empower you to make adjustments. Some of the most influential factors include:

- Location: Urban areas like Houston and Dallas have higher rates due to traffic density and crime statistics.

- Home Construction: Brick homes often receive lower windstorm premiums than wood‑frame houses.

- Driving Record: Tickets, accidents, and DWI convictions dramatically raise auto rates.

- Credit Score: Texas insurers may use credit-based insurance scores to set premiums.

- Claims History: Frequent past claims suggest higher future risk.

For a broader view of how premiums are calculated across insurance types, revisit the fundamentals in Why Do Insurance Companies Charge Premiums? Understanding the Basics.

Tips to Reduce Your Home and Auto Insurance Costs in Texas

Saving money isn’t just about finding the cheapest policy; it’s about optimizing coverage to match your risk profile. Here are actionable steps you can take:

1. Bundle Policies

As mentioned earlier, a multi‑policy discount can shave off a significant chunk of your premium. Talk to your current insurer about bundle options before you shop elsewhere.

2. Raise Your Deductibles

If you have an emergency fund, increasing the deductible on both home and auto policies can lower monthly costs. Just be sure you can cover the out‑of‑pocket amount if a claim arises.

3. Install Safety Devices

Security systems, smoke detectors, and deadbolts can lower home premiums. For autos, anti‑theft devices and advanced driver‑assist features (like lane‑keep assist) can earn discounts.

4. Review Coverage Annually

Life changes—new kids, a home remodel, or a new vehicle—should trigger a policy review. Dropping unnecessary riders or adjusting limits can keep premiums in check.

5. Take Advantage of State Programs

Texas offers the Texas Windstorm Insurance Association (TWIA) for residents in high‑risk wind zones. While it’s not a discount, it provides a more affordable option than private insurers for wind damage.

6. Maintain a Clean Driving Record

Safe driving is rewarded. Enroll in defensive driving courses if you’re eligible; some insurers give point reductions on your policy.

Special Considerations for Texas Residents

Every state has its quirks, and Texas is no exception. Here are a few region‑specific nuances you should keep in mind when selecting home and auto insurance:

- Hailstorms in Central Texas: The Dallas‑Fort Worth area sees frequent hail. Ensure your auto policy includes comprehensive coverage for hail damage, and consider a windstorm endorsement for your home.

- Coastal Flood Risks: If you live near the Gulf Coast, standard homeowners policies won’t cover flood. Purchase a separate NFIP flood policy.

- Rural Property Issues: Many rural Texans have mobile homes or manufactured homes. These often require specialized policies—look for “manufactured home” coverage.

- High‑Value Vehicles: Luxury cars, trucks, and classic models may need higher limits or agreed‑value coverage. Discuss these specifics with your auto insurer.

- Insurance Fraud Awareness: Texas has a higher than average rate of staged accidents. Choose an insurer with strong fraud detection and a clear claims process.

How to File a Claim Effectively

Even with the best precautions, you may need to file a claim at some point. Here’s a streamlined process to make it as painless as possible:

- Document the Damage: Take photos, videos, and write notes immediately after the incident.

- Contact Your Insurer Promptly: Most policies require notification within a certain timeframe—usually 24‑48 hours for auto, 30 days for home.

- Gather Supporting Documents: Police reports for auto accidents, repair estimates for home damage, and any receipts for personal property losses.

- Work With the Adjuster: Be honest and thorough. Provide all requested information to avoid delays.

- Review Settlement Offers: Ensure the payout covers repair or replacement costs. Don’t hesitate to negotiate if you feel the offer is low.

Having a clear understanding of the claims process can reduce stress, especially after a natural disaster—a reality for many Texans.

Future Trends in Texas Home and Auto Insurance

Insurance is an evolving industry, and Texas is at the forefront of several emerging trends:

- Usage‑Based Auto Policies: Telematics devices are becoming standard, rewarding low‑mileage drivers with lower rates.

- Parametric Insurance for Weather Events: Some insurers are experimenting with payout models based on measurable triggers—like wind speed—rather than traditional loss assessments.

- Increased Emphasis on Cyber Coverage: Smart homes and connected cars bring new risks; many carriers now offer cyber endorsements for both property and vehicles.

- Climate‑Adapted Pricing: As extreme weather patterns intensify, insurers are adjusting premiums to reflect higher risk zones, especially for wind and flood.

Staying informed about these trends can help you anticipate changes in your policy costs and coverage options.

In the end, securing reliable home and auto insurance in Texas is about balancing protection with affordability. By understanding state regulations, leveraging bundling discounts, and staying proactive about risk mitigation, you’ll be well positioned to protect your home, your vehicle, and your peace of mind for years to come.