Table of Contents

- Why You Should Get Pre Approved for VA Home Loan

- Steps to Get Pre Approved for VA Home Loan

- Eligibility Requirements for VA Home Loan Pre‑Approval

- Understanding Your Entitlement

- Gathering the Right Documents

- Choosing the Right Lender

- Benefits of VA Loan Pre‑Approval

- Tips to Strengthen Your Pre‑Approval Application

- Common Pitfalls and How to Avoid Them

- Frequently Asked Questions

- Can I get a VA loan if I have a low credit score?

- Do I need to pay a down payment?

- What is the VA funding fee?

- Can I use a VA loan to buy a condo?

- How long does the pre‑approval process take?

- From Pre‑Approval to Closing: What Happens Next?

Buying a home is a big milestone, and if you’re a veteran or an active‑duty service member, the VA home loan program can make that milestone a lot easier. One of the smartest first moves you can make is to get pre approved for VA home loan financing before you even start house hunting. Why? A pre‑approval not only shows sellers that you’re serious, it also gives you a clear picture of how much house you can afford, and it speeds up the closing process when you find the right property.

Many veterans think the VA loan is a mystery wrapped in paperwork, but the reality is that the process is fairly straightforward once you know what to expect. From confirming your eligibility to gathering the right documents, each step builds confidence and reduces surprises later on. In this guide we’ll walk you through everything you need to do to get pre approved for VA home loan success, with practical tips, common pitfalls to avoid, and a few insider tricks that lenders love.

Ready to turn the “American Dream” into a reality with the help of your service benefits? Let’s dive in.

Why You Should Get Pre Approved for VA Home Loan

Getting pre approved for a VA home loan does more than just give you a number. It equips you with bargaining power, speeds up the underwriting timeline, and protects you from falling in love with a house that’s out of reach. Lenders use the pre‑approval to run a quick credit check, verify your income, and confirm your VA entitlement. Once that’s done, you’ll receive a pre‑approval letter that you can attach to any offer you make, letting sellers know you have the financing ready to go.

Besides the obvious advantage of stronger offers, a pre‑approval also helps you avoid last‑minute surprises. For example, if your debt‑to‑income ratio is higher than you thought, you’ll learn that early and can either adjust your budget or work on paying down debt before you start the house‑hunting marathon.

Steps to Get Pre Approved for VA Home Loan

- Confirm Your Eligibility: Verify your service record through the VA’s eBenefits portal or request a Certificate of Eligibility (COE).

- Check Your Credit Score: A higher score can get you better rates, even though VA loans are more forgiving than conventional mortgages.

- Gather Financial Documents: Pay stubs, W‑2s, tax returns, and bank statements are typically required.

- Choose a VA‑Savvy Lender: Not all lenders are equally experienced with VA loans. Some, like Rocket Mortgage, specialize in them – see the article Does Rocket Mortgage Do VA Loans? A Complete Guide for more details.

- Submit a Pre‑Approval Application: Provide the documents, let the lender run a credit pull, and wait for the pre‑approval letter.

- Review the Letter: Make sure the loan amount, interest rate, and any conditions are clearly stated.

Following these steps will put you in a strong position to get pre approved for VA home loan financing quickly and confidently.

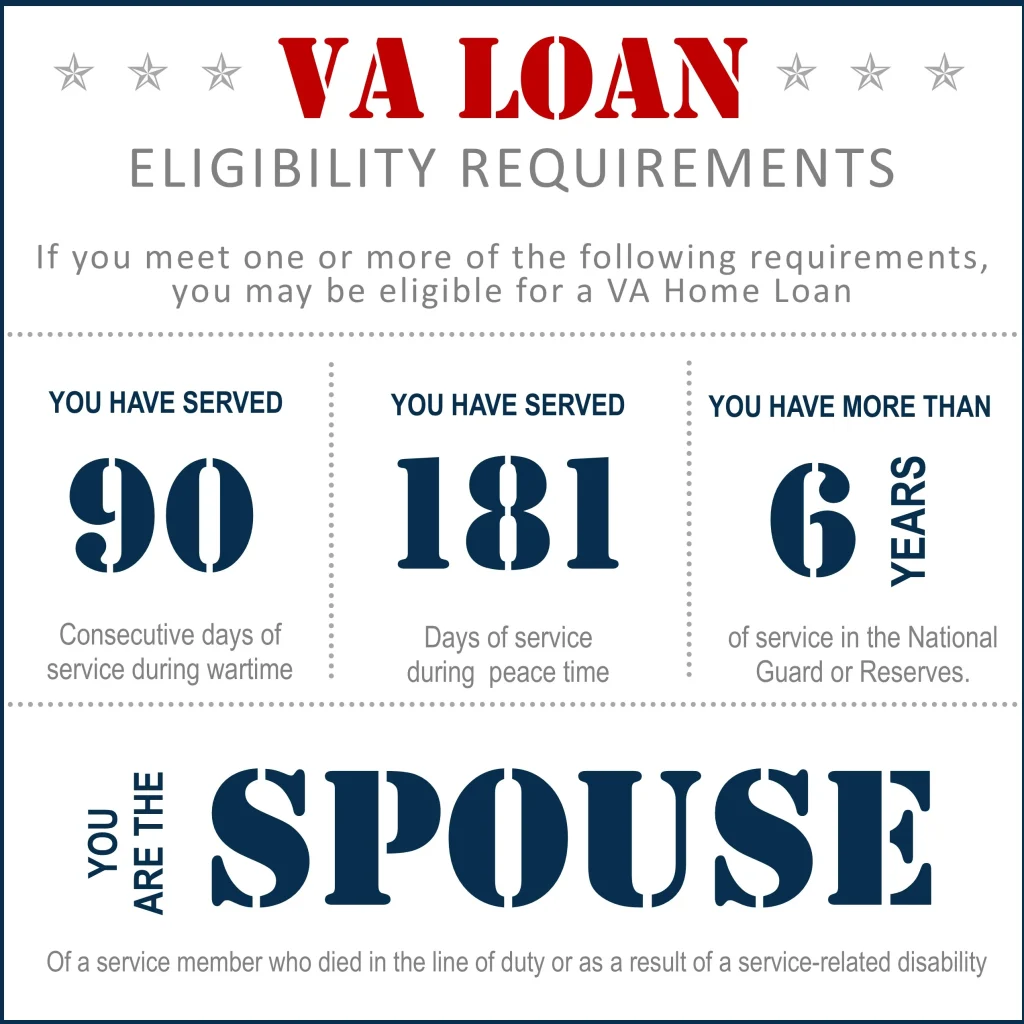

Eligibility Requirements for VA Home Loan Pre‑Approval

The first gate to clear when you want to get pre approved for VA home loan is eligibility. The VA offers this benefit to:

- Veterans who served at least 90 consecutive days of active duty during wartime, or 181 days during peacetime.

- Members of the National Guard and Reserve who have completed at least six years of service.

- Surviving spouses of service members who died in the line of duty or as a result of a service‑connected disability.

If you meet one of these criteria, you can request a Certificate of Eligibility (COE) through the VA’s eBenefits portal or ask your lender to obtain it on your behalf. The COE is the key document lenders look for when you want to get pre approved for VA home loan financing.

Understanding Your Entitlement

VA loans are partially guaranteed by the Department of Veterans Affairs, and the amount you can borrow without a down payment is based on your entitlement. Your basic entitlement is usually $36,000, but most lenders allow you to borrow up to four times that amount (up to $144,000) without a down payment, depending on the county loan limits. If you’ve used your entitlement before, you might still have remaining entitlement that can be restored after you sell the previous home or pay off the loan.

Gathering the Right Documents

When you decide to get pre approved for VA home loan, the paperwork is the next big hurdle. Having everything ready speeds up the process and shows lenders you’re organized. Below is a checklist of the most common documents you’ll need:

- Certificate of Eligibility (COE)

- Government‑issued ID (driver’s license or passport)

- Recent pay stubs (last 30 days)

- Two years of W‑2 forms and tax returns

- Bank statements (last two months)

- Proof of any additional income (bonuses, commissions, or military allowances)

- Debt statements (student loans, credit cards, auto loans)

If you’re self‑employed, expect to provide profit‑and‑loss statements and possibly a year‑to‑date balance sheet. For those who have recently changed jobs, a letter of employment verification can smooth the path to get pre approved for VA home loan.

Choosing the Right Lender

Not all lenders treat VA loans the same way. Some may offer lower fees, while others might have more flexible underwriting criteria. When you’re looking to get pre approved for VA home loan, consider the following:

- Experience with VA Loans: A lender who regularly processes VA loans will understand the nuances of entitlement, funding fees, and property eligibility.

- Interest Rates and Fees: Compare the APR, origination fees, and any VA funding fee waivers (e.g., for veterans with service‑connected disabilities).

- Customer Service: Quick responses and clear explanations can make the pre‑approval journey less stressful.

If you’re also interested in financing a business venture, you might want to explore Small Business Loans for Construction Company – Your Complete Guide, which can be a useful side‑track for veteran entrepreneurs.

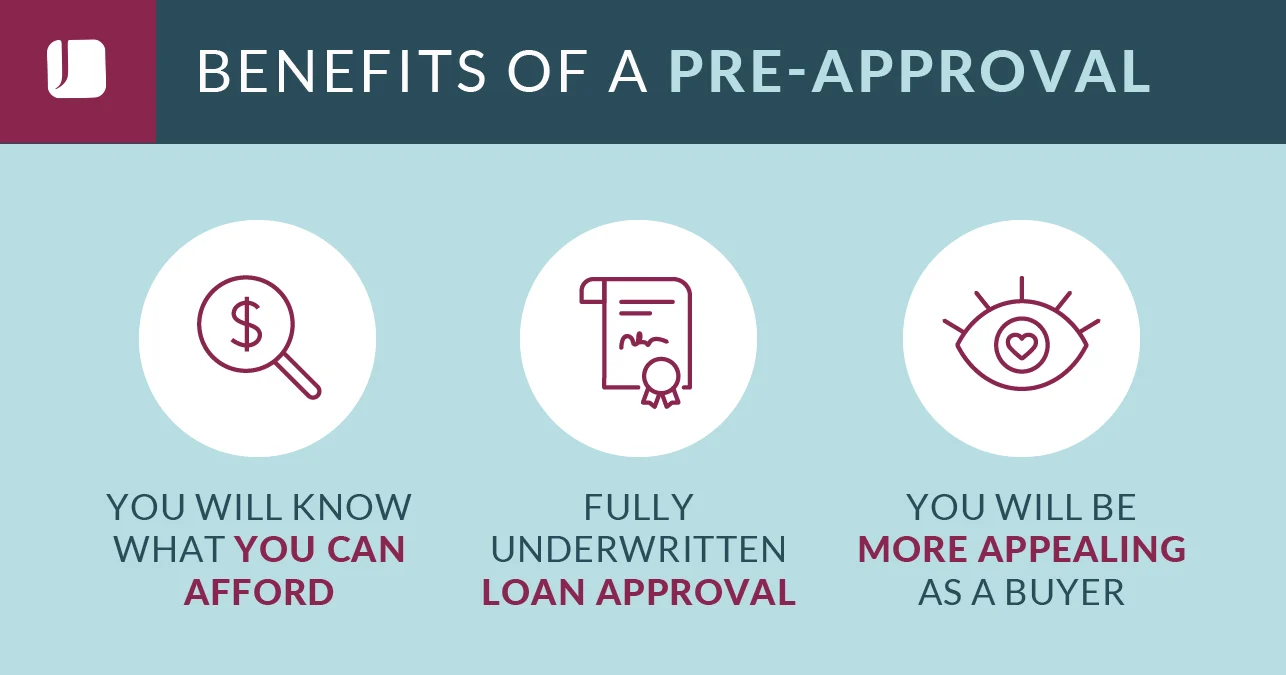

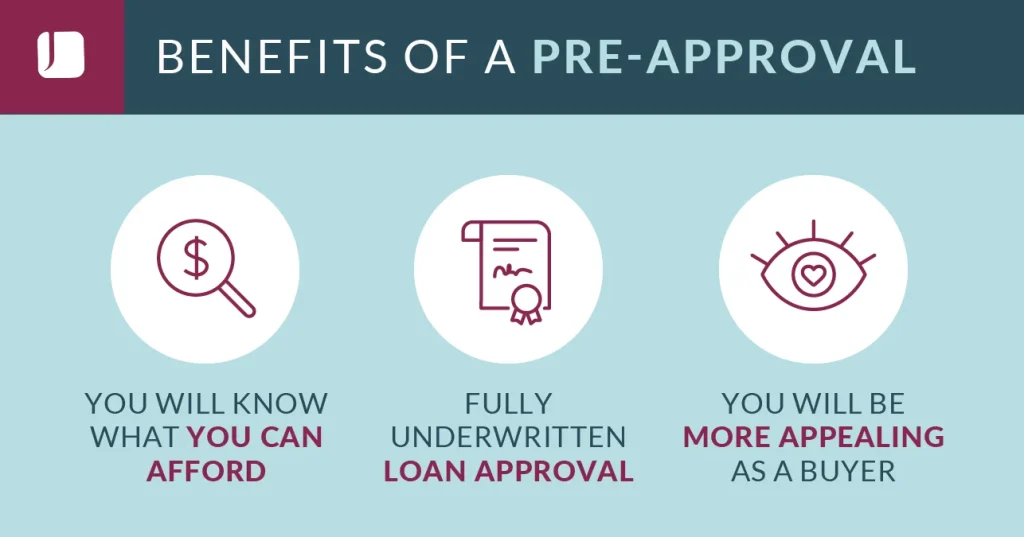

Benefits of VA Loan Pre‑Approval

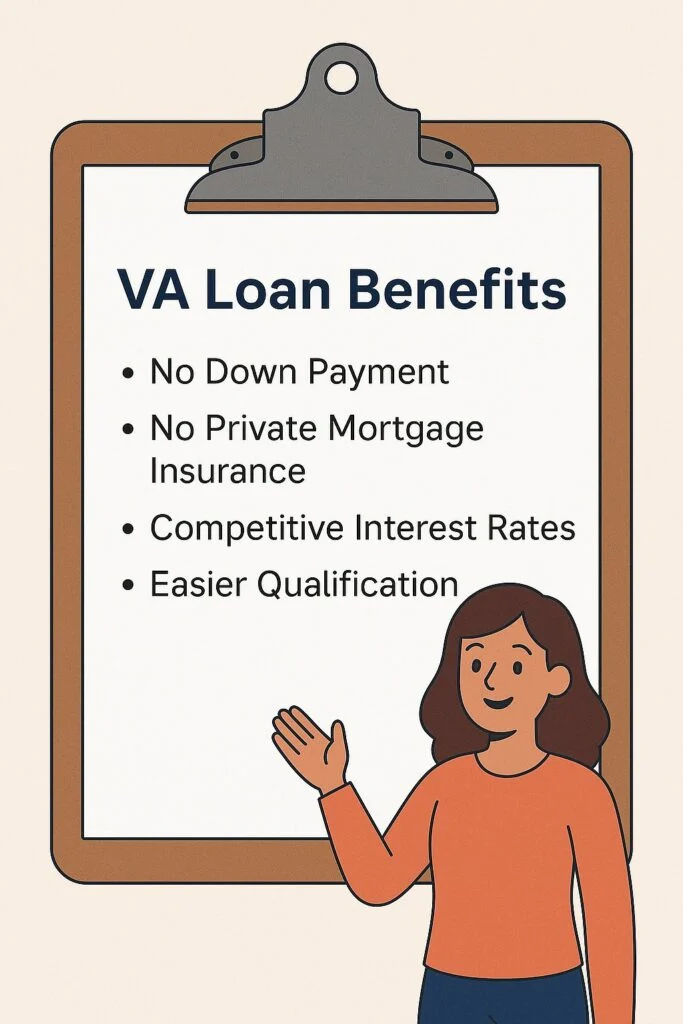

While the VA loan program already offers generous benefits—no down payment, no private mortgage insurance (PMI), and competitive interest rates—being pre‑approved adds an extra layer of advantage:

- Stronger Negotiating Position: Sellers often prefer offers backed by a pre‑approval letter because it reduces the risk of financing falling through.

- Faster Closing: Since the lender has already verified your income and credit, the final approval stage moves quickly once you sign a purchase contract.

- Clear Budget: You know exactly how much you can borrow, which helps you focus on homes within your price range.

- Potential Rate Locks: Some lenders allow you to lock in an interest rate at the time of pre‑approval, protecting you from market fluctuations.

Tips to Strengthen Your Pre‑Approval Application

- Pay down high‑interest credit card balances before applying.

- Keep your job history stable for at least two years, if possible.

- Save a small cushion of cash (even though PMI isn’t required) to demonstrate financial resilience.

- Ask the lender about any available fee reductions for veterans with service‑connected disabilities.

Common Pitfalls and How to Avoid Them

Even though the VA loan process is veteran‑friendly, there are a few traps that can delay or jeopardize your chance to get pre approved for VA home loan:

- Outdated COE: Always request the most recent Certificate of Eligibility; an outdated one can cause unnecessary back‑and‑forth with the lender.

- Unexplained Credit Inquiries: Multiple credit pulls in a short period can lower your score. Consolidate your applications within a 45‑day window to minimize impact.

- Ignoring Debt‑to‑Income Ratio: VA loans still look at your DTI. Aim for a ratio below 41% to stay comfortably within most lenders’ guidelines.

- Choosing a Property That Doesn’t Qualify: The VA has specific property standards. A home with major structural issues may not be eligible for financing.

If you’re uncertain about any of these issues, a quick read of Business Loans Based on Cash Flow – A Complete Guide can give you perspective on how lenders assess financial health beyond the VA loan program.

Frequently Asked Questions

Can I get a VA loan if I have a low credit score?

Yes. While the VA itself does not set a minimum credit score, most lenders prefer a score of 620 or higher. If your score is lower, you may still qualify but could face higher interest rates.

Do I need to pay a down payment?

One of the biggest advantages of a VA loan is that you can finance 100% of the purchase price, meaning no down payment is required (subject to the loan limit in your area).

What is the VA funding fee?

The funding fee helps offset the cost of the VA loan program to taxpayers. It ranges from 1.4% to 3.6% of the loan amount, depending on factors like down payment size, first‑time use, and service‑connected disability status. Certain veterans may be exempt.

Can I use a VA loan to buy a condo?

Yes, as long as the condo association is VA‑approved. The approval list can be verified through the VA’s website or by asking your lender.

How long does the pre‑approval process take?

Typically, once you submit all required documents, a lender can issue a pre‑approval letter within 24‑48 hours. However, the timeline can extend if additional verification is needed.

From Pre‑Approval to Closing: What Happens Next?

After you get pre approved for VA home loan and make an offer, the lender will move into the underwriting phase. This includes a property appraisal (the VA appraisal) to confirm the home meets safety, soundness, and marketability standards. Assuming the appraisal is satisfactory, the lender will issue a final loan approval, and you’ll proceed to closing.

At closing, you’ll sign the loan documents, pay any closing costs not covered by the seller, and the VA funding fee (unless waived). Once everything is signed and recorded, the home is yours!

Remember, the journey from pre‑approval to homeownership is smoother when you stay organized, maintain communication with your lender, and keep an eye on any additional documentation that may be requested. By following the steps outlined above, you’ll be well on your way to successfully get pre approved for VA home loan and enjoy the pride of owning a home built on the foundation of your service.

Congratulations on taking this important step. With the right preparation, the VA home loan can be a powerful tool to help you achieve your home‑ownership goals.