Table of Contents

- Understanding the Basics of Applying for a VA Mortgage Loan

- Eligibility Checklist When Applying for a VA Mortgage Loan

- Step‑by‑Step Process for Applying for a VA Mortgage Loan

- 1. Get Your Certificate of Eligibility (COE)

- 2. Choose a VA‑Savvy Lender

- 3. Pre‑Qualify or Get Pre‑Approved

- 4. Gather Required Documentation

- 5. Home Search and Offer

- 6. VA Appraisal and Inspection

- 7. Underwriting and Final Approval

- 8. Closing the Loan

- Tips to Smooth the Process When Applying for a VA Mortgage Loan

- Start Early with Your COE

- Watch Your Debt‑to‑Income Ratio

- Consider a VA Funding Fee Waiver

- Shop Around for Lender Fees

- Leverage the VA’s Energy Efficiency Incentives

- Common Misconceptions About Applying for a VA Mortgage Loan

- Myth 1: You Must Have Perfect Credit

- Myth 2: The VA Loan Is Only for Primary Residences

- Myth 3: You Can’t Use a VA Loan After a Divorce

- Myth 4: The VA Funding Fee Is Mandatory for All Borrowers

- Refinancing Options for VA Mortgage Loan Borrowers

- VA Interest‑Rate Reduction Refinance Loan (IRRRL)

- Cash‑Out Refinance

- Final Thoughts on Applying for a VA Mortgage Loan

Buying a home is a big milestone, and for veterans and active‑duty service members, the VA mortgage loan program can turn that milestone into a reality with fewer hurdles and lower costs. Unlike conventional mortgages, a VA loan doesn’t require a down payment, private mortgage insurance (PMI), or a perfect credit score, but the process still involves paperwork, timing, and a clear understanding of the rules. Whether you’re a first‑time homebuyer or a seasoned homeowner looking to refinance, knowing how to navigate the application process is essential.

In this article we’ll walk through every stage of applying for a VA mortgage loan, from confirming eligibility to closing the deal. You’ll learn which documents you’ll need, how to choose the right lender, and practical tips to boost your chances of approval. Along the way, we’ll sprinkle in a few useful links to related guides—like how to pre‑qualify for a VA home loan or refinance student loans—so you can get a broader picture of your financing options.

Ready to turn your VA benefits into a set of house keys? Let’s dive in.

Understanding the Basics of Applying for a VA Mortgage Loan

The VA mortgage loan program, administered by the U.S. Department of Veterans Affairs, is designed to help eligible veterans, active‑duty service members, National Guard and Reserve personnel, and surviving spouses purchase, build, or refinance a home. The core advantages include:

- No down payment required (subject to loan limits).

- No private mortgage insurance (PMI) premiums.

- Limited closing costs and the ability to roll some fees into the loan.

<liCompetitive interest rates compared to conventional loans.

Even with these perks, the application process still follows many of the same steps as a conventional mortgage, plus a few VA‑specific requirements. That’s why it’s crucial to start with a solid foundation: confirming your eligibility and gathering the right paperwork.

Eligibility Checklist When Applying for a VA Mortgage Loan

- Service Requirements: Typically 90 consecutive days of active duty during wartime, 181 days during peacetime, or 6 years in the National Guard/Reserve. Surviving spouses of service members who died in combat or due to a service‑connected disability may also qualify.

- Certificate of Eligibility (COE): This is your official proof of eligibility. You can obtain it online through the VA’s eBenefits portal, by mail, or through your lender.

- Credit Score: While the VA doesn’t set a minimum score, most lenders look for at least 620–640 for conventional financing.

- Debt‑to‑Income (DTI) Ratio: Ideally below 41%, though some lenders can go higher with compensating factors.

- Property Requirements: The home must meet the VA’s Minimum Property Requirements (MPRs) to ensure it’s safe, structurally sound, and sanitary.

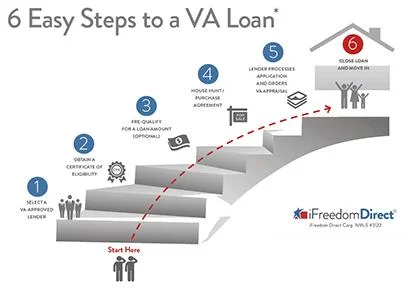

Step‑by‑Step Process for Applying for a VA Mortgage Loan

Now that you know you’re eligible, let’s break down the actual application journey. Each step builds on the previous one, so staying organized can save you weeks of back‑and‑forth.

1. Get Your Certificate of Eligibility (COE)

The COE is the cornerstone of any VA loan application. Most lenders can request it on your behalf through the VA’s web portal, but you can also pull it yourself at eBenefits. Once you have the COE, keep a digital copy handy—many lenders will ask to upload it during the loan submission.

2. Choose a VA‑Savvy Lender

Not every mortgage lender has experience with VA loans. Look for lenders who:

- Hold a VA‑approved status.

- Offer competitive VA loan rates and low closing costs.

- Provide a dedicated loan officer familiar with VA guidelines.

Tip: If you’re also interested in refinancing other debt, you might find a lender that bundles a VA mortgage with a business loan or a student‑loan refinance option. This can simplify paperwork and sometimes lower overall rates.

3. Pre‑Qualify or Get Pre‑Approved

Before you start house hunting, it’s smart to get pre‑qualified or pre‑approved. Pre‑qualification is a quick estimate based on self‑reported income, while pre‑approval involves a full credit check and document review. A pre‑approval letter shows sellers you’re serious and financially ready.

For a deeper dive on this step, check out our guide on how to prequalify for a VA home loan. It walks you through the exact documents lenders typically request.

4. Gather Required Documentation

While the exact list can vary by lender, most will ask for:

- Recent pay stubs (last 30 days).

- Two years of W‑2 forms or tax returns if self‑employed.

- Bank statements (last two months) to verify assets.

- Proof of military service (COE, DD214, or statement of service).

- Debt statements (credit cards, student loans, auto loans).

If you have existing student loans, you might also want to explore refinancing student loans without a degree to improve your DTI ratio before applying.

5. Home Search and Offer

With pre‑approval in hand, you can start viewing homes that meet VA’s Minimum Property Requirements. Once you find a property you love, submit an offer that includes a VA appraisal contingency. This protects you if the property doesn’t meet VA standards or appraises below the purchase price.

6. VA Appraisal and Inspection

The VA will order its own appraisal to confirm the home’s value and compliance with MPRs. While the VA appraisal covers safety and livability, you should still order a private home inspection to uncover any hidden issues.

7. Underwriting and Final Approval

After the appraisal, the lender’s underwriter reviews all documentation, the appraisal report, and the title work. They’ll verify that the loan meets both VA guidelines and the lender’s internal policies. This is often the longest phase, but staying responsive to any requests for additional documents can keep things moving.

8. Closing the Loan

At closing, you’ll sign the mortgage note, the deed of trust, and other legal documents. You’ll also pay any closing costs not covered by the VA (often lenders allow you to roll these into the loan). After the paperwork is recorded, the home is officially yours.

Tips to Smooth the Process When Applying for a VA Mortgage Loan

Even with the benefits of a VA loan, a few pitfalls can slow you down. Below are practical tips drawn from years of experience with veteran borrowers.

Start Early with Your COE

Getting the Certificate of Eligibility can sometimes take a week or more, especially during peak periods. Request it as soon as you start house hunting to avoid bottlenecks.

Watch Your Debt‑to‑Income Ratio

Even though the VA is forgiving on credit scores, a high DTI can still raise red flags. Pay down credit cards or consider consolidating high‑interest debt before you apply. A lower DTI not only helps approval odds but may also secure you a better interest rate.

Consider a VA Funding Fee Waiver

If you’re a disabled veteran, you may be eligible for a waiver of the VA funding fee—a one‑time charge that ranges from 1.4% to 3.6% of the loan amount. Submit your disability documentation along with the loan application to claim the exemption.

Shop Around for Lender Fees

While interest rates are often comparable across lenders, closing costs can vary widely. Ask for a Good‑Faith Estimate (GFE) from at least three VA‑approved lenders and compare items like origination fees, underwriting fees, and third‑party costs.

Leverage the VA’s Energy Efficiency Incentives

If you’re buying a home that could benefit from energy‑saving upgrades, the VA offers incentives that can be rolled into the loan. Talk to your lender about the VA’s Energy Efficient Mortgage (EEM) program to see if you qualify.

Common Misconceptions About Applying for a VA Mortgage Loan

Because the VA loan program is unique, many myths circulate in the veteran community. Let’s clear up a few of the most common misunderstandings.

Myth 1: You Must Have Perfect Credit

False. While a higher credit score can lead to better rates, the VA does not set a minimum score. Many lenders will work with borrowers in the low‑600s, especially if they have strong employment history and low DTI.

Myth 2: The VA Loan Is Only for Primary Residences

Correct. The VA loan can be used for a primary home, a second home, or even a multi‑unit property (up to four units) as long as you occupy one of the units as your primary residence.

Myth 3: You Can’t Use a VA Loan After a Divorce

In many cases, you can. If your former spouse was the eligible veteran and the loan was assumed, you may be able to keep the loan. However, you’ll need to meet credit and income qualifications independently.

Myth 4: The VA Funding Fee Is Mandatory for All Borrowers

Not true. As mentioned earlier, disabled veterans, surviving spouses, and those who have already paid the fee on a previous VA loan may be exempt.

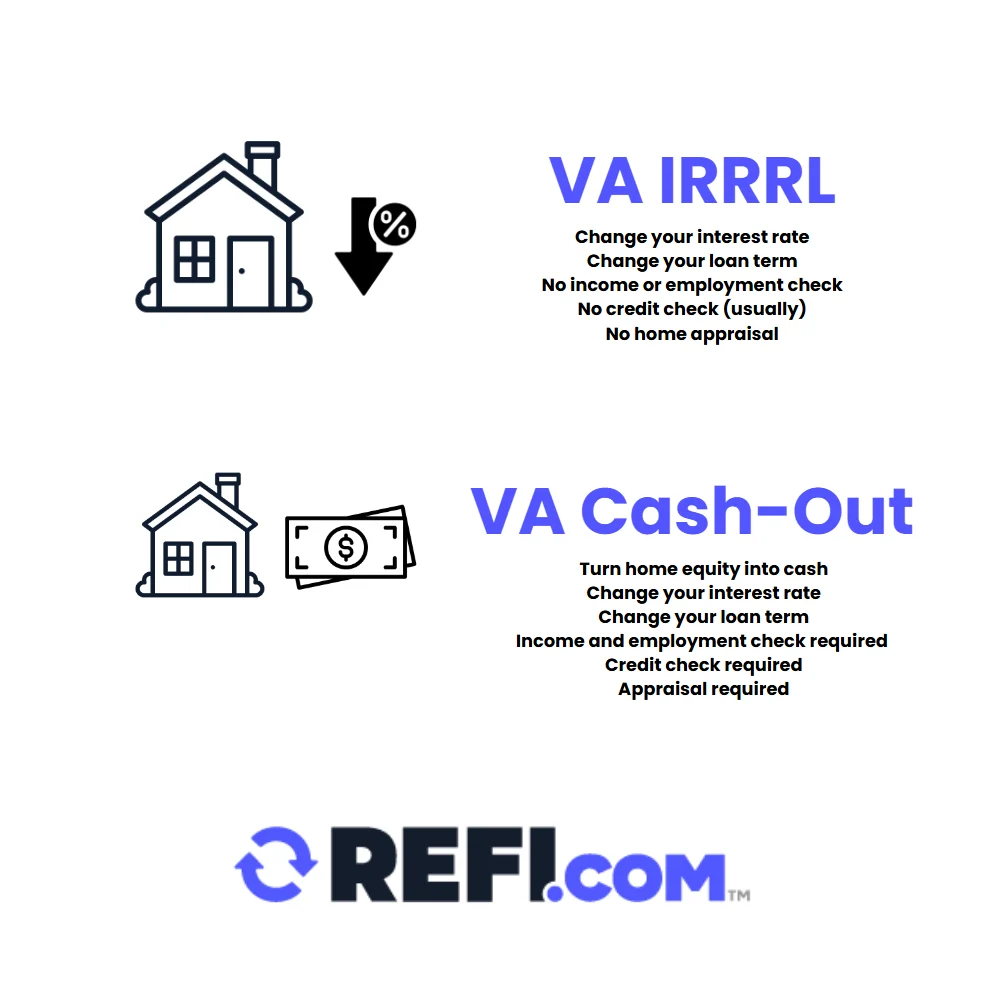

Refinancing Options for VA Mortgage Loan Borrowers

Even after you’ve secured your VA loan, life changes—like a lower interest rate environment or a need to tap home equity—can make refinancing appealing.

VA Interest‑Rate Reduction Refinance Loan (IRRRL)

Often called a “VA streamline refinance,” the IRRRL allows you to refinance into a lower rate with minimal paperwork and no appraisal, as long as the new loan is for the same property and the borrower remains eligible.

Cash‑Out Refinance

If you’ve built equity, a VA cash‑out refinance lets you pull out up to 15% of the home’s value (up to 20% for certain veterans). This can be a smart way to finance home improvements, pay off high‑interest debt, or fund a college tuition.

Before you decide, compare the costs of a cash‑out refinance with other options, like a home equity line of credit (HELOC). For a broader perspective on using home equity, see our article on applying for a home equity loan.

Final Thoughts on Applying for a VA Mortgage Loan

Applying for a VA mortgage loan can feel like navigating a maze, but with the right preparation, the journey is smoother than most people expect. Start by confirming your eligibility and obtaining the COE, then partner with a lender who knows the VA’s nuances. Keep your financial profile tidy—pay down debts, gather documentation early, and be ready for the appraisal process.

Remember, the VA loan’s greatest strength is its flexibility: no down payment, no PMI, and generous terms that honor your service. By following the steps outlined above and staying proactive, you’ll be well on your way to turning that “For Sale” sign into a place you can truly call home.