Table of Contents

- How to prequalify for a VA home loan

- Steps to prequalify for a VA home loan

- Understanding VA entitlement and loan limits

- Credit score requirements for VA prequalification

- Income documentation you’ll need

- Common pitfalls and how to avoid them

- What to expect after prequalification

- Tips for a smoother VA loan prequalification experience

Buying a home is a big milestone, and for veterans the VA loan program can make that dream more attainable. But before you start scrolling through listings, you’ll want to know whether you can actually secure a loan under the program’s favorable terms. That’s where the process of prequalify for a VA home loan comes into play. Think of it as a quick health check for your mortgage eligibility—it tells you where you stand before you get deep into paperwork.

In this article we’ll walk you through everything you need to know: the documents you’ll gather, the credit score considerations, how the VA’s entitlement works, and the exact steps to take so you can prequalify for a VA home loan with confidence. Whether you’re a first‑time homebuyer or a seasoned homeowner looking to refinance, the guidance here will keep you on the right track.

We’ll also sprinkle in a few practical tips from veterans who’ve been through the process, and we’ll link to other helpful resources on our site so you can keep learning without leaving the page.

How to prequalify for a VA home loan

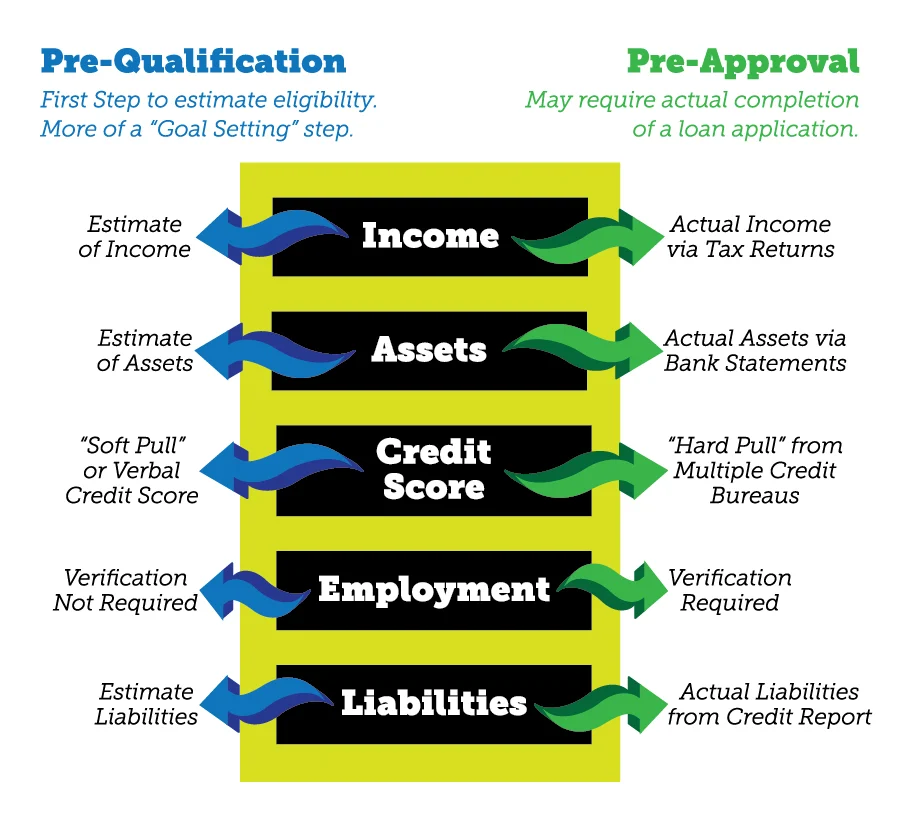

Prequalification is the first informal step in the mortgage journey. Unlike a full loan application, it doesn’t bind you to a lender, but it does give you a realistic snapshot of the loan amount you might qualify for. For VA loans, this step is especially useful because the Department of Veterans Affairs uses a unique “entitlement” system that can affect how much you can borrow.

Below is a straightforward roadmap you can follow to prequalify for a VA home loan in just a few days.

Steps to prequalify for a VA home loan

- Gather your service verification. The VA requires proof of eligibility—your DD‑214, statement of service, or VA Certificate of Eligibility (COE). You can request the COE online through eBenefits or ask your lender to pull it for you.

- Check your credit report. A solid credit history makes the prequalification smoother. If you have questions about how student loans affect your score, our article on Does Student Loan Appear on Credit Report? explains the details.

- Calculate your debt‑to‑income (DTI) ratio. Lenders typically look for a DTI under 41%, though the VA can be flexible if you have strong compensating factors.

- Determine your VA entitlement. Most borrowers have a basic entitlement of $36,000, but you can have additional entitlement based on your previous use of the benefit.

- Choose a VA‑approved lender. Not all lenders specialize in VA loans. Working with a lender experienced in the program can speed up the prequalification and reduce potential hiccups.

- Submit a short prequalification form. This usually includes your income, employment history, and a brief credit check. Some lenders even offer an instant online prequalification tool.

- Receive a prequalification letter. This letter states the loan amount you’re likely eligible for and can be shown to real‑estate agents to strengthen your buying position.

Once you have that letter in hand, you’re ready to start house hunting with a realistic budget. Remember, prequalification is not a guarantee—final approval will require full documentation and underwriting.

Understanding VA entitlement and loan limits

The VA’s entitlement is the amount the government guarantees to the lender, which reduces the lender’s risk. In most cases, the basic entitlement is $36,000, but the VA also calculates a “maximum entitlement” based on county loan limits. This means you can often borrow well above $200,000 without a down payment, as long as the total loan amount stays within the county’s limit.

If you’ve used your VA benefit before and still have remaining entitlement, you can apply it to a new purchase or refinance. The key is to request a new COE that reflects your current entitlement status. For a deeper dive into the entitlement calculation, check out our complete guide to VA loan prequalification.

Credit score requirements for VA prequalification

One of the biggest myths about VA loans is that they don’t care about credit scores. In reality, while the VA itself does not set a minimum score, most lenders follow their own guidelines. Generally, a score of 620 or higher is considered acceptable for prequalification, but a score of 680+ puts you in a stronger negotiating position for better interest rates.

Here are a few credit‑friendly strategies to boost your chances:

- Pay down revolving balances—credit cards and personal loans—so your utilization drops below 30%.

- Correct any errors on your credit report before you apply. A quick dispute can sometimes add 20‑30 points.

- Keep older accounts open; length of credit history positively impacts your score.

If you’re juggling student loans, remember that the VA doesn’t penalize you for them, but they do affect your DTI. Our article on Applying for a VA Home Loan: Complete Guide & Tips discusses how to balance those obligations.

Income documentation you’ll need

During the prequalification phase, lenders typically ask for a snapshot of your income. This can include:

- Recent pay stubs (last 30 days)

- W‑2 forms from the past two years

- If self‑employed, a profit‑and‑loss statement and tax returns

- Proof of any additional income—bonuses, overtime, or rental income

Having these documents ready speeds up the prequalification process and shows the lender that you’re organized and serious about buying.

Common pitfalls and how to avoid them

Even though the VA loan program is veteran‑friendly, certain mistakes can derail your prequalification:

- Skipping the COE request. Without a verified Certificate of Eligibility, lenders can’t move forward.

- Overlooking debt obligations. All recurring debts—car loans, credit cards, even alimony—are factored into your DTI.

- Assuming you’ll get a zero‑down loan. While many VA loans require no down payment, if the purchase price exceeds the county loan limit you may need a down payment to cover the difference.

- Choosing a lender unfamiliar with VA nuances. Some lenders may try to push you into a conventional loan that doesn’t offer the same benefits.

By staying aware of these issues, you can keep the prequalification process smooth and avoid unnecessary delays.

What to expect after prequalification

Once you receive your prequalification letter, the next steps are:

- House hunting. Use the loan amount on your letter as a budget ceiling.

- Make an offer. Include a clause that the sale is contingent on VA loan approval.

- Formal loan application. Submit the full paperwork, including the COE, credit report, and detailed income verification.

- VA appraisal. The VA will order an appraisal to ensure the property meets minimum safety and market value standards.

- Closing. After underwriting clears, you’ll sign the closing documents and take ownership of the home.

Remember, prequalification is just the first checkpoint. It gives you confidence, but the final loan approval will still require a full underwriting process.

Tips for a smoother VA loan prequalification experience

- Stay in touch with your lender. Promptly provide any additional documents they request.

- Maintain stable employment. Frequent job changes can raise red flags during underwriting.

- Keep credit inquiries to a minimum. Too many hard pulls within a short period can slightly lower your score.

- Know your entitlement. Understanding how much the VA guarantees helps you negotiate better terms.

Following these tips can turn a simple prequalification into a solid stepping stone toward homeownership.

In the end, the VA loan program remains one of the most generous mortgage options available to veterans. By taking the time to properly prequalify for a VA home loan, you set yourself up for a smoother, less stressful buying experience. Keep your documents organized, stay on top of your credit, and partner with a lender who knows the VA inside and out. With those pieces in place, you’ll be well on your way to opening the door on your new home.