Table of Contents

- Understanding Business Loans for New Small Businesses

- How to Choose the Right Loan for Your Startup

- Assess Your Funding Needs

- Match Loan Type to Cash‑Flow Cycle

- Compare Interest Rates and Fees

- Step‑by‑Step Guide to Securing Business Loans for New Small Businesses

- 1. Clean Up Your Personal and Business Credit

- 2. Prepare a Solid Business Plan

- 3. Gather Required Documentation

- 4. Choose the Right Lender

- 5. Submit Your Application

- 6. Review the Loan Offer

- 7. Close the Deal and Deploy Funds Wisely

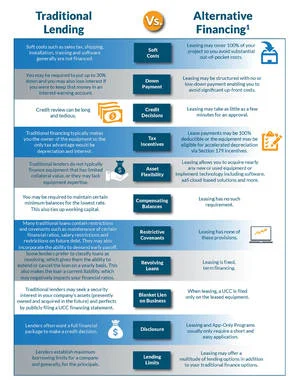

- Alternative Financing Options When Traditional Loans Aren’t Viable

- When to Consider a Business Credit Card

- Common Pitfalls and How to Avoid Them

- Underestimating Total Loan Costs

- Borrowing More Than Needed

- Ignoring the Impact on Personal Credit

- Failing to Keep Records Updated

- Success Stories: How Real Entrepreneurs Leveraged Business Loans for New Small Businesses

- Key Takeaways for New Small Business Owners

Starting a small business is exhilarating, but turning a great idea into a thriving operation often requires a solid infusion of cash. Whether you need to purchase inventory, lease a storefront, or hire that first employee, the right financing can bridge the gap between concept and reality. Yet, many entrepreneurs feel overwhelmed by the myriad of loan products, eligibility criteria, and the paperwork that seems to accompany every application.

In this article we’ll demystify the landscape of business loans for new small businesses. From traditional bank loans to alternative online lenders, we’ll break down the pros and cons, walk you through the application process, and share practical tips to improve your chances of approval. By the end, you’ll have a clear roadmap to fund your venture without getting lost in financial jargon.

Ready to dive in? Let’s explore how you can secure the capital you need, stay financially healthy, and set the foundation for long‑term success.

Understanding Business Loans for New Small Businesses

When we talk about business loans for new small businesses, we’re referring to financing products specifically designed for startups and early‑stage companies. Unlike established firms with extensive credit histories, new entrepreneurs often face tighter lending criteria. However, lenders have adapted by offering flexible options that consider factors beyond just credit scores—such as cash flow projections, business plans, and personal guarantees.

Here’s a quick snapshot of the most common loan types you’ll encounter:

- SBA Microloans: Government‑backed loans up to $50,000, ideal for equipment, working capital, or inventory.

- Traditional Bank Term Loans: Fixed‑rate loans with longer repayment terms, typically requiring strong credit and collateral.

- Online Business Loans: Faster approval, higher interest rates, but less paperwork.

- Business Line of Credit: Revolving credit that lets you draw funds as needed, paying interest only on the amount used.

- Equipment Financing: Loans secured by the equipment you purchase, preserving cash flow for other needs.

How to Choose the Right Loan for Your Startup

Selecting the best financing solution depends on three core factors: the amount you need, how quickly you need it, and how comfortable you are with repayment terms. Below we’ll outline a decision‑making framework to help you align loan features with your business goals.

Assess Your Funding Needs

Before you chase after any loan, sit down with a spreadsheet and map out exactly why you need money. Break down the costs into categories—inventory, marketing, payroll, technology, and emergency reserves. This clarity not only guides your loan search but also strengthens your loan application, because lenders love to see a well‑structured financial plan.

Match Loan Type to Cash‑Flow Cycle

For businesses with seasonal peaks, a line of credit can smooth out cash‑flow gaps, while a term loan works better for one‑time investments like purchasing a storefront or machinery. If you’re unsure, consider a hybrid approach: combine a modest term loan with a revolving line of credit for flexibility.

Compare Interest Rates and Fees

Don’t just look at the advertised interest rate. Calculate the Annual Percentage Rate (APR), which includes origination fees, processing fees, and any prepayment penalties. A lower rate with high fees may end up costing more over the life of the loan.

Step‑by‑Step Guide to Securing Business Loans for New Small Businesses

Now that you understand the landscape, let’s walk through the practical steps you’ll need to take to secure financing.

1. Clean Up Your Personal and Business Credit

Most lenders—especially for business loans for new small businesses—look at both personal and business credit scores. Pay down outstanding credit‑card balances, correct any errors on your credit report, and avoid opening new credit lines right before applying.

2. Prepare a Solid Business Plan

A compelling business plan should include an executive summary, market analysis, competitive landscape, marketing strategy, operational plan, and detailed financial projections (profit‑and‑loss, cash flow, and balance sheet for at least three years). This document shows lenders that you have a clear vision and a realistic path to profitability.

3. Gather Required Documentation

Typical documents include:

- Personal and business tax returns (last 2 years)

- Bank statements (last 6 months)

- Business licenses and registrations

- Legal structure documents (LLC agreement, partnership deed, etc.)

- Financial projections and a detailed use‑of‑funds statement

4. Choose the Right Lender

If you prefer a traditional route, start with banks where you already have a relationship. For faster approvals, explore reputable online lenders that specialize in business loans for new small businesses. Platforms like i need a loan for my business – Complete Guide to Funding Your Venture offer comparison tools that can save you time.

5. Submit Your Application

Complete the application accurately, attach all supporting documents, and be prepared to answer follow‑up questions. Many lenders now use automated underwriting systems that can provide a decision within days.

6. Review the Loan Offer

When you receive an offer, scrutinize the terms: interest rate, repayment schedule, covenants, and any collateral requirements. If something feels off, negotiate or walk away—there are always other options.

7. Close the Deal and Deploy Funds Wisely

After signing the loan agreement, the funds will be disbursed—usually directly to your business bank account. Stick to the budget you presented in your application; lenders often monitor cash flow to ensure you stay on track.

Alternative Financing Options When Traditional Loans Aren’t Viable

Even with a thorough approach, some startups may still struggle to qualify for conventional business loans for new small businesses. In those cases, consider these alternative routes:

- Micro‑Funding Platforms: Websites like Kiva or Fundera let you raise small amounts from a community of lenders.

- Revenue‑Based Financing: Repayments are tied to a percentage of monthly revenue, easing pressure during slower months.

- Angel Investors & Venture Capital: If you have a high‑growth idea, equity financing may be more suitable than debt.

- Crowdfunding: Platforms such as Kickstarter or Indiegogo let you pre‑sell products to fund production.

When to Consider a Business Credit Card

For very short‑term cash needs (e.g., covering a minor inventory purchase), a business credit card can be a convenient bridge. Look for cards offering 0% introductory APR and rewards that align with your spend categories. Just be cautious of high post‑introductory rates.

Common Pitfalls and How to Avoid Them

Even seasoned entrepreneurs can fall into traps when seeking financing. Here are the most frequent mistakes and actionable tips to steer clear.

Underestimating Total Loan Costs

Always calculate the total cost of borrowing, not just the monthly payment. Use loan calculators that factor in interest, fees, and any early‑repayment penalties.

Borrowing More Than Needed

It’s tempting to take the maximum amount offered, but extra debt can strain cash flow. Borrow only what your financial projections justify.

Ignoring the Impact on Personal Credit

Many lenders require a personal guarantee, meaning default could affect your personal credit score. Keep personal and business finances as separate as possible to protect yourself.

Failing to Keep Records Updated

Lenders may request updated financial statements even after the loan is funded. Maintain organized records to avoid surprises during audits or covenant checks.

Success Stories: How Real Entrepreneurs Leveraged Business Loans for New Small Businesses

Seeing real‑world examples can inspire confidence. Here are two brief case studies:

- Emma’s Boutique: Emma used an SBA microloan of $30,000 to lease a downtown space, purchase inventory, and launch a targeted Instagram campaign. Within 12 months, revenue grew 150%, allowing her to refinance with a low‑interest term loan.

- TechStart Labs: A tech startup secured a $75,000 online business loan to develop a prototype and protect intellectual property. The rapid product rollout attracted angel investors, who later provided equity funding for scaling.

Both entrepreneurs emphasized the importance of a clear use‑of‑funds plan and maintaining transparent communication with their lenders.

Key Takeaways for New Small Business Owners

Securing business loans for new small businesses is less about finding a magic formula and more about preparation, research, and strategic alignment. By cleaning up your credit, crafting a compelling business plan, and matching loan features to your cash‑flow needs, you position yourself as a low‑risk borrower.

Remember to explore alternative financing if traditional routes fall short, and always keep an eye on the total cost of borrowing. With the right loan in hand, you can invest in growth, weather early challenges, and set the stage for long‑term profitability.

Need a deeper dive into the application process or want to compare lenders side‑by‑side? Check out our comprehensive guide i need a loan for my business – Complete Guide to Funding Your Venture for step‑by‑step instructions and real‑world tips.

Good luck on your financing journey—may your new venture flourish and your repayment schedule stay comfortably on track.