Table of Contents

- How Business Loans Through Credit Card Processing Actually Work

- Key Benefits of Using Credit Card Processing for Business Loans

- Potential Drawbacks and Costs to Watch Out For

- Choosing the Right Provider for Business Loans Through Credit Card Processing

- 1. Transparency of Fees and Terms

- 2. Reputation and Customer Support

- 3. Compatibility with Your Existing POS System

- When Is a Credit‑Card‑Based Loan the Right Choice?

- Step‑by‑Step Guide to Securing a Business Loan Through Credit Card Processing

- Common Myths About Business Loans Through Credit Card Processing Debunked

- Future Trends: What’s Next for Credit‑Card‑Based Business Financing?

When you run a retail store, a coffee shop, or any business that relies on point‑of‑sale (POS) transactions, you already have a steady stream of credit‑card payments flowing through your merchant account. What many entrepreneurs don’t realize is that this same data can become a shortcut to capital. Instead of applying for a traditional bank loan, you can tap into business loans through credit card processing—a financing model that leverages your daily card sales to deliver quick cash.

This approach isn’t a brand‑new invention; it’s an evolution of the merchant cash advance (MCA) that has been around for years. What sets it apart today is the integration of modern analytics, transparent fee structures, and a focus on helping businesses that may not qualify for conventional loans. Whether you need to buy inventory, upgrade equipment, or cover a seasonal cash‑flow gap, understanding how these loans work can open a door to funding that’s both fast and flexible.

In the next sections we’ll break down the mechanics, compare the costs with other financing options, and give you practical tips on choosing the right partner. By the end, you’ll have a clear roadmap to decide if business loans through credit card processing are the right fit for your growth plans.

How Business Loans Through Credit Card Processing Actually Work

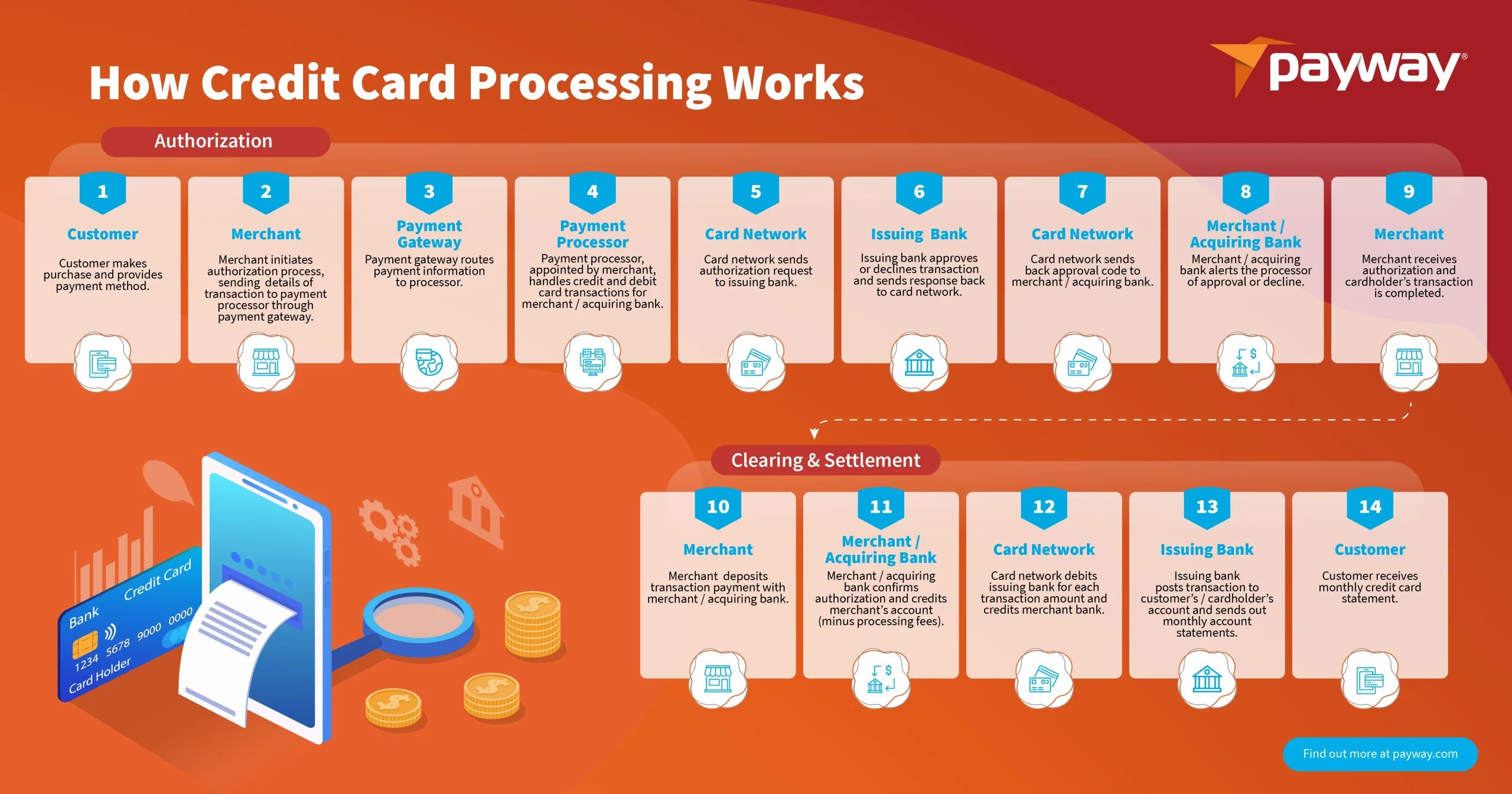

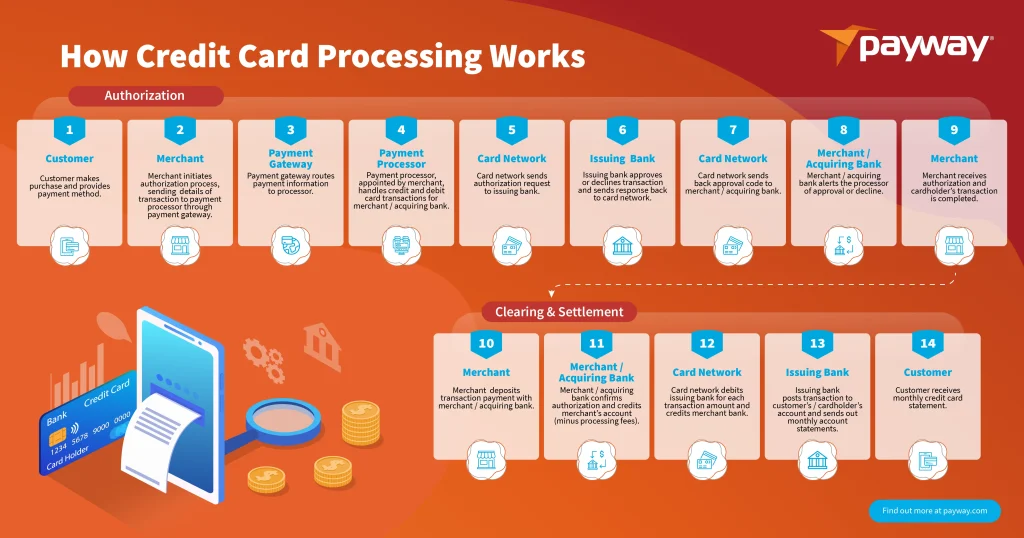

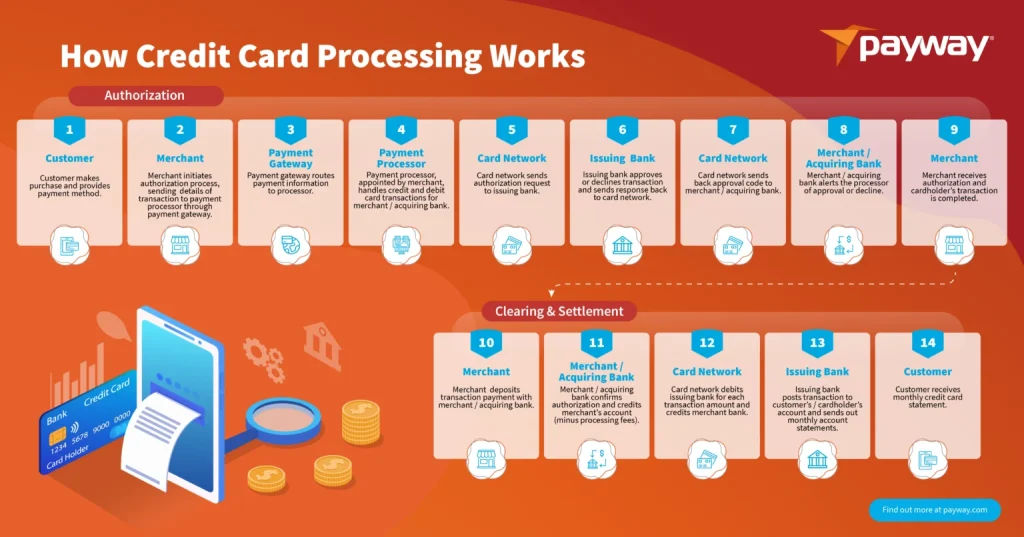

The core idea is simple: a lender looks at the volume of credit‑card transactions you process each month and offers you a lump‑sum advance that you repay by withholding a fixed percentage of those daily sales. Unlike a traditional loan with a set monthly payment, repayment fluctuates with your cash flow—if you have a busy weekend, you pay a bit more; if sales dip, the repayment slows down.

Here’s a step‑by‑step snapshot of the typical process:

- Application & verification: You provide recent credit‑card statements (usually 30‑90 days) and basic business information.

- Approval & funding: Once the lender assesses your average daily debit/credit volume, they approve a loan amount—often 10‑30% of your monthly processing volume.

- Repayment setup: A predetermined holdback rate (commonly 5‑15% of each transaction) is programmed into your merchant account.

- Daily deductions: As customers swipe or tap, the holdback amount is automatically deducted and sent to the lender until the balance is cleared.

The elegance of this model lies in its speed. Because the lender’s risk is tied directly to your ongoing sales, they can often fund the loan within 24‑48 hours—far quicker than the weeks or months it can take to navigate bank underwriting.

Key Benefits of Using Credit Card Processing for Business Loans

While the concept might seem niche, the advantages are surprisingly broad:

- Speedy access to cash: Funding can be received in as little as one business day, which is crucial for time‑sensitive opportunities.

- Flexibility in repayment: Payments adjust with your revenue, reducing the risk of missed payments during slow periods.

- Lower credit score reliance: Since the lender bases the decision on transaction history rather than personal credit, businesses with limited credit history can still qualify.

- No collateral required: You don’t have to pledge assets like equipment or real estate.

- Simple documentation: Often only a few weeks of processing statements and basic business paperwork are needed.

These perks make business loans through credit card processing especially attractive for seasonal businesses, startups, or companies looking to bridge a short‑term cash‑flow gap without taking on long‑term debt.

Potential Drawbacks and Costs to Watch Out For

Every financing solution comes with trade‑offs, and this model is no exception. The most common concerns include:

- Higher effective APR: Because the repayment is structured as a percentage of sales, the annual percentage rate can be significantly higher than traditional bank loans.

- Daily holdbacks affect cash flow: Even though the percentage is small, the constant deduction can feel like a “tax” on your sales.

- Potential for hidden fees: Some lenders add origination fees, early‑payoff penalties, or administrative charges that inflate the total cost.

- Impact on merchant account: Certain providers may place a lien on your processing account, which could affect future financing options.

Before you sign on the dotted line, run the numbers. Use a simple calculator: (Loan amount ÷ Holdback rate) = Approximate days to repayment. Compare that timeline and total cost with a conventional loan’s amortization schedule to see which is truly cheaper for your situation.

Choosing the Right Provider for Business Loans Through Credit Card Processing

Not all lenders are created equal. Here are three practical criteria to evaluate potential partners:

1. Transparency of Fees and Terms

Look for providers that clearly disclose the total factor rate, holdback percentage, and any ancillary fees. A reputable lender will present a “total cost of financing” figure upfront, allowing you to compare apples‑to‑apples with other options.

2. Reputation and Customer Support

Read reviews, ask for references, and verify that the lender is registered with the Better Business Bureau. Good customer service matters when you need to adjust holdback rates or resolve payment disputes.

3. Compatibility with Your Existing POS System

Some lenders require you to switch to their proprietary processing platform, which could mean new hardware or software fees. Others integrate seamlessly with popular systems like Square, Clover, or Toast. Ensure the integration won’t disrupt your daily operations.

If you’re still exploring financing alternatives, the guide Business Loans for New Small Businesses – A Complete Guide provides a broader overview of options, helping you decide whether a credit‑card‑based loan fits into your overall strategy.

When Is a Credit‑Card‑Based Loan the Right Choice?

Consider these scenarios:

- Seasonal spikes: If you earn a large portion of revenue during holidays or peak months, the flexible repayment aligns well with fluctuating cash flow.

- Urgent inventory purchase: Need to restock before a major sales event? The quick funding can keep shelves stocked without waiting for a bank approval.

- Limited credit history: New businesses that haven’t built a solid credit score can still access capital based on sales data.

- Desire to avoid collateral: If you’re hesitant to risk assets, this unsecured model offers peace of mind.

Conversely, if your business has a stable, low‑interest loan option from a traditional lender, or if you plan to borrow a large sum for a multi‑year project, a conventional term loan may be more cost‑effective.

Step‑by‑Step Guide to Securing a Business Loan Through Credit Card Processing

- Gather your processing statements: Pull the last 30‑90 days of transaction reports from your merchant account.

- Calculate average monthly volume: This figure will determine the maximum advance you can qualify for.

- Research lenders: Use the criteria above to shortlist three to five providers.

- Request quotes: Ask each lender for a detailed offer that includes factor rate, holdback percentage, and any fees.

- Compare total cost: Convert each offer into an APR equivalent to see the real cost of borrowing.

- Read the fine print: Look for early‑payoff clauses, lien conditions, and termination penalties.

- Submit application: Provide the required documents and wait for approval—often within 24 hours.

- Set up the holdback: Your lender will work with your processor to implement the daily deduction.

- Monitor repayments: Keep an eye on how the holdback impacts cash flow and adjust operations if needed.

For entrepreneurs who are just starting out, the article i need a loan for my business – Complete Guide to Funding Your Venture offers additional context on how this financing method fits into a broader capital‑raising strategy.

Common Myths About Business Loans Through Credit Card Processing Debunked

Myth 1: “It’s the same as a merchant cash advance.” While both use future sales as collateral, modern credit‑card‑based loans often provide clearer terms and lower fees than traditional MCAs, which can be opaque.

Myth 2: “You need perfect credit to qualify.” Since the lender’s primary focus is on transaction volume, many businesses with sub‑prime personal credit scores still receive approval.

Myth 3: “You lose control of your POS system.” Most providers integrate with existing processors; you’re not forced to switch platforms unless you choose a bundled solution.

Future Trends: What’s Next for Credit‑Card‑Based Business Financing?

Technology is reshaping the landscape. Real‑time data analytics, AI‑driven underwriting, and blockchain‑secured contracts are beginning to streamline the approval process even further. In the next few years, we can expect:

- Instant approvals: Leveraging machine learning to assess risk in seconds.

- Dynamic holdback rates: Adjusting percentages automatically based on predictive sales trends.

- Hybrid products: Combining traditional term loan features with credit‑card repayment flexibility.

Staying informed about these developments will help you make smarter financing decisions as the market evolves.

Ultimately, business loans through credit card processing represent a powerful tool in the modern entrepreneur’s toolbox. By weighing the speed and flexibility against the higher cost of capital, you can determine whether this financing route aligns with your growth timeline and cash‑flow reality. As with any financial decision, do your homework, compare offers, and choose a partner that values transparency as much as you do.