Table of Contents

- How to Refinance a Private Student Loan: The Full Process Explained

- Step 1: Assess Your Current Loan Portfolio

- Step 2: Check Your Credit Score and Credit Report

- Step 3: Determine Your Desired Refinancing Goals

- Step 4: Shop Around for Lenders

- Step 5: Gather Required Documentation

- Step 6: Submit Your Application

- Step 7: Review the Loan Offer

- Step 8: Close the New Loan and Pay Off the Old One

- Step 9: Set Up Automatic Payments

- Step 10: Monitor Your Credit and Savings

- Key Factors to Consider When Refinancing a Private Student Loan

- Interest Rate vs. Loan Term Trade‑off

- Fixed vs. Variable Rates

- Impact on Federal Benefits

- Co‑Signer Considerations

- Fees and Hidden Costs

- Common Mistakes to Avoid When Refinancing a Private Student Loan

- Skipping the Credit Check

- Ignoring the Total Cost

- Refinancing Too Early

- Not Reading the Fine Print

- Forgetting to Update Automatic Payments

- When Refinancing Makes Sense (and When It Doesn’t)

- Best Times to Refinance

- When to Pause or Skip Refinancing

- Tools and Resources to Simplify the Process

- Loan Comparison Websites

- Credit Monitoring Services

- Student Loan Calculators

- Understanding Interest Calculations

- Final Thoughts on Mastering How to Refinance a Private Student Loan

Private student loans can feel like a never‑ending weight on your shoulders, especially when the interest rates are high and the repayment terms are rigid. Unlike federal loans, private loans don’t come with income‑driven repayment plans, forgiveness options, or easy deferments, so many borrowers start looking for ways to cut costs. The most common answer? how to refinance a private student loan. By swapping your existing loan for a new one with a lower rate or better terms, you can potentially shave years off your repayment schedule and keep more cash in your pocket each month.

But the refinancing landscape isn’t a free‑for‑all. Lenders will scrutinize your credit, income, and overall financial health before they hand over a better deal. That means the process can be a little intimidating if you’ve never walked through it before. In this article we’ll walk you through every stage— from checking your eligibility to sealing the deal—so you’ll know exactly how to refinance a private student loan without any surprise roadblocks.

Before we dive into the nitty‑gritty, let’s clear up a couple of myths that often trip up borrowers. First, refinancing doesn’t erase your original loan; it simply replaces it with a new contract. Second, you won’t lose any borrower protections you already have, but you also won’t gain the federal benefits that come with federal loans. Understanding these basics will help you decide if refinancing is truly the right move for your financial situation.

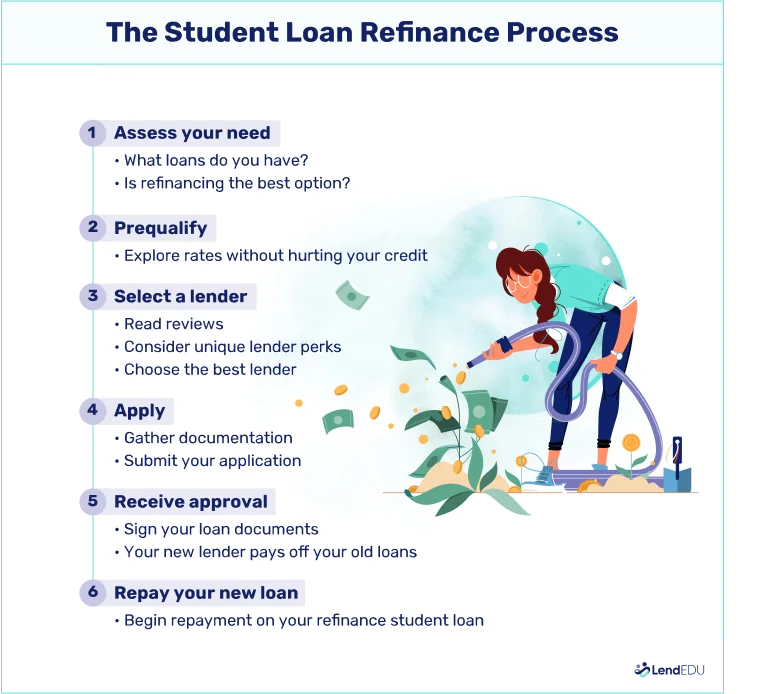

How to Refinance a Private Student Loan: The Full Process Explained

Now that you’ve got the big picture, let’s break down the step‑by‑step approach to refinancing. Each phase builds on the previous one, and skipping a step can cost you time—or money.

Step 1: Assess Your Current Loan Portfolio

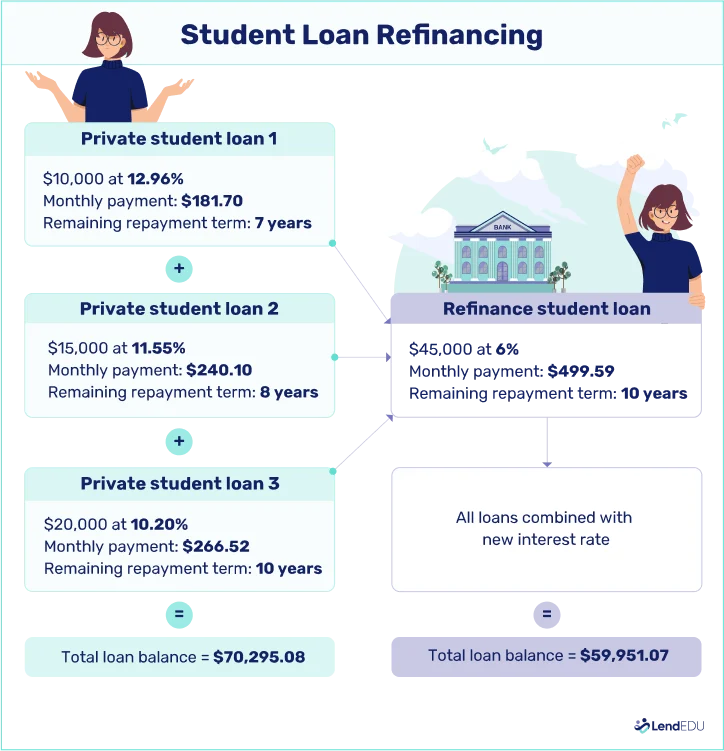

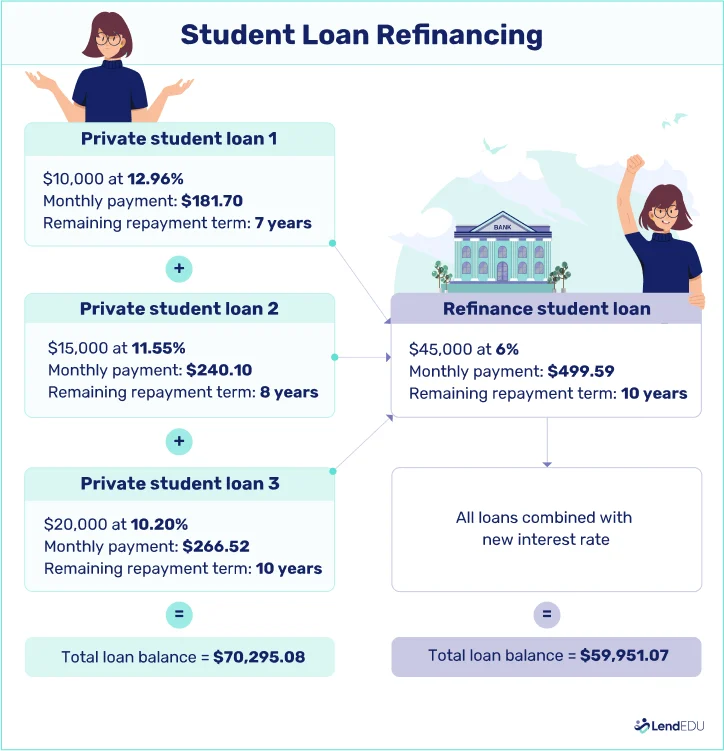

Start by gathering every detail about your existing private loans: balance, interest rate, remaining term, and any fees for early repayment. Knowing these numbers lets you calculate your current monthly payment and compare it against potential offers later on. Tools like loan calculators can help you see how much you’d save with a lower rate.

Step 2: Check Your Credit Score and Credit Report

Your credit score is the single biggest factor lenders consider when you’re learning how to refinance a private student loan. A score of 700 or higher generally opens the door to the most competitive rates. Pull your credit reports from the three major bureaus (Equifax, Experian, TransUnion) and dispute any errors before you apply.

Step 3: Determine Your Desired Refinancing Goals

- Lower interest rate: The most common goal, which reduces overall interest paid.

- Shorter loan term: Helps you pay off debt faster, though monthly payments may rise.

- Reduced monthly payment: Extending the term can free up cash flow.

- Switching from variable to fixed rate: Locks in a predictable payment schedule.

Knowing which goal matters most to you will guide the type of lender you target and the offers you’ll compare.

Step 4: Shop Around for Lenders

Don’t settle for the first quote you receive. Major banks, credit unions, and online lenders all have different underwriting criteria. Use comparison sites to pull multiple pre‑qualification offers—most of them won’t affect your credit score because they use a soft inquiry. When you see an offer that aligns with your goals, dig deeper into the APR, fees, and any special conditions.

Step 5: Gather Required Documentation

Typical documents include:

- Proof of income (pay stubs, W‑2s, tax returns)

- Identification (driver’s license, passport)

- Current loan statements

- Bank statements (to verify assets)

Having everything ready speeds up the underwriting process and shows lenders you’re organized.

Step 6: Submit Your Application

Most lenders now allow you to complete the application online. Fill out personal information, upload the documents you prepared, and answer any additional questions about your financial habits. If the lender uses a hard credit pull, be prepared for a slight dip in your score—typically less than five points.

Step 7: Review the Loan Offer

When the lender approves you, they’ll present a loan agreement. Pay special attention to:

- Interest rate (APR): Make sure it’s lower than your current rate.

- Loan term: Verify it aligns with your goal (shorter vs. longer).

- Fees: Origination fees, prepayment penalties, or closing costs can offset savings.

- Repayment schedule: Check the exact monthly payment amount.

If anything looks off, negotiate or request a revised offer before you sign.

Step 8: Close the New Loan and Pay Off the Old One

Once you accept the terms, the new lender will typically send the funds directly to your existing loan servicer to pay off the balance. This “one‑step” payoff eliminates the need for you to handle large transfers yourself, reducing the risk of missed payments.

Step 9: Set Up Automatic Payments

Most lenders reward borrowers with a small interest rate discount when you enroll in automatic monthly debits. It’s a win‑win: you never miss a payment, and you lock in a slightly better rate.

Step 10: Monitor Your Credit and Savings

After refinancing, keep an eye on your credit report to ensure the old loan is marked as “paid in full.” Then, track how much you’re saving each month and annually. Use the extra cash to build an emergency fund, invest, or accelerate the repayment of other debts.

Key Factors to Consider When Refinancing a Private Student Loan

Understanding how to refinance a private student loan isn’t just about following steps; it’s also about weighing the pros and cons specific to your situation.

Interest Rate vs. Loan Term Trade‑off

A lower rate with a longer term can lower your monthly payment but may increase the total interest paid over the life of the loan. Conversely, a shorter term with a modestly lower rate can speed up debt freedom while still saving you money overall. Use a calculator to model both scenarios.

Fixed vs. Variable Rates

Variable rates often start lower than fixed rates but can rise if the market changes. If you plan to keep the loan for many years, a fixed rate offers predictability. If you expect to pay off the loan quickly, a variable rate might give you a better short‑term deal.

Impact on Federal Benefits

Because you’re dealing with private loans, you won’t lose any federal benefits—because there are none attached. However, if you have a mix of federal and private loans, consider keeping the federal portion separate to retain options like income‑driven repayment or forgiveness.

Co‑Signer Considerations

Some borrowers use a co‑signer to qualify for a better rate. While this can open doors, it also places financial responsibility on the co‑signer. Make sure both parties understand the commitment and are comfortable with the credit implications.

Fees and Hidden Costs

Some lenders charge origination fees (usually 1%‑5% of the loan amount) or waive them in exchange for a slightly higher rate. Always calculate the net savings after factoring in these costs.

Common Mistakes to Avoid When Refinancing a Private Student Loan

Even seasoned borrowers can slip up. Here are the pitfalls that can erode the benefits of refinancing.

Skipping the Credit Check

Assuming you’ll get a great rate without checking your credit score can lead to disappointment. A surprise low score may push you into a higher‑interest offer, negating any potential savings.

Ignoring the Total Cost

Focusing only on the monthly payment can be misleading. Always compare the total amount you’ll pay over the life of the loan, including any fees.

Refinancing Too Early

If you’re still early in your career, waiting a year or two can boost your credit and income, opening the door to even better rates.

Not Reading the Fine Print

Some lenders hide prepayment penalties or require you to stay with them for a minimum period. Those clauses can trap you in an unfavorable deal.

Forgetting to Update Automatic Payments

After the old loan is paid off, make sure you set up a new automatic payment schedule with the new lender. Missing this step can cause a late payment and damage your credit.

When Refinancing Makes Sense (and When It Doesn’t)

Every financial decision hinges on personal context. Below are scenarios where how to refinance a private student loan is typically a smart move, and others where you might hold off.

Best Times to Refinance

- Credit score above 720: You’ll qualify for the most competitive rates.

- Stable, high income: Lenders view you as low risk.

- High existing interest rate (6%+): A lower rate can save thousands.

- Desire for a fixed rate: Lock in predictability for the long term.

When to Pause or Skip Refinancing

- Low interest rate (under 4%): Savings may be minimal.

- Close to loan payoff: Fees could outweigh benefits.

- Potential future federal benefits: If you might qualify for forgiveness, keep the loan federal.

- Unstable income: Variable payments could become a burden.

Tools and Resources to Simplify the Process

Technology makes it easier than ever to navigate how to refinance a private student loan. Here are a few resources you might find handy:

Loan Comparison Websites

Platforms like Refinance Student Loans Without a Degree – Your Complete Guide aggregate offers from multiple lenders, allowing you to see side‑by‑side APRs, terms, and fees with just a few clicks.

Credit Monitoring Services

Free tools from credit bureaus let you track score changes in real time, helping you time your application for the best possible rate.

Student Loan Calculators

Use online calculators to model different scenarios—fixed vs. variable rates, shorter terms, or adding a co‑signer—to see how each choice impacts your monthly payment and total interest.

Understanding Interest Calculations

If you’re unsure whether your loan interest accrues monthly or yearly, check out Is Student Loan Interest Monthly or Yearly? A Complete Guide. Knowing the compounding method helps you estimate true costs more accurately.

Final Thoughts on Mastering How to Refinance a Private Student Loan

Refinancing a private student loan can be a powerful lever to improve your financial health, but it’s not a one‑size‑fits‑all solution. By following the steps outlined above—assessing your current loan, checking your credit, setting clear goals, shopping around, and carefully reviewing offers—you’ll position yourself to make an informed decision that truly aligns with your long‑term objectives.

Remember, the ultimate goal isn’t just a lower monthly payment; it’s to reduce the total cost of borrowing and free up resources for the things that matter most—whether that’s building an emergency fund, investing for retirement, or simply gaining peace of mind.

Take the time to evaluate your personal circumstances, leverage the right tools, and don’t rush the process. With a disciplined approach, you’ll discover exactly how to refinance a private student loan in a way that maximizes savings and supports your broader financial roadmap.

Ready to start? Grab your loan statements, pull your credit report, and begin comparing offers today. The sooner you act, the faster you’ll be on the path to a lighter, more manageable debt load.

[FINANCE]: Finance