Table of Contents

- how do i refinance my student loans: The Full Process Explained

- how do i refinance my student loans – Assess Your Current Situation

- how do i refinance my student loans – Research Lenders and Loan Products

- how do i refinance my student loans – Gather Required Documentation

- how do i refinance my student loans – Submit Applications and Compare Offers

- how do i refinance my student loans – Accept the Offer and Close the Deal

- how do i refinance my student loans – Monitor and Adjust Over Time

- Common Questions About Refinancing Student Loans

- Can I refinance federal loans without losing benefits?

- What credit score do I need?

- How much can I actually save?

- Is there a cost to refinance?

- Do I need a cosigner?

- Tips to Maximize Your Refinancing Success

Student loan debt can feel like a heavy backpack you’re forced to carry for years, especially when interest rates start to nibble away at your principal. The good news? You don’t have to stay stuck with the original terms you signed up for. By asking yourself “how do i refinance my student loans,” you open the door to potentially lower interest rates, reduced monthly payments, and a clearer path to financial freedom.

Before diving into the mechanics, it’s worth remembering that refinancing isn’t a one‑size‑fits‑all solution. It works best for borrowers with stable income, solid credit, and a clear plan for repayment. If you’re juggling multiple loans, variable rates, or a mix of federal and private debt, the process can feel a bit overwhelming. This guide breaks everything down into bite‑size steps, so you’ll know exactly what to do, when to do it, and why each move matters.

Let’s get started by demystifying the core concept: refinancing simply means taking out a new loan—usually with a private lender—to pay off one or more of your existing student loans. The new loan replaces the old ones, ideally at a lower rate or more favorable terms. Below you’ll find a step‑by‑step roadmap that answers the most common questions about how do i refinance my student loans and equips you with the tools to make an informed decision.

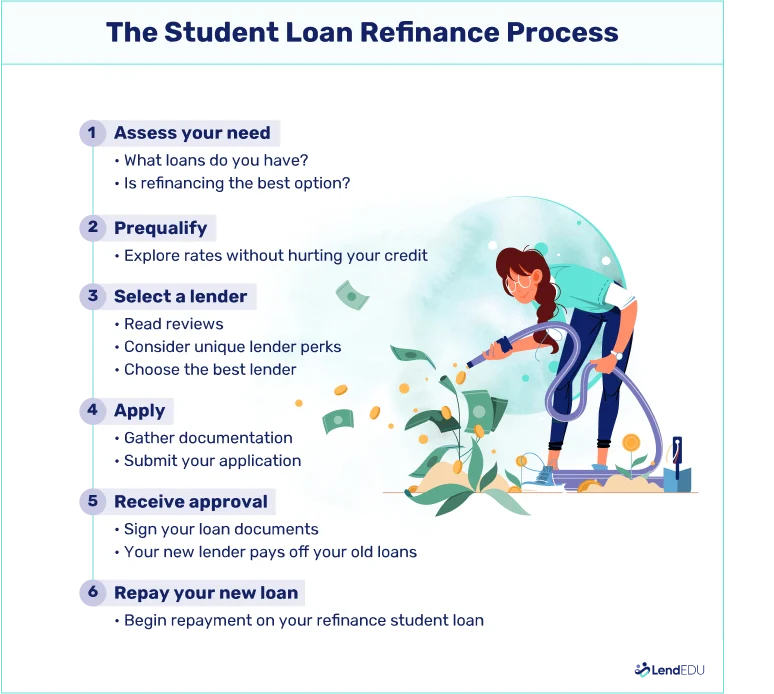

how do i refinance my student loans: The Full Process Explained

Refinancing your student debt can be boiled down to six main stages. Each stage has its own checklist, pitfalls to avoid, and best‑practice tips. By following this roadmap, you’ll minimize surprises and maximize the chances of landing a deal that truly benefits you.

how do i refinance my student loans – Assess Your Current Situation

Before you even open a lender’s website, take a hard look at where you stand financially:

- Interest rates: Note the APR on each loan. Federal loans often sit around 4‑7%, while private loans can range from 3% to 12% or higher.

- Monthly payment: Add up what you’re paying each month across all loans.

- Remaining balance: Knowing the total principal helps you gauge how much you can save.

- Credit score: Most private lenders require a credit score of 660+ for the best rates; a score above 720 can unlock the lowest offers.

- Employment stability: Lenders love a steady income stream. Gather recent pay stubs or tax returns.

Having these numbers in front of you will make the comparison phase much smoother. It also helps you answer the core question “how do i refinance my student loans?” by showing whether a better rate is realistic for your profile.

how do i refinance my student loans – Research Lenders and Loan Products

Not all lenders are created equal. Some specialize in low‑interest rates for high‑credit borrowers, while others offer flexible repayment options for those with a modest credit history. Here’s how to sift through the options:

- Interest type: Fixed vs. variable. Fixed rates lock in a single percentage for the life of the loan; variable rates can start lower but may rise over time.

- Loan terms: Typical repayment periods range from 5 to 20 years. Shorter terms mean higher monthly payments but less interest overall.

- Fees: Look for origination fees, prepayment penalties, or application fees that could erode your savings.

- Customer service: Read reviews and consider whether the lender offers a dedicated support line for borrowers.

For a deeper dive into private‑loan refinancing, check out our practical guide to refinancing private student loans. That article walks you through lender selection, rate negotiation, and what to watch out for.

how do i refinance my student loans – Gather Required Documentation

Most lenders will ask for a similar set of documents. Having them ready speeds up the approval process:

- Government‑issued ID (driver’s license or passport)

- Social Security number

- Proof of income (pay stubs, W‑2s, or tax returns)

- List of existing student loans (statements showing balances and interest rates)

- Bank account information for disbursement and repayment

Organize everything in a dedicated folder—digital or physical—so you can upload or fax documents at a moment’s notice.

how do i refinance my student loans – Submit Applications and Compare Offers

With documentation in hand, you can now apply to several lenders. Most major banks, credit unions, and online lenders provide a quick pre‑qualification tool that gives you a tentative rate without a hard credit pull. Use this to:

- Identify the most competitive APR.

- Check total monthly payment after refinancing.

- Calculate total interest paid over the life of the new loan.

When you receive formal offers, line them up side‑by‑side. A handy spreadsheet can help you compare APR, term length, monthly payment, and any fees. Remember: the “lowest rate” isn’t always the “best deal” if it comes with high origination fees or a short repayment window you can’t afford.

how do i refinance my student loans – Accept the Offer and Close the Deal

Once you’ve selected the lender that best matches your goals, the closing process is fairly straightforward:

- Sign the loan agreement electronically or on paper.

- Provide any final documentation the lender requests.

- The lender pays off your existing loans directly—often within 2‑4 weeks.

- You begin making payments to the new lender according to the agreed schedule.

Keep an eye on the transition period. Some borrowers notice a brief overlap where both the old and new lenders are processing payments. To avoid missed payments, consider setting up automatic withdrawals a few days before the first new‑loan payment is due.

how do i refinance my student loans – Monitor and Adjust Over Time

Refinancing is not a “set it and forget it” maneuver. After you’ve secured the new loan, stay proactive:

- Watch interest rates: If rates drop significantly, you may be able to refinance again for even better terms.

- Reassess your budget: If your income rises, you could shorten the term to pay off debt faster.

- Maintain good credit: Paying on time and keeping credit utilization low will keep your score healthy for future financing needs.

In short, the answer to “how do i refinance my student loans” is a continuous cycle of evaluation and adjustment, not a single transaction.

Common Questions About Refinancing Student Loans

Can I refinance federal loans without losing benefits?

Yes, you can refinance federal loans, but doing so replaces them with a private loan, meaning you lose access to federal protections such as income‑driven repayment plans, deferment, forbearance, and loan forgiveness programs. If those benefits are valuable to you, weigh them carefully before moving forward. Many borrowers keep a portion of their federal debt untouched while refinancing the private portion.

What credit score do I need?

While requirements vary, a score of 660+ typically qualifies for the best rates, and 720+ often unlocks the ultra‑low‑APR offers you see advertised. If your score is lower, consider a co‑signer, a credit‑union loan, or spending a few months improving your credit before applying.

How much can I actually save?

Saving potential depends on the spread between your current APR and the new rate, as well as the term you choose. For example, refinancing a $40,000 balance from 7% to 4% over 10 years can shave off roughly $5,000 in interest and cut the monthly payment by $150. Use an online calculator to model different scenarios.

Is there a cost to refinance?

Many lenders offer “no‑fee” refinancing, but some charge an origination fee (usually 1%‑2% of the loan amount). Always factor this into your total cost calculation. A small fee can be worthwhile if the rate drop is substantial.

Do I need a cosigner?

If your credit profile isn’t strong enough to secure a low rate on your own, a cosigner with good credit can improve your offer. However, the cosigner becomes legally responsible for the loan, so discuss expectations and repayment plans upfront.

Tips to Maximize Your Refinancing Success

- Shop around: Apply to at least three lenders to compare rates and terms.

- Lock in a rate quickly: Once you find a favorable offer, lock it in before market rates shift.

- Consider a shorter term: Even a modest reduction in loan length can dramatically lower total interest.

- Automate payments: Many lenders shave 0.25%‑0.5% off your APR for auto‑pay enrollment.

- Keep an eye on fees: A low rate paired with a high origination fee can negate savings.

If you’re curious about how loan consolidation works for federal debt, our complete guide on student loan interest breaks down the math in plain English.

Refinancing is a powerful tool, but it’s only as good as the research and planning you put into it. By following the steps outlined above, you’ll confidently answer the question “how do i refinance my student loans” and move toward a lighter financial load.

So, take a breath, pull together your documents, and start comparing offers today. The sooner you act, the sooner you could be paying less each month, saving thousands in interest, and edging closer to a debt‑free future.