Table of Contents

- Understanding the High Loan to Value Home Equity Loan

- Why Borrowers Choose a High Loan to Value Home Equity Loan

- Key Benefits of a High Loan to Value Home Equity Loan

- Flexibility and Speed

- Potentially Lower Interest Than Credit Cards

- Tax‑Deductible Interest (When Applicable)

- Risks and Drawbacks to Keep in Mind

- Higher Interest Rates and Fees

- Reduced Home Equity Cushion

- Stricter Qualification Standards

- Potential Impact on Future Financing

- How to Qualify for a High Loan to Value Home Equity Loan

- Credit Score and History

- Debt‑to‑Income Ratio (DTI)

- Stable Income and Employment

- Appraisal and Property Condition

- Smart Strategies for Managing a High Loan to Value Home Equity Loan

- Pay More Than the Minimum

- Consider a Fixed‑Rate Option

- Build an Emergency Fund

- Keep an Eye on Property Value

- Alternatives to a High Loan to Value Home Equity Loan

- Home Equity Line of Credit (HELOC)

- Cash‑Out Refinance

- Personal Loans

- Other Asset‑Based Loans

- Real‑World Example: When a High Loan to Value Home Equity Loan Made Sense

- Frequently Asked Questions About High Loan to Value Home Equity Loans

- Can I refinance a high loan to value home equity loan later?

- Is the interest tax‑deductible?

- What happens if I can’t make payments?

- Do lenders require mortgage insurance?

- How does a high loan to value home equity loan affect my credit score?

When you hear the term “high loan to value home equity loan,” it can feel like financial jargon that only lenders understand. In reality, it’s simply a type of home equity borrowing where the lender lets you tap a larger slice of your property’s equity than what’s typical. For many homeowners, this can open doors to renovation funds, debt consolidation, or even a fresh start after a financial setback.

But as with any credit product, the higher the loan‑to‑value (LTV) ratio, the higher the risk—for both you and the lender. That risk shows up as higher interest rates, stricter qualification standards, and sometimes extra fees. Understanding how a high loan to value home equity loan works, when it makes sense, and how to protect yourself is crucial before you sign on the dotted line.

In this article, we’ll break down the concept, walk through the pros and cons, and share practical tips to help you decide if this financing option aligns with your goals. Whether you’re a first‑time homeowner or a seasoned real‑estate investor, you’ll walk away with a clearer picture of what a high loan to value home equity loan can do for you.

Understanding the High Loan to Value Home Equity Loan

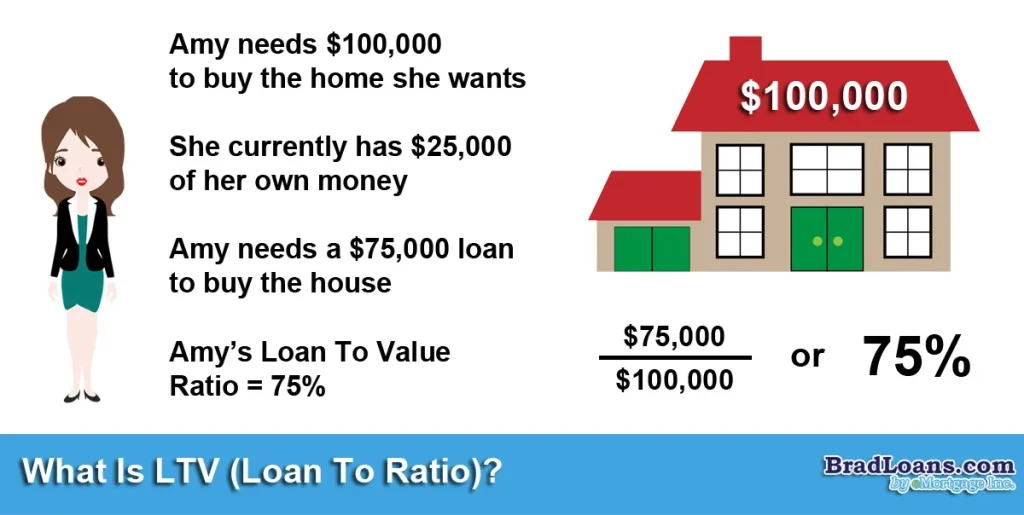

A “high loan to value home equity loan” means the amount you borrow is a high percentage of your home’s current market value. Traditional home equity loans often cap the LTV at 80 %—meaning you can borrow up to 80 % of the home’s appraised value, minus any existing mortgage balance. A high LTV loan pushes that boundary, sometimes allowing borrowers to reach 90 % or even 95 % LTV.

Here’s a quick snapshot of how the math works:

- Current market value of home: $400,000

- Outstanding mortgage balance: $200,000

- Maximum LTV allowed (e.g., 90 %): $360,000

- Potential equity you could tap: $360,000 – $200,000 = $160,000

In this scenario, a high loan to value home equity loan would let you borrow $160,000, whereas a conventional 80 % LTV loan would only allow $120,000. That extra $40,000 can be a game‑changer for large projects, but it also means the lender is taking on more risk, which often translates to higher costs for you.

Why Borrowers Choose a High Loan to Value Home Equity Loan

- Access to larger funds: Ideal for major renovations, buying an investment property, or covering unexpected expenses.

- Fewer assets needed: If you don’t have significant cash reserves, leveraging more of your home’s equity can be attractive.

- Potential tax benefits: In some jurisdictions, interest on home equity loans remains tax‑deductible if used for home improvements.

Key Benefits of a High Loan to Value Home Equity Loan

While the higher LTV ratio brings extra cost, there are tangible benefits that can outweigh those concerns for the right borrower.

Flexibility and Speed

Because the loan is secured by your property, lenders can often approve and fund the loan faster than unsecured personal loans. This speed is useful when you need cash quickly for a remodel or an investment opportunity.

Potentially Lower Interest Than Credit Cards

Even with a premium rate, a high loan to value home equity loan usually beats credit‑card APRs, which can soar above 20 %.

Tax‑Deductible Interest (When Applicable)

If you use the borrowed funds for qualified home improvements, the interest may be deductible on your federal tax return, effectively lowering the after‑tax cost of borrowing.

Risks and Drawbacks to Keep in Mind

Every financial decision has a flip side. With a high loan to value home equity loan, the most pressing concerns revolve around cost, qualification hurdles, and the impact on your overall financial health.

Higher Interest Rates and Fees

Lenders price the extra risk with steeper interest rates and sometimes add origination fees, appraisal costs, or mortgage insurance premiums.

Reduced Home Equity Cushion

By borrowing more against your home, you shrink the equity buffer that could protect you in a market downturn. If property values drop, you could end up “under‑water,” owing more than the home is worth.

Stricter Qualification Standards

Credit score requirements, debt‑to‑income (DTI) ratios, and proof of stable income become more stringent as the LTV climbs. Some lenders may also require private mortgage insurance (PMI) when the LTV exceeds a certain threshold.

Potential Impact on Future Financing

A high LTV loan can limit your ability to refinance or obtain additional credit later. Lenders may view the increased debt load as a red flag.

How to Qualify for a High Loan to Value Home Equity Loan

Getting approved isn’t impossible, but you’ll need to prepare a strong financial profile. Below are the main pillars lenders examine:

Credit Score and History

Most lenders look for a minimum score of 680–720 for high LTV products. A spotless payment history, low credit utilization, and limited recent inquiries boost your chances.

Debt‑to‑Income Ratio (DTI)

DTI is the percentage of your gross monthly income that goes toward debt payments. For high LTV loans, aim for a DTI below 40 %—the lower, the better.

Stable Income and Employment

Lenders love consistency. Two years of steady employment, preferably in the same field, reassures them you can handle the larger monthly payment.

Appraisal and Property Condition

An up‑to‑date appraisal is mandatory. If the appraisal comes in lower than expected, it could reduce the maximum loan amount or push you out of the high LTV bracket.

Smart Strategies for Managing a High Loan to Value Home Equity Loan

Even after you secure the loan, responsible management is key to avoiding pitfalls.

Pay More Than the Minimum

High LTV loans often carry higher rates, so any extra principal you pay reduces interest over the life of the loan. Set up automatic extra payments if possible.

Consider a Fixed‑Rate Option

If you’re concerned about rising rates, a fixed‑rate high loan to value home equity loan locks in a predictable payment schedule.

Build an Emergency Fund

Having three to six months of expenses saved can protect you from default if your income takes a hit.

Keep an Eye on Property Value

Regularly monitor your home’s market value. If you notice a downward trend, you might want to accelerate repayments to avoid negative equity.

Alternatives to a High Loan to Value Home Equity Loan

Before committing, compare other financing routes that could be cheaper or less risky.

Home Equity Line of Credit (HELOC)

A HELOC works like a credit card, allowing you to draw funds as needed. It typically offers lower initial rates, but the variable rate can climb over time.

Cash‑Out Refinance

Refinancing your entire mortgage and pulling out cash can sometimes provide a lower rate than a high LTV home equity loan, especially if you have strong credit.

Personal Loans

Unsecured personal loans have higher rates than traditional home equity products, but they don’t put your home at risk.

Other Asset‑Based Loans

If you own other valuable assets—like a 401(k) or investment portfolio—you might explore borrowing against them. For instance, you could read Should You Use 401(k) to Pay Off Student Loan? A Practical Guide to understand how leveraging retirement accounts works, though it’s a different context.

Real‑World Example: When a High Loan to Value Home Equity Loan Made Sense

Imagine a homeowner, Sarah, who owns a $500,000 property with a $150,000 mortgage balance. She wants to add a second story and an accessory dwelling unit (ADU) to increase rental income. The renovation cost is estimated at $180,000.

Sarah’s options:

- Standard 80 % LTV loan: Max borrowing = $400,000 (80 % of $500k) – $150k = $250k. She could fund the project, but the lender requires a lower loan amount due to her credit score, leaving her short.

- High loan to value home equity loan at 90 % LTV: Max borrowing = $450,000 – $150k = $300k. She can cover the $180k renovation comfortably and still have cash left for contingencies, albeit at a higher interest rate.

Sarah’s credit score is 720, DTI is 32 %, and she has a solid employment history. She qualifies, locks in a fixed‑rate loan, and uses the extra cash cushion to finish the project ahead of schedule. The rental income from the ADU later offsets the higher monthly payment, making the high LTV loan a strategic move.

Frequently Asked Questions About High Loan to Value Home Equity Loans

Can I refinance a high loan to value home equity loan later?

Yes, many borrowers refinance once their LTV drops below a more favorable threshold (e.g., 80 %). This can reduce interest rates and eliminate mortgage insurance. Keep an eye on market rates and your equity position.

Is the interest tax‑deductible?

Only if the loan proceeds are used for qualified home improvements. For other uses, the interest generally isn’t deductible. Consult a tax professional for personalized advice.

What happens if I can’t make payments?

Missing payments can lead to foreclosure, as the loan is secured by your home. That’s why building an emergency fund and choosing a loan you can comfortably service are essential.

Do lenders require mortgage insurance?

When LTV exceeds a certain level (often 80 % or 85 %), lenders may require private mortgage insurance (PMI) to protect themselves, adding to your monthly cost.

How does a high loan to value home equity loan affect my credit score?

Applying for the loan triggers a hard inquiry, which may dip your score slightly. More importantly, the new debt increases your overall credit utilization, which can lower your score until you demonstrate on‑time payments.

If you’re curious about how other types of borrowing compare, you might explore What Does Refinancing a Student Loan Mean? A Full Guide to see how loan terms and rates differ across product categories.

In the end, a high loan to value home equity loan can be a powerful tool when used wisely. It offers larger cash access, potentially lower rates than unsecured debt, and tax advantages if you meet the criteria. However, the higher cost, stricter qualification, and reduced equity cushion mean you must weigh the pros against the cons carefully.

Do a thorough self‑assessment, shop around for the best rates, and consider alternative financing before committing. With a clear plan and disciplined repayment strategy, you can harness the extra equity in your home without jeopardizing your financial future.