Table of Contents

- Understanding the Small Business Loan Line of Credit

- How a Small Business Loan Line of Credit Works

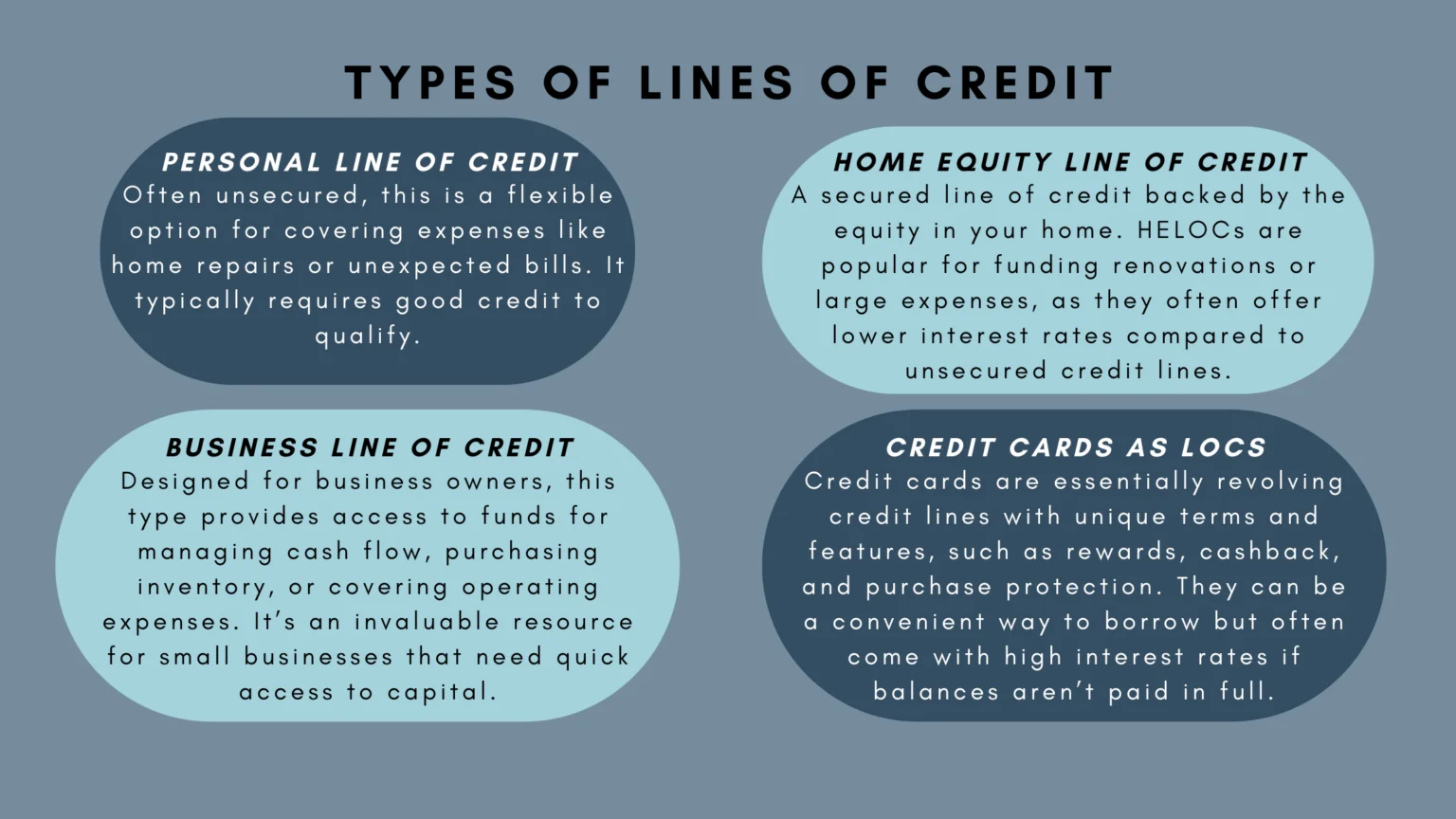

- Benefits of a Small Business Loan Line of Credit

- Eligibility and Qualification Criteria

- Choosing the Right Lender

- Tips to Maximize Your Small Business Loan Line of Credit

- Common Pitfalls and How to Avoid Them

Running a small business means juggling cash flow, inventory, payroll, and unexpected opportunities—all at the same time. When a sudden invoice arrives or a promising marketing campaign needs funding, having cash on hand can be the difference between seizing the moment and watching it slip away. That’s where a small business loan line of credit steps in, offering a flexible pool of money that you can draw from, repay, and draw again, much like a credit card but tailored for business needs.

Unlike a traditional term loan, which hands you a lump sum that you must repay on a fixed schedule, a line of credit acts more like a financial safety net. You only pay interest on the amount you actually use, and once you pay it back, the credit becomes available again. This revolving nature makes it especially attractive for businesses with fluctuating expenses or seasonal revenue streams. In this article we’ll unpack every layer of the small business loan line of credit, from how it works to the nitty‑gritty of qualifying, and give you actionable tips to make the most of this financing tool.

Understanding the Small Business Loan Line of Credit

A small business loan line of credit is essentially an agreement between you and a lender that sets a maximum credit limit you can borrow against at any time. Think of it as a pre‑approved loan that stays open for a set period—usually 12 to 60 months—allowing you to tap into funds as needed. The key features include:

- Revolving credit: Borrow, repay, and borrow again without reapplying.

- Variable interest rates: Most lines of credit charge interest only on the amount drawn, often tied to the prime rate plus a margin.

- Flexible repayment terms: Minimum monthly payments are usually interest‑only, but you can pay down principal faster to reduce overall costs.

- Credit limit: Determined by your business’s financial health, annual revenue, and credit score.

If you’ve ever read the small business line of credit guide on our site, you’ll recognize that the core principle remains the same across lenders: a pool of money that you control. The main advantage is flexibility—use it for inventory purchases, bridge cash‑flow gaps, fund marketing campaigns, or even cover unexpected equipment repairs.

How a Small Business Loan Line of Credit Works

Once approved, the lender allocates a credit line, say $50,000. You receive a draw account—often accessible via an online portal, a linked business debit card, or checks. When you need cash, you “draw” an amount, for example $10,000, to pay a vendor. Interest accrues on that $10,000, not the full $50,000. As you repay the $10,000 plus interest, the $10,000 becomes available again, ready for the next draw. This revolving loop can continue for the life of the agreement, provided you stay within the credit limit and meet any covenants.

Many lenders also offer a “draw period” (usually the first 12–24 months) where you can borrow up to the limit, followed by a “repayment period” where you focus on paying down the balance. Some lines, however, remain fully revolving for the entire term, giving you perpetual flexibility.

Benefits of a Small Business Loan Line of Credit

- Cash‑flow management: Smooth out the peaks and valleys of revenue, ensuring you can cover payroll or supplier invoices even during slow months.

- Cost‑effective borrowing: Pay interest only on the amount you use, unlike term loans where you’re charged interest on the full amount from day one.

- Speed and convenience: Once the line is set up, drawing funds is almost instantaneous, saving you time compared to applying for a new loan each time.

- Credit building: Regular, responsible use can improve your business credit profile, making future financing easier.

- Negotiating power: Having ready cash can strengthen your position with vendors, potentially unlocking better payment terms or bulk discounts.

Eligibility and Qualification Criteria

Getting approved for a small business loan line of credit isn’t a walk in the park, but it’s far less stringent than many other financing options. Lenders typically look at:

- Business credit score: A score of 650+ is generally considered good; the higher, the better rates you’ll receive.

- Annual revenue: Most lenders require at least $100,000 in annual revenue, though some alternative lenders are more flexible.

- Time in business: A minimum of 1–2 years operating history is common, though startups may qualify with strong personal credit.

- Debt‑to‑income ratio: Lenders assess how much of your cash flow is already committed to existing debt.

- Bank statements and financial statements: Demonstrating steady cash flow and profitability helps your case.

If you’re unsure where you stand, a quick review of the small business loans based on revenue guide can give you a benchmark. Remember, the stronger your financials, the larger the credit limit you can negotiate.

Choosing the Right Lender

Not all lenders are created equal. Traditional banks, credit unions, online lenders, and fintech platforms each bring different terms, rates, and application experiences. Here are a few factors to weigh:

- Interest rate structure: Fixed vs. variable, APR, and any rate caps.

- Fees: Setup fees, annual fees, draw fees, and early‑termination fees can add up.

- Credit limit flexibility: Some lenders allow you to increase the limit after a review period.

- Customer service: Quick response times and an intuitive online portal are priceless when you need funds fast.

- Reputation: Look for reviews, Better Business Bureau ratings, and testimonials from businesses similar to yours.

For many owners, the decision comes down to a balance of cost and convenience. A bank might offer the lowest rate but require extensive paperwork, while an online lender could approve you within 24 hours at a slightly higher APR. Evaluate what matters most for your operational rhythm.

Tips to Maximize Your Small Business Loan Line of Credit

- Use it strategically, not as a cash‑dump: Draw only for genuine business needs. Treat the line as a tool for growth, not a substitute for proper budgeting.

- Pay down principal early: Reducing the balance lowers interest costs and frees up credit for future draws.

- Monitor utilization ratio: Keep your usage below 30‑40% of the limit to maintain a healthy credit profile.

- Set up automatic payments: Avoid missed payments that can trigger higher rates or limit reductions.

- Review terms annually: As your business grows, you may qualify for a higher limit or better rates; renegotiate proactively.

One often‑overlooked tactic is to align your line of credit with seasonal peaks. For example, a retailer might draw heavily before holiday inventory purchases, then repay quickly after the sales rush, keeping interest exposure minimal.

Common Pitfalls and How to Avoid Them

Even with a flexible financing tool, missteps can erode the benefits:

- Over‑borrowing: Pulling the maximum amount without a clear repayment plan can strain cash flow.

- Ignoring fees: Some lenders charge a fee for each draw; track these to avoid surprise costs.

- Neglecting credit health: Late payments or high utilization can damage your business credit score, making future financing more expensive.

- Relying on the line for long‑term debt: A line of credit is best for short‑term, revolving needs. For major equipment purchases or expansion, a term loan may be more cost‑effective.

If you ever find yourself stuck with a high‑cost financing product, such as a merchant cash advance, our How to Get Out of MCA Loans – Proven Strategies article offers a roadmap to transition to healthier credit options, including a small business loan line of credit.

In practice, the right line of credit becomes a silent partner in your daily operations—always there when you need it, but never intruding when you don’t. By staying disciplined, tracking usage, and choosing a lender that aligns with your growth trajectory, you can leverage this financing instrument to smooth cash flow, seize opportunities, and ultimately fuel sustainable expansion.

Remember, financing is a marathon, not a sprint. A well‑managed small business loan line of credit can provide the breathing room you need to focus on what truly matters: delivering value to your customers, innovating your product line, and building a brand that stands the test of time. Keep the line of credit as a strategic asset, revisit its terms periodically, and let it work for you—rather than the other way around.