Table of Contents

- does student loan consolidation affect credit score – The Basics

- does student loan consolidation affect credit score – Short‑Term Effects

- does student loan consolidation affect credit score – Long‑Term Benefits

- Key Factors That Determine the Credit Score Outcome

- Interest Rate and Monthly Payment

- Loan Term Length

- Credit Utilization on Revolving Accounts

- Timing of the Consolidation

- Practical Tips to Minimize Negative Impacts

- Check Your Credit Report Before Consolidating

- Shop for Consolidation Lenders Within a Short Window

- Maintain Low Balances on Revolving Credit

- Set Up Automatic Payments

- Consider a Shorter Repayment Term If Feasible

- Common Misconceptions About Consolidation and Credit Scores

- My Consolidation Will Instantly Raise My Score

- Closing Old Loans Erases Positive Payment History

- All Consolidation Loans Are the Same

- Consolidation Guarantees a Lower Interest Rate

- When Consolidation Might Not Be the Best Choice

- Resources for Further Reading

Student loan consolidation is a buzzword that shows up whenever you browse personal finance forums or chat with a college‑aged friend about debt management. The idea sounds simple: bundle several loans into one, maybe snag a lower interest rate, and enjoy a single monthly payment. But before you click “apply,” there’s a critical question that pops up again and again: does student loan consolidation affect credit score?

Understanding the answer isn’t just about numbers on a credit report; it’s about how consolidation fits into your broader financial roadmap. Whether you’re fresh out of school, juggling multiple payments, or looking for a fresh start, the impact on your credit score can influence everything from mortgage eligibility to car loan rates.

In this article we’ll break down the mechanics of consolidation, explore short‑term and long‑term credit score effects, and give you practical steps to make the most of the process while safeguarding your credit health.

does student loan consolidation affect credit score – The Basics

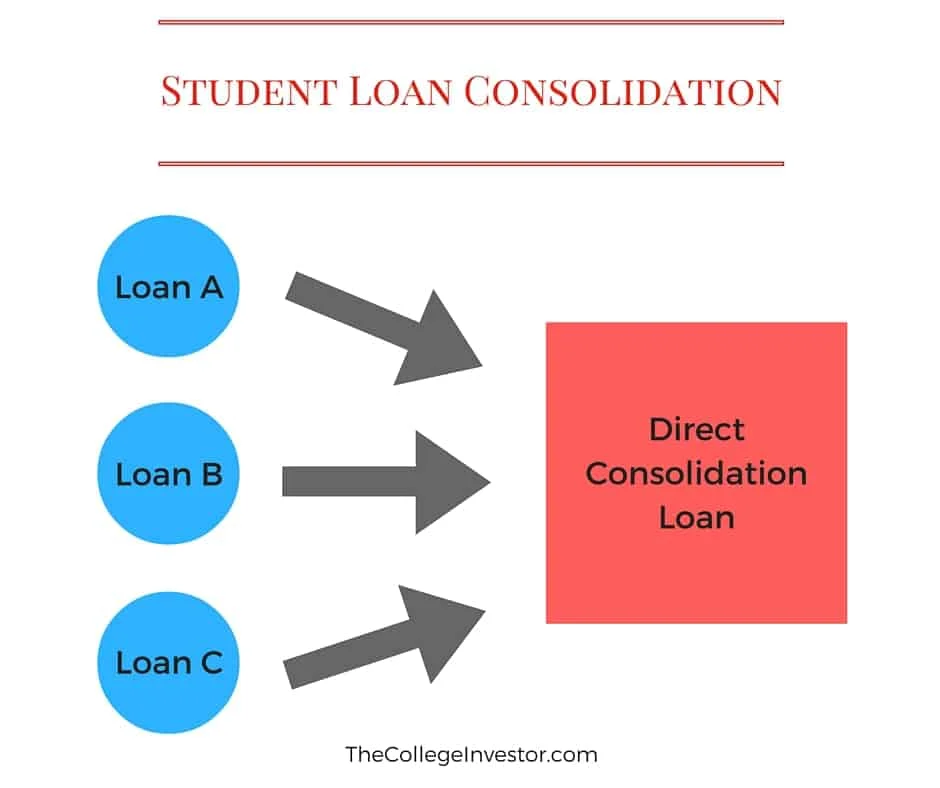

At its core, a consolidation loan is a new credit account that replaces one or more existing student loans. Because a new account is created, the credit bureaus receive a “hard inquiry,” and the old loans are reported as closed. Both actions can cause a ripple in your credit score.

Here’s a quick snapshot of the two main ways the consolidation move can change your score:

- Hard inquiry: When a lender checks your credit to approve the consolidation, it registers as a hard pull, which may knock a few points off your score temporarily.

- Account mix and length: Closing older loans and opening a new one can shorten the average age of your credit accounts, potentially lowering the score in the short run.

However, these are not the whole story. The overall impact depends on how the consolidation alters your payment behavior, credit utilization, and overall debt profile.

does student loan consolidation affect credit score – Short‑Term Effects

In the first month or two after consolidation, you’ll likely see a modest dip in your credit score. This is mostly due to the hard inquiry and the shift in your credit history length. Most credit scoring models treat a hard inquiry as a minor, temporary factor—usually subtracting 5 to 10 points, and the impact fades within 12 months.

Another nuance is the “closed” status of your original loans. When an account is closed, its positive payment history stays on your report for up to 10 years, but the removal of that account can slightly reduce the average age of your credit. If your original loans were several years old, the average age will drop, nudging your score down a bit.

Don’t panic if you notice a short‑term dip. The key is to watch the bigger picture and how your credit behavior evolves post‑consolidation.

does student loan consolidation affect credit score – Long‑Term Benefits

Over time, consolidation can actually boost your credit score if you manage the new loan responsibly. Here’s why:

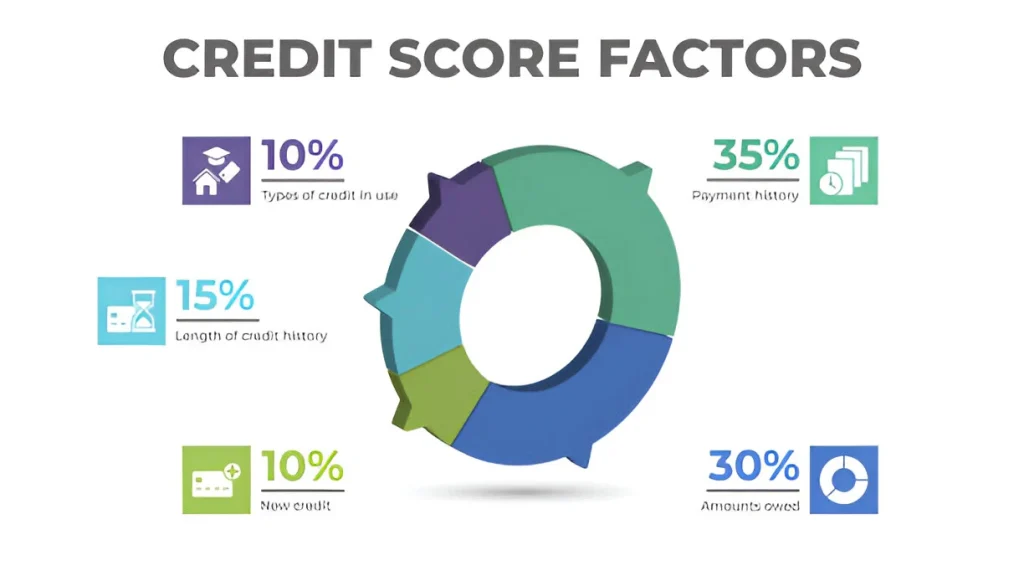

- Payment consistency: A single, lower monthly payment can make it easier to stay current. Consistently paying on time is one of the strongest positive drivers in most credit scoring models.

- Reduced debt‑to‑income ratio: While student loans don’t directly affect credit utilization (since they’re installment loans), a lower overall debt load can improve the “amount owed” factor that some models consider.

- Simplified credit management: Fewer accounts mean fewer chances to miss a payment, which reduces the risk of negative marks that can drag your score down.

In essence, if consolidation leads to better payment habits, the net effect on your credit score will be positive after the initial dip.

Key Factors That Determine the Credit Score Outcome

Not every consolidation story is the same. Several variables shape whether does student loan consolidation affect credit score in a favorable or unfavorable way.

Interest Rate and Monthly Payment

A lower interest rate can shrink your monthly payment, freeing up cash for other obligations or allowing you to pay the consolidation loan faster. Paying down the principal more quickly reduces the total amount of debt, which can be a subtle boost to your credit profile.

Loan Term Length

Extending the repayment term reduces your monthly payment but can increase the total interest you’ll pay over the life of the loan. A longer term also means the loan stays on your credit report for a longer period, which can keep a positive payment history in place—but it also delays the point at which the account is closed, potentially affecting the average age of credit.

Credit Utilization on Revolving Accounts

Although student loans are installment accounts, the overall debt load influences lenders’ perception of risk. If consolidation lowers your total monthly outflow, you may have more room to keep credit card balances low, thereby improving your credit utilization ratio—a critical factor for credit scores.

Timing of the Consolidation

When you apply for consolidation matters. If you’re already planning to apply for a mortgage or auto loan, it might be wise to wait until after those applications are processed. Multiple hard inquiries in a short period can compound the short‑term dip.

Practical Tips to Minimize Negative Impacts

Now that we’ve covered the mechanics, let’s talk strategy. Below are actionable steps to ensure that the answer to does student loan consolidation affect credit score leans toward the positive side.

Check Your Credit Report Before Consolidating

Pull your free credit reports from the three major bureaus. Verify that all your student loans are reported accurately. Errors can cause unnecessary score drops, and fixing them beforehand gives you a clean baseline.

Shop for Consolidation Lenders Within a Short Window

Credit scoring models treat multiple inquiries for the same type of loan (like student loan consolidation) as a single inquiry if they occur within a 30‑day window. This “rate shopping” protection helps you compare offers without piling on hard pulls.

Maintain Low Balances on Revolving Credit

Even though installment loans don’t affect utilization directly, keeping credit cards under 30% of their limits helps offset any temporary score dip from the consolidation inquiry.

Set Up Automatic Payments

Most lenders offer a small interest rate discount for autopay. More importantly, automatic payments reduce the chance of a missed payment, which can cause a severe score drop.

Consider a Shorter Repayment Term If Feasible

If you can afford a slightly higher monthly payment, a shorter term means you’ll pay off the loan faster, which can improve your credit score sooner and reduce total interest paid.

Common Misconceptions About Consolidation and Credit Scores

There’s a lot of myth‑busting to do when it comes to does student loan consolidation affect credit score. Let’s clear up a few of the most frequent misunderstandings.

My Consolidation Will Instantly Raise My Score

Reality check: the positive impact of better payment habits takes time to show up on your credit report. Expect to see improvements after 3‑6 months of on‑time payments, not overnight.

Closing Old Loans Erases Positive Payment History

Closed accounts with good payment history stay on your credit report for up to 10 years. The history doesn’t disappear, but the average age of accounts can shift, causing a temporary dip.

All Consolidation Loans Are the Same

Private lenders, federal Direct Consolidation, and credit union options each have different terms, fees, and reporting practices. Some may report to all three bureaus, while others only to one, influencing how the consolidation appears on your credit file.

Consolidation Guarantees a Lower Interest Rate

While many borrowers secure a better rate, especially if they have strong credit, it’s not a universal rule. Always compare the APR, fees, and repayment terms before deciding.

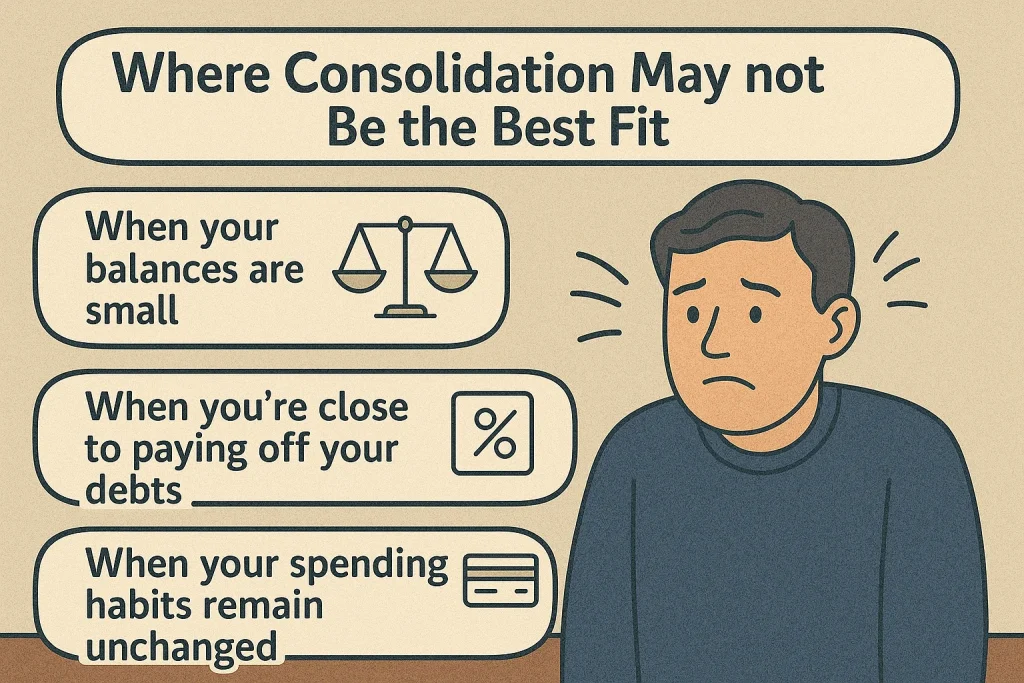

When Consolidation Might Not Be the Best Choice

Even though consolidation can be a powerful tool, there are scenarios where it may not serve your credit goals.

- Eligibility for Income‑Driven Repayment (IDR) Plans: Federal loans offer IDR options that can reduce monthly payments without affecting your credit score. Consolidating into a private loan would eliminate those benefits.

- Existing Low Interest Rates: If you already have a low rate on a federal loan, moving to a private lender could increase your interest cost, offsetting any credit score gains.

- Upcoming Major Credit Applications: If you’re planning to buy a home or car soon, the hard inquiry and temporary dip could affect loan approval odds.

If any of these points resonate, it might be worth exploring alternatives like refinancing (instead of consolidation) or applying for an IDR plan.

Resources for Further Reading

To deepen your understanding, check out these related guides:

- Does Consolidating Student Loans Affect Credit Score? A Complete Guide

- What is Grace Period for Student Loans? Everything You Need to Know

- Income Limit for Student Loan Interest Deduction Explained

By staying informed and planning strategically, you can answer the central question—does student loan consolidation affect credit score—with confidence, turning a potential credit challenge into a stepping stone toward stronger financial health.

Remember, the goal isn’t just to consolidate for the sake of convenience; it’s to create a sustainable repayment path that keeps your credit score climbing and your financial stress shrinking. Keep an eye on your credit reports, maintain disciplined payment habits, and use consolidation as one of many tools in your financial toolkit.

[ CATEGORY ]: Finance