Table of Contents

- Why Consider Refinance Student Loans for 30 Years?

- How Refinance Student Loans for 30 Years Impacts Total Interest

- Eligibility and Credit Considerations

- Refinance Student Loans for 30 Years: Choosing the Right Lender

- Step‑by‑Step Process to Refinance Student Loans for 30 Years

- Tips to Maximize Savings While Refinancing Student Loans for 30 Years

- Potential Pitfalls and How to Avoid Them

- When a 30‑Year Term Makes Sense

- Alternative Strategies to Consider

Student debt can feel like a marathon, especially when the repayment schedule stretches out for a decade or more. For many borrowers, the idea of extending that timeline to 30 years may sound like a lifeline—lower monthly payments, more breathing room, and a chance to keep other financial goals alive. But before you click “apply,” it helps to understand what it really means to refinance student loans for 30 years, how it impacts your overall financial picture, and which strategies can keep you from paying unnecessary interest.

In this guide we’ll walk through the mechanics of a 30‑year refinance, compare it to traditional 10‑ or 20‑year plans, and give you a toolbox of tips to make the decision feel less like a gamble and more like a calculated move. Whether you’re a recent graduate just starting out, a mid‑career professional juggling a mortgage, or someone who’s been in repayment for years, the information below can help you weigh the trade‑offs with clarity.

Before we dive deep, remember that refinancing is not a one‑size‑fits‑all solution. Your credit score, income stability, and long‑term goals all play a part. If you’re curious about how loan servicers work or want to see how the military might affect your repayment options, check out How to Find My Student Loan Servicer – A Step‑by‑Step Guide for a quick primer.

Why Consider Refinance Student Loans for 30 Years?

Extending the repayment term to 30 years can be a strategic move when cash flow is tight. Here are the main reasons borrowers explore this option:

- Lower Monthly Payments: Spreading the principal over three decades reduces the amount due each month, freeing up money for rent, utilities, or emergency savings.

- Predictable Budgeting: A fixed-rate 30‑year loan locks in a consistent payment, which can simplify budgeting compared to variable federal loan terms.

- Improved Debt‑to‑Income Ratio: Smaller monthly obligations can make you look more favorable to lenders if you plan to apply for a mortgage or car loan later.

- Flexibility for Life Events: If you anticipate periods of reduced income—like going back to school, starting a family, or taking a career break—a longer term provides a safety net.

However, the trade‑off is paying more interest over the life of the loan. A 30‑year term can add thousands, sometimes tens of thousands, of dollars in total interest compared to a 10‑year repayment schedule. The key is to decide whether the immediate cash‑flow relief outweighs the long‑term cost.

How Refinance Student Loans for 30 Years Impacts Total Interest

Let’s break down the math with a simple example. Suppose you have $40,000 in student debt at an interest rate of 5.5%. If you refinance with a 10‑year term, your monthly payment would be about $434, and you’d pay roughly $5,100 in interest total. Stretch that same loan to 30 years at the same rate, and the monthly payment drops to $226, but the total interest climbs to about $42,000. That’s a $36,900 difference—a stark illustration of the “cost of convenience.”

Of course, the actual numbers depend on the rate you secure. If you can lock in a lower rate (say 4.0% instead of 5.5%) the interest gap narrows, but it rarely disappears entirely. This is why many borrowers use a 30‑year refinance as a short‑term bridge, intending to refinance again later when their financial situation improves.

Eligibility and Credit Considerations

Most private lenders require a minimum credit score—usually around 660—for the most competitive rates. However, some lenders will still approve borrowers with lower scores, albeit at higher interest rates. Here’s what lenders typically look at:

- Credit Score: Higher scores translate to lower rates. A score of 720+ often lands you the best terms.

- Debt‑to‑Income (DTI) Ratio: Lenders prefer a DTI under 36%, though a 30‑year term can help keep your DTI lower.

- Employment History: Stable employment for at least two years demonstrates repayment reliability.

- Loan Balance: Most lenders set a minimum balance (often $5,000) and a maximum (commonly $500,000) for refinance eligibility.

If your credit isn’t where you’d like it to be, consider taking a few months to improve it—pay down revolving debt, correct any errors on your credit report, and avoid new credit inquiries. The effort can shave off a full percentage point or more on the interest rate, dramatically reducing the total cost even on a 30‑year term.

Refinance Student Loans for 30 Years: Choosing the Right Lender

When scouting lenders, compare the following factors:

- APR vs. Interest Rate: The APR includes fees and gives a clearer picture of the true cost.

- Origination Fees: Some lenders charge 1‑2% up front, which can be rolled into the loan.

- Prepayment Penalties: A good 30‑year refinance should let you pay off early without fees.

- Customer Service: Look for reviews on how responsive the servicer is—important if you need to modify payments later.

For a deeper dive into managing loan servicers, you might find the article Granite State Management Resources Student Loans – Your Complete Guide helpful.

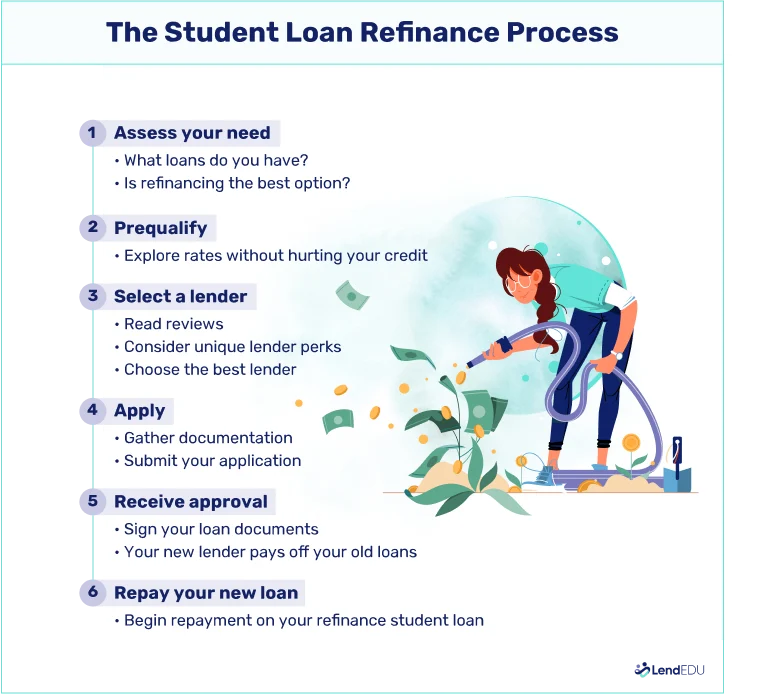

Step‑by‑Step Process to Refinance Student Loans for 30 Years

Ready to start? Follow this roadmap to keep the process smooth:

- Gather Your Current Loan Details: Note the balances, interest rates, and servicer contact info for each loan you hold.

- Check Your Credit Report: Pull a free copy from AnnualCreditReport.com and address any inaccuracies.

- Shop Around: Use comparison tools, request quotes from at least three lenders, and ask for a “30‑year term” quote specifically.

- Calculate the True Cost: Use an online amortization calculator to see monthly payment, total interest, and break‑even points for each offer.

- Apply Online: Most lenders let you submit documents digitally—pay stubs, tax returns, and ID.

- Close the Deal: Review the final loan agreement, confirm there are no hidden fees, and sign.

- Set Up Automatic Payments: Many lenders offer a 0.25% rate discount for autopay, which can shave off a few hundred dollars over 30 years.

- Notify Your Old Servicer: Once the new loan is funded, the old servicer will close out the account. Keep a copy of the final payoff statement for your records.

Even after you’ve locked in a 30‑year term, keep an eye on the market. If rates drop dramatically, you can refinance again to a shorter term or a lower rate—this is often called “refi‑refi.”

Tips to Maximize Savings While Refinancing Student Loans for 30 Years

- Lock In a Low Rate Early: If you anticipate rates climbing, securing a low rate now—even for 30 years—can protect you from future hikes.

- Combine Federal and Private Loans: Consolidating both types into a single private loan simplifies payments but consider losing federal protections (like income‑driven repayment plans).

- Make Extra Payments When Possible: Any surplus can be applied directly to the principal, shortening the effective loan life without altering the scheduled term.

- Use Tax‑Deductible Interest: If your adjusted gross income (AGI) is below the threshold, you may deduct up to $2,500 of student loan interest annually. A longer term may increase the amount of interest you can deduct each year, though the overall deduction limit still applies.

- Watch for Refinancing Promotions: Some lenders run limited‑time offers with zero origination fees or reduced rates for new customers.

Potential Pitfalls and How to Avoid Them

While the idea of a gentle $200‑something monthly payment can be tempting, there are several red flags to watch for:

- Loss of Federal Benefits: By moving to a private lender, you surrender access to income‑driven repayment plans, deferment options, and loan forgiveness programs.

- Higher Total Cost: As illustrated earlier, a 30‑year term can dramatically increase the amount of interest you pay.

- Variable vs. Fixed Rates: Some lenders only offer variable rates on long terms. If rates rise, your payment could increase substantially.

- Hidden Fees: Origination fees, late payment penalties, and prepayment penalties can erode the savings you expect.

If you’re a service member or veteran, there are special considerations. For instance, the military sometimes offers loan repayment assistance that could be more advantageous than a 30‑year refinance. Learn more in Will the Military Pay Student Loans? Everything You Need to Know.

When a 30‑Year Term Makes Sense

A 30‑year refinance is most appropriate when:

- You have irregular income streams (freelancers, gig workers) and need a low, predictable payment.

- You’re approaching retirement and want to keep debt manageable without draining savings.

- You’re using the cash flow to address higher‑interest debt, like credit cards, which can provide a net savings.

- You plan to refinance again in a few years once your credit improves or rates drop.

Alternative Strategies to Consider

If the thought of paying extra interest over three decades makes you uneasy, explore these alternatives before committing to a 30‑year refinance:

- Income‑Driven Repayment (IDR) Plans: Federal loans offer plans that cap payments at a percentage of discretionary income, often extending the term to 20‑25 years with possible forgiveness.

- Partial Consolidation: Keep a high‑interest loan separate and refinance only the lower‑interest portion for a shorter term.

- Side‑Hustle Income: Use extra earnings to make occasional lump‑sum payments, reducing the principal faster without altering the term.

- Employer Tuition Assistance: Some companies reimburse student loan payments as a benefit—check HR policies.

Each of these paths can help you manage debt without locking yourself into a lengthy payment schedule. The right choice depends on your personal financial landscape.

In the end, refinancing student loans for 30 years is a tool—not a cure. By understanding the cost, evaluating your credit, and weighing the pros and cons, you can decide whether a low monthly payment outweighs the extra interest. Keep reviewing your situation annually; life changes, and so do loan products. With the right approach, you’ll stay in control of your debt and keep your financial goals within reach.

[Finance]: Finance