Table of Contents

- Understanding liability insurance for real estate agents

- Key components of liability insurance for real estate agents

- How much does liability insurance for real estate agents cost?

- Choosing the right policy – tips for agents

- Common scenarios where liability insurance for real estate agents pays off

- Undisclosed material facts

- Misrepresentation of property boundaries

- Failure to meet contractual deadlines

- Cyber breaches and data loss

- Integrating liability insurance into your overall business strategy

- Standardize documentation and disclosure practices

- Leverage technology to minimize errors

- Partner with a knowledgeable broker

Working as a real‑estate agent isn’t just about showing houses, negotiating offers, and closing deals. Behind the scenes, every transaction carries a risk of disputes, lawsuits, or claims that could hit your pocket hard. That’s where liability insurance steps in, acting as a financial safety net when things go sideways.

Imagine a client sues you because a property they bought later turned out to have undisclosed structural issues. Or picture a fellow agent accusing you of negligence after a missed deadline caused a deal to fall apart. In both scenarios, the costs of legal defense, settlements, or judgments can quickly outstrip a single agent’s savings.

In this guide we’ll explore why liability insurance for real estate agents is more than a nice‑to‑have add‑on—it’s a critical component of a sustainable business. From the basics of what the policy actually covers to tips on picking the right provider, you’ll walk away with a clear roadmap to protect yourself, your clients, and your reputation.

Understanding liability insurance for real estate agents

Liability insurance for real estate agents, sometimes called errors‑and‑omissions (E&O) insurance, is designed to shield agents from financial loss arising from professional mistakes. Unlike general commercial liability, which covers bodily injury or property damage caused by your business operations, E&O focuses on claims that allege negligence, misrepresentation, or failure to perform professional duties.

Most states either require agents to carry a minimum level of coverage or strongly recommend it as part of a brokerage’s risk‑management policy. Even in states where it isn’t mandatory, the cost of a single lawsuit can dwarf the annual premium, making the investment a smart move for anyone serious about a long‑term career.

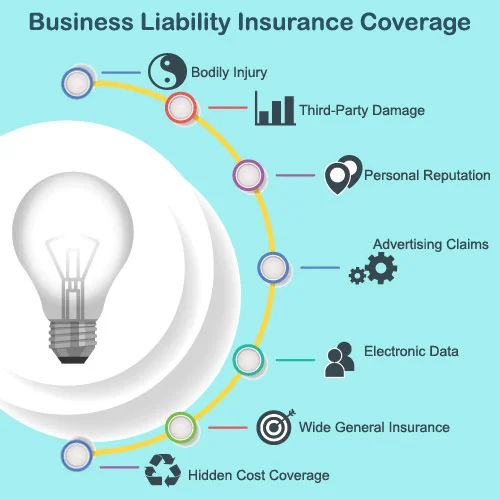

Key components of liability insurance for real estate agents

- Professional liability (E&O): Covers legal defense costs and settlements when a client claims you made an error, omitted critical information, or gave negligent advice.

- General liability: Protects against third‑party bodily injury or property damage occurring on your premises or during business activities.

- Cyber liability: As agents increasingly handle digital documents and client data, this coverage helps with breach response, data restoration, and liability from privacy violations.

- Pollution liability (optional): Useful for agents dealing with older properties where environmental hazards might be discovered after a sale.

When you compare policies, look for clear definitions of “covered acts,” any exclusions (like intentional misconduct), and the limits of liability. A typical policy might offer $1 million per claim with a $1 million aggregate limit, but high‑volume agents often opt for higher caps.

How much does liability insurance for real estate agents cost?

The premium you pay depends on several factors:

- Experience level: New agents usually face higher rates because they lack a track record.

- Transaction volume: The more deals you close each year, the greater the perceived risk.

- Geographic location: States with higher litigation rates or stricter regulations can drive up costs.

- Coverage limits and deductibles: Higher limits protect you better but raise the premium; a larger deductible can lower the monthly cost.

On average, a solo agent might pay anywhere from $400 to $1,200 annually for a basic E&O policy. Larger brokerages often negotiate group rates that bring the cost down per agent.

Choosing the right policy – tips for agents

Here are some practical steps to ensure you pick a policy that truly fits your business:

- Assess your risk profile: List the types of transactions you handle most often (residential, commercial, luxury) and any specialized services you provide, such as property management or investment consulting.

- Read the fine print: Look for exclusions that could catch you off guard. For instance, some policies exclude claims arising from “known defects” that were not disclosed.

- Check the insurer’s reputation: A low‑cost policy is tempting, but you’ll want an insurer with a proven track record of handling real‑estate claims promptly.

- Bundle with other coverages: Many carriers offer discounts if you combine E&O with general liability, cyber, or even workers’ compensation.

- Review annually: Your business can change quickly—new staff, higher sales volume, or expanded service areas may require adjustments to your limits.

For agents who rely heavily on digital marketing and lead generation, protecting yourself against data‑related mishaps is increasingly important. In fact, pairing liability coverage with a robust top real estate lead generation companies strategy can reduce the chance of errors that lead to client complaints.

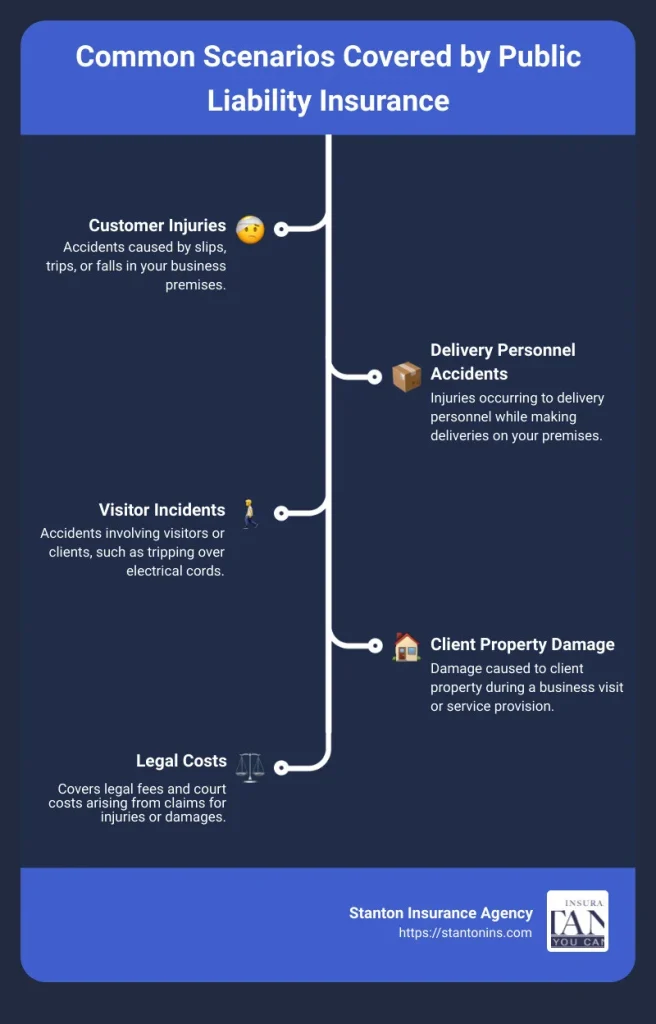

Common scenarios where liability insurance for real estate agents pays off

Understanding real‑world situations where your policy can save the day helps you appreciate its value. Below are a few frequent claim triggers:

Undisclosed material facts

A buyer discovers after closing that the roof has a hidden leak. They claim you failed to disclose the issue, even though you relied on the seller’s disclosure forms. Your E&O coverage can cover the legal defense and any settlement up to the policy limit.

Misrepresentation of property boundaries

During a commercial lease negotiation, an agent mistakenly provides an inaccurate lot line map. The tenant later discovers the error, leading to a costly redesign. Liability insurance for real estate agents steps in to cover the resulting claim.

Failure to meet contractual deadlines

Time is money in real estate. Missing a financing deadline can cause a deal to fall through, prompting the buyer to sue for lost opportunity costs. A solid policy will help with attorney fees and any awarded damages.

Cyber breaches and data loss

Agents store sensitive client information—social security numbers, bank details, and contract drafts—on cloud platforms. A ransomware attack that encrypts these files could result in a privacy lawsuit. Cyber liability coverage, often an add‑on to your E&O, handles the costs of notification, credit monitoring, and legal defense.

By reviewing these scenarios, you’ll see why a comprehensive liability insurance for real estate agents plan is not just a box‑checking exercise—it’s a safeguard against the unpredictable nature of the market.

Integrating liability insurance into your overall business strategy

Insurance should be part of a broader risk‑management framework. Here are three ways to weave liability coverage into everyday operations:

Standardize documentation and disclosure practices

Develop checklists for each transaction stage. Clear, written disclosures reduce the likelihood of omissions that could trigger a claim. Training your team on these protocols also demonstrates due diligence, which can be a favorable factor if a lawsuit arises.

Leverage technology to minimize errors

Automation tools—such as a bookkeeping software for real estate agents or a CRM platform—ensure data consistency across listings, client communication, and contract generation. When information flows accurately, the chances of misrepresentation drop dramatically.

Partner with a knowledgeable broker

A specialized insurance broker who understands the real‑estate industry can tailor a policy that reflects your specific exposures. They’ll also keep you informed about regulatory changes that might affect required coverage levels.

Finally, keep an open line of communication with your brokerage’s compliance officer (if you work for one). Many brokerages already have a master E&O policy, and you may only need to purchase a supplemental rider for unique services you offer.

In short, liability insurance for real estate agents isn’t an isolated product; it works best when combined with solid procedures, tech tools, and professional guidance.

Whether you’re just starting out or managing a seasoned team, taking the time to understand your coverage, evaluate risk, and embed protective habits into your workflow will pay dividends in confidence—and in your bottom line. So, review your current policy, ask the right questions, and make adjustments before the next deal goes on the market.

Remember, the goal isn’t to eliminate risk entirely—something no insurance can do—but to ensure that when the unexpected happens, you have a sturdy safety net that lets you keep focusing on what you do best: matching people with their perfect homes.