Table of Contents

- american funds 2030 target date retirement fund: Overview and Core Features

- american funds 2030 target date retirement fund: Asset Allocation Timeline

- Key Benefits of the american funds 2030 target date retirement fund

- Costs and Fees: What to Expect

- How the american funds 2030 target date retirement fund Fits into a Diversified Portfolio

- Choosing the Right Share Class and Account Type

- Tax Implications of the american funds 2030 target date retirement fund

- Performance Track Record: What the Numbers Say

- Comparing the american funds 2030 target date retirement fund to Other Options

- Practical Tips for Getting the Most Out of Your Investment

- Using CRM Systems to Track Your Investment Goals

- When Might You Switch Away from the american funds 2030 target date retirement fund?

When it comes to planning for a comfortable retirement, the sheer number of investment options can feel overwhelming. From individual stocks to complex annuities, every choice carries its own set of risks and rewards. One popular solution that many investors gravitate toward is a target‑date fund—particularly those offered by reputable managers like American Funds. If you’re aiming to retire around the early 2030s, the american funds 2030 target date retirement fund often lands near the top of recommendation lists.

But why does this specific fund attract both seasoned retirees and younger savers alike? The answer lies in its blend of simplicity, professional management, and a glide‑path that automatically shifts toward more conservative assets as the target year approaches. In this article, we’ll peel back the layers of the american funds 2030 target date retirement fund, explore its underlying strategy, examine costs, and discuss how it fits into a broader retirement plan. Whether you’re a first‑time investor or someone looking to rebalance your portfolio, you’ll find actionable insights to help you decide if this fund deserves a spot in your retirement toolbox.

Before diving into the nitty‑gritty, it’s worth noting that no single fund can guarantee a perfect retirement outcome. Market volatility, personal financial changes, and tax considerations all play a role. The goal of a target‑date fund is to provide a “set‑and‑forget” approach that aligns with your expected retirement year, while still offering diversification and professional oversight. With that in mind, let’s explore what makes the american funds 2030 target date retirement fund a compelling choice for many.

american funds 2030 target date retirement fund: Overview and Core Features

The american funds 2030 target date retirement fund is part of American Funds’ larger American Funds Target Date Series. Designed for investors planning to retire around 2030, the fund follows a predefined glide‑path that gradually reduces exposure to equities and increases allocation to fixed‑income and cash equivalents as the target date nears.

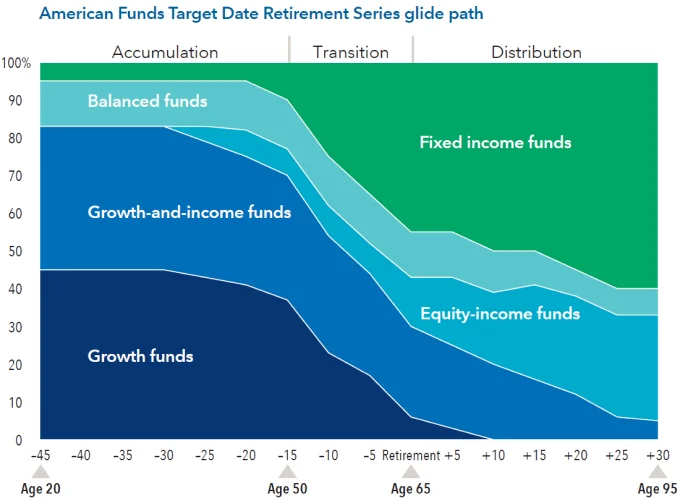

american funds 2030 target date retirement fund: Asset Allocation Timeline

Understanding the fund’s asset allocation is key to grasping its risk profile. Below is a simplified timeline of how the mix typically evolves:

- 2024‑2026 (Early Stage): Approximately 80% equities, 20% fixed income.

- 2027‑2029 (Mid‑Stage): Around 65% equities, 30% fixed income, 5% cash.

- 2030 (Target Year): Roughly 45% equities, 45% fixed income, 10% cash.

- Post‑2030 (Retirement Phase): The fund continues to shift, often ending up with roughly 30% equities and 70% fixed income/cash.

This glide‑path is designed to preserve capital as you transition from the accumulation phase to the distribution phase of retirement. It automatically rebalances each quarter, sparing you the need to constantly adjust your holdings.

Key Benefits of the american funds 2030 target date retirement fund

Several features make the american funds 2030 target date retirement fund stand out:

- Professional Management: A team of seasoned portfolio managers actively monitors market conditions and makes tactical adjustments within the broader glide‑path.

- Diversification: The fund invests across multiple asset classes, sectors, and geographic regions, reducing concentration risk.

- Automatic Rebalancing: Quarterly rebalancing keeps the portfolio aligned with the intended risk level.

- Low Turnover: Compared to actively managed mutual funds, turnover is moderate, which can help mitigate tax impacts.

- Accessibility: Available through most major brokerage platforms, retirement accounts, and employer 401(k) plans.

Costs and Fees: What to Expect

Like any investment vehicle, fees matter. The american funds 2030 target date retirement fund typically carries a blended expense ratio that includes the management fee, administrative costs, and any underlying fund expenses. As of the latest prospectus, the expense ratio hovers around 0.75%—a figure that sits comfortably in the middle of the industry range for target‑date funds.

It’s important to differentiate between the expense ratio and any potential sales loads. Some versions of the fund are no‑load, while others, particularly those purchased through certain broker‑dealers, may include a front‑end or back‑end load. Always check the share class (e.g., Investor Class vs. Advisor Class) to understand the exact cost structure.

How the american funds 2030 target date retirement fund Fits into a Diversified Portfolio

While a target‑date fund offers a one‑stop solution, many investors choose to supplement it with other assets to fine‑tune risk exposure. For example, if you already own a substantial amount of real estate holdings, you might want to adjust the equity portion of the american funds 2030 target date retirement fund to avoid over‑weighting the market.

If you’re interested in how real estate can complement your retirement portfolio, check out our guide on building a real estate website. The synergy between passive income from property and the systematic growth of a target‑date fund can create a resilient retirement strategy.

Choosing the Right Share Class and Account Type

The american funds 2030 target date retirement fund is offered in several share classes, each tailored to different investor needs:

- Investor Class (A‑Shares): Typically lower expense ratios but may carry a front‑end load.

- Adviser Class (C‑Shares): No front‑end load, but slightly higher expense ratios; often used in employer‑sponsored plans.

- Institutional Class (I‑Shares): Designed for large‑scale investors, offering the lowest expense ratios.

When selecting a share class, consider where you’re purchasing the fund. If it’s through a 401(k) or a Roth IRA, the adviser or institutional class may be the most cost‑effective. For a direct brokerage account, you might weigh the load against the long‑term expense savings.

Tax Implications of the american funds 2030 target date retirement fund

Target‑date funds generate taxable events in the form of capital gains, dividends, and interest. Holding the fund in a tax‑advantaged account (like a 401(k), Traditional IRA, or Roth IRA) can shield you from annual tax liabilities and let the investment compound more efficiently.

If you’re investing outside a retirement account, be mindful of the fund’s distribution schedule. The annual IRS Form 1099 will detail taxable income, and you may need to plan for quarterly estimated tax payments if the distribution is substantial.

Performance Track Record: What the Numbers Say

Historical performance is not a guarantee of future results, but it offers valuable context. Over the past five years, the american funds 2030 target date retirement fund has delivered an average annual return of roughly 7.5%, outperforming many peers in the same target‑date category. This performance reflects a balanced exposure to both growth‑oriented equities and stable fixed‑income securities.

During market downturns, such as the 2020 COVID‑19 crash, the fund’s diversified nature helped cushion losses. While equity allocations dipped, the fixed‑income portion provided a buffer, resulting in a smaller overall drawdown compared to a pure equity fund.

Comparing the american funds 2030 target date retirement fund to Other Options

When evaluating alternatives, consider these common competitors:

- Vanguard Target Retirement 2035 Fund (VTTHX): Slightly later target date, lower expense ratio (~0.15%).

- Fidelity Freedom 2030 Fund (FELDX): Similar glide‑path, expense ratio around 0.70%.

- T. Rowe Price Retirement 2030 Fund (TRRCX): Higher equity tilt in early years, expense ratio about 0.80%.

Each has its own philosophy, but the american funds 2030 target date retirement fund stands out for its active management approach and robust research resources.

Practical Tips for Getting the Most Out of Your Investment

Here are a few actionable steps to ensure the american funds 2030 target date retirement fund works effectively within your retirement plan:

- Set Clear Goals: Define your desired retirement age, lifestyle expectations, and risk tolerance before committing.

- Review Annually: Even though the fund rebalances automatically, a yearly review helps you stay aligned with any life changes (e.g., marriage, job loss, inheritance).

- Consider a “Core‑Satellite” Approach: Use the target‑date fund as your core holding and add satellite positions—like a REIT or a small‑cap stock—to customize exposure.

- Leverage Tax‑Advantaged Accounts: Maximize contributions to 401(k)s and IRAs before investing in taxable brokerage accounts.

- Stay Informed: Follow fund updates and quarterly reports from American Funds to understand any strategic shifts.

Speaking of diversification, many investors pair their retirement accounts with real‑estate investments. If you’re curious about how a real‑estate agent can help you find properties that generate passive income, our real estate agent guide offers practical steps to get started.

Using CRM Systems to Track Your Investment Goals

Staying organized is half the battle. While a CRM system is traditionally used for sales pipelines, it can also help you monitor financial milestones. Our article on CRM systems for real estate agents outlines how customizable dashboards can be repurposed for personal finance tracking, ensuring you never miss a contribution deadline or rebalancing window.

When Might You Switch Away from the american funds 2030 target date retirement fund?

Even the best‑designed fund isn’t a lifelong commitment for everyone. Consider these scenarios where you might transition to a different strategy:

- Changing Retirement Timeline: If you decide to retire earlier or later than 2030, a fund with a closer or farther target date may better align with your timeline.

- Risk Appetite Shifts: As you accumulate wealth, you may want to take on more or less risk than the fund’s glide‑path provides.

- Higher Fees: If a lower‑cost competitor emerges, switching could improve net returns over the long term.

- Portfolio Rebalancing Needs: Adding specialized assets—like a direct real‑estate investment or a private equity stake—might require moving a portion of your holdings out of the target‑date fund.

In any case, a thoughtful review with a financial advisor can ensure you make a move that aligns with both short‑term cash flow needs and long‑term retirement aspirations.

Ultimately, the american funds 2030 target date retirement fund offers a convenient, professionally managed pathway for investors targeting retirement around the early 2030s. Its blend of diversified assets, automatic rebalancing, and moderate fees make it a solid foundation for many retirement portfolios. By understanding its mechanics, costs, and how it interacts with other investments—like real estate—you can confidently decide whether this fund belongs in your retirement plan.

[Finance]: Finance