Table of Contents

- vanguard target retirement 2035 fund vtthx – Overview and Core Features

- vanguard target retirement 2035 fund vtthx – Asset Allocation Strategy

- Performance Snapshot – How Has VTTHX Performed?

- Why Choose Vanguard’s Target‑Date Funds?

- Comparing VTTHX to Other Target‑Date Options

- Who Should Consider VTTHX?

- Practical Tips for Getting the Most Out of VTTHX

- 1. Stick to the Target Date

- 2. Combine with Other Accounts for Flexibility

- 3. Review Periodically, Not Weekly

- 4. Watch the Expense Ratio

- Potential Drawbacks to Keep in Mind

- How to Invest in VTTHX

- Tax Considerations

- Future Outlook – What’s Next for VTTHX?

When it comes to planning a comfortable retirement, many investors lean on target‑date funds for their “set‑and‑forget” simplicity. Among the crowded arena of options, the Vanguard Target Retirement 2035 Fund (VTTHX) often pops up as a solid, low‑cost choice for those aiming to retire around the mid‑2030s. But what exactly makes this fund tick, and is it the right fit for your portfolio?

In this article we’ll unpack the nuts and bolts of VTTHX—its asset allocation, historical performance, fee structure, and the underlying philosophy that Vanguard uses to glide investors smoothly toward retirement. We’ll also compare it with a few peers, talk about who should consider adding it to their plan, and share some practical tips to make the most of a target‑date strategy.

Whether you’re a seasoned saver or just starting to think about your retirement timeline, understanding the Vanguard Target Retirement 2035 Fund VTTHX can help you make an informed decision that aligns with your risk tolerance and long‑term goals.

vanguard target retirement 2035 fund vtthx – Overview and Core Features

The Vanguard Target Retirement 2035 Fund VTTHX is part of Vanguard’s broad lineup of target‑date mutual funds. Designed for investors who expect to retire around the year 2035, VTTHX automatically adjusts its asset mix over time—starting with a higher allocation to equities for growth and gradually shifting toward bonds as the target date approaches.

Key characteristics include:

- Fund Type: Target‑date mutual fund (share class VTTHX)

- Inception Date: June 2007

- Management Style: Passive index‑based with a strategic glide‑path

- Expense Ratio: 0.15% (as of 2024), one of the lowest in its peer group

- Investment Minimum: $3,000 for a regular account

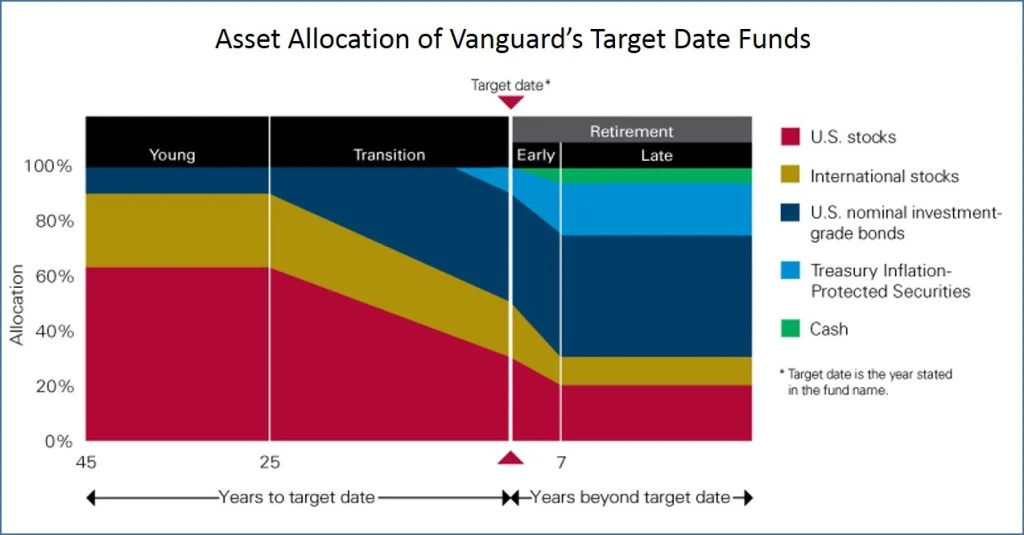

vanguard target retirement 2035 fund vtthx – Asset Allocation Strategy

The fund’s glide‑path is anchored to Vanguard’s “LifeStrategy” philosophy, which balances risk and return through a diversified mix of U.S. stocks, international stocks, U.S. bonds, and international bonds. As of the latest quarterly update, the allocation looks roughly like this:

- U.S. equities: 45%

- International equities: 25%

- U.S. investment‑grade bonds: 20%

- International investment‑grade bonds: 10%

When you’re several years away from 2035, the fund leans more heavily on equities to capture growth. As the target date nears, Vanguard automatically reduces equity exposure, adding more bonds to preserve capital and dampen volatility.

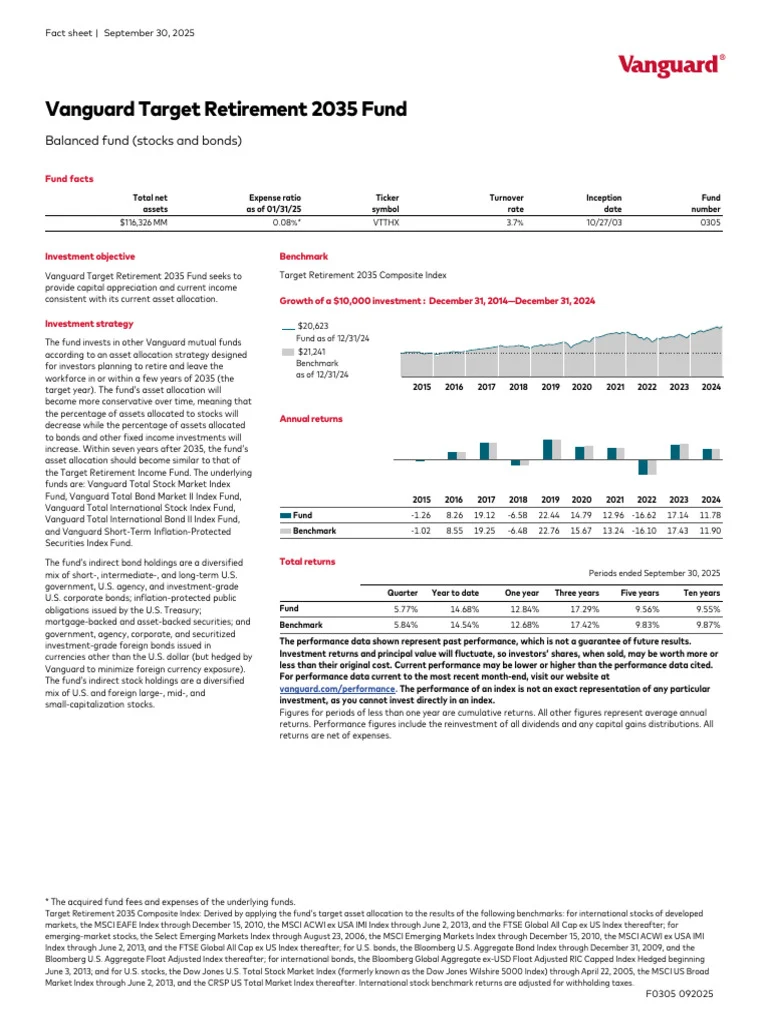

Performance Snapshot – How Has VTTHX Performed?

While past performance isn’t a guarantee of future results, it does provide a useful benchmark. Over the past 10 years, VTTHX has delivered an average annual return of about 9.2%, outperforming many comparable target‑date funds with higher expense ratios. During market downturns, such as the sharp dip in early 2020, VTTHX’s diversified allocation helped cushion losses relative to pure‑stock funds.

It’s also worth noting that the fund’s low expense ratio contributes directly to net returns. When you compare VTTHX to a similar fund with a 0.50% expense ratio, the difference in compounded returns over a 20‑year horizon can amount to several percentage points—an impact that becomes especially pronounced in retirement accounts where every basis point counts.

Why Choose Vanguard’s Target‑Date Funds?

Vanguard’s reputation for low costs and investor‑first philosophy is a big draw. Here’s why the Vanguard Target Retirement 2035 Fund VTTHX often stands out:

- Cost Efficiency: At 0.15%, the expense ratio is well below the industry average, meaning more of your money stays invested.

- Automatic Rebalancing: The fund’s glide‑path automatically rebalances each quarter, removing the need for manual adjustments.

- Broad Diversification: Exposure to both domestic and international equities and bonds reduces concentration risk.

- Transparent Management: Vanguard publishes the exact index composition and the glide‑path methodology, so you know what you’re getting.

Comparing VTTHX to Other Target‑Date Options

If you’re shopping around, you’ll likely encounter similar funds from other providers—Fidelity, T. Rowe Price, and American Funds, to name a few. For a direct side‑by‑side, consider the American Funds 2030 Target Date Retirement Fund: A Complete Guide. While the American Funds offering has a slightly higher expense ratio (around 0.55%) and a more active management style, it also includes a higher allocation to small‑cap value stocks, which can add both upside potential and volatility.

When comparing, keep an eye on three main factors:

- Expense Ratio: Lower fees generally translate to higher net returns over time.

- Glide‑Path Design: Some funds shift to bonds earlier or later than Vanguard’s model. Choose a timeline that matches your risk comfort.

- Underlying Indexes: Vanguard uses well‑known indexes (e.g., Vanguard Total Stock Market Index), while other providers may use proprietary blends.

Who Should Consider VTTHX?

The Vanguard Target Retirement 2035 Fund VTTHX is best suited for investors who:

- Plan to retire roughly between 2033 and 2037.

- Prefer a hands‑off approach and trust a systematic glide‑path.

- Value low fees and want to keep more of their investment gains.

- Have a moderate risk tolerance—enough to handle equity volatility but not so aggressive as to stay fully invested in stocks.

If you’re younger than 30 and have a longer horizon, you might look at the Vanguard Target Retirement 2050 or 2060 funds, which keep equity exposure higher for a longer period. Conversely, if you’re already approaching retirement, the Vanguard Target Retirement 2025 fund could be more appropriate.

Practical Tips for Getting the Most Out of VTTHX

1. Stick to the Target Date

It can be tempting to “beat” the fund’s glide‑path by adding more equities early on, but the whole point of a target‑date fund is to automate risk management. Deviating from the preset allocation may expose you to unnecessary risk.

2. Combine with Other Accounts for Flexibility

If you have a mix of tax‑advantaged accounts (IRA, 401(k)) and taxable accounts, consider using VTTHX in the retirement accounts while holding a more aggressive or tax‑efficient fund in taxable accounts. This layered approach can help you manage tax drag while still benefiting from VTTHX’s low-cost diversification.

3. Review Periodically, Not Weekly

Target‑date funds are built for long‑term investors. A semi‑annual or annual check‑in is sufficient unless your personal circumstances (e.g., job change, inheritance) dramatically shift your financial landscape.

4. Watch the Expense Ratio

Even though VTTHX’s expense ratio is low, it’s still a cost that compounds over decades. If you ever find a comparable fund with a lower fee and a glide‑path you trust, a switch could be worthwhile—but remember that transaction costs and tax implications may offset the savings.

Potential Drawbacks to Keep in Mind

No investment is perfect. Here are a few considerations that might make VTTHX less ideal for some investors:

- One‑Size‑Fits‑All Glide‑Path: The fund follows a standard allocation schedule that may not perfectly match your personal risk appetite.

- Limited Customization: You can’t pick and choose individual holdings; you’re locked into Vanguard’s index blend.

- Market Timing Constraints: Because VTTHX automatically shifts toward bonds as the target date nears, you can’t accelerate the transition if you anticipate a market downturn.

For investors who crave more control or who have specific sector preferences, a self‑directed portfolio of index funds might be a better fit.

How to Invest in VTTHX

Getting started is straightforward:

- Open a Vanguard brokerage or retirement account (or a platform that offers Vanguard funds).

- Deposit at least the minimum investment amount ($3,000 for most accounts).

- Search for “VTTHX” or “Vanguard Target Retirement 2035 Fund” and place a buy order.

- Set up automatic contributions if possible—consistent investing can smooth out market volatility.

If you already hold a Vanguard account, you can simply add VTTHX to your existing portfolio with a few clicks.

Tax Considerations

Because VTTHX is typically held in tax‑advantaged accounts, you’ll usually avoid capital gains taxes on the fund’s internal rebalancing. However, if you hold VTTHX in a taxable brokerage account, any dividends or capital gains distributions will be taxable in the year they’re received. Vanguard’s low turnover helps keep those taxable events to a minimum, but it’s still something to monitor, especially if you’re in a higher tax bracket.

Future Outlook – What’s Next for VTTHX?

Looking ahead, Vanguard is likely to continue refining the glide‑path methodology based on evolving market conditions and investor feedback. The fund’s underlying index holdings are expected to remain largely unchanged, ensuring that VTTHX stays true to its low‑cost, diversified ethos.

As the 2035 horizon approaches, you can expect the equity portion to shrink incrementally each quarter, while the bond allocation grows. This gradual shift is designed to protect the accumulated nest egg from the heightened volatility that typically accompanies retirement spending.

For those who are curious about how other target‑date strategies compare, the Build a Real Estate Website with IDX and CRM – The Complete Playbook article, while unrelated to investing, demonstrates the value of systematic planning—a principle that also underpins the design of VTTHX.

In summary, the Vanguard Target Retirement 2035 Fund VTTHX offers a compelling mix of low fees, diversified exposure, and a well‑designed glide‑path that can serve as the backbone of a retirement plan for anyone targeting the mid‑2030s. By understanding its structure, keeping an eye on your own risk tolerance, and staying disciplined with contributions, you can let VTTHX do the heavy lifting while you focus on other aspects of your financial life.