Table of Contents

- s set up an individual retirement account

- s set up an individual retirement account – Choosing the Right Type

- Eligibility and Contribution Limits

- Step‑by‑Step: How to s set up an individual retirement account

- Common Pitfalls to Avoid When s set up an individual retirement account

- Tax Implications of s set up an individual retirement account

- Integrating IRA Contributions with Other Retirement Plans

- Managing Your IRA Over Time

- When to Take Distributions and How to Minimize Taxes

Planning for retirement can feel like navigating a maze, especially when you’re juggling a career, family, and everyday expenses. One of the most straightforward ways to cut through the confusion is to open an Individual Retirement Account (IRA). An IRA gives you a tax‑advantaged vehicle to grow your savings over decades, and the good news is that you don’t need a corporate sponsor or a complicated enrollment process. In this article we’ll walk you through how s set up an individual retirement account from start to finish, covering everything from choosing the right type to making your first contribution.

Whether you’re a recent graduate just starting to earn, a mid‑career professional looking to boost your nest egg, or someone nearing retirement and wanting to catch up, the steps are surprisingly similar. The key is to understand the nuances—like the difference between a Traditional and a Roth IRA, the contribution limits, and the rules around withdrawals—so you can make an informed decision that aligns with your financial goals. Let’s dive in and demystify the process.

s set up an individual retirement account

Before you even click “Open Account,” it’s crucial to answer a few foundational questions:

- What is your current tax bracket, and do you expect it to change in retirement?

- Do you have earned income that qualifies for IRA contributions?

- Are you looking for immediate tax deductions or tax‑free growth?

These considerations will guide you toward the appropriate IRA type and help you avoid costly mistakes later on.

s set up an individual retirement account – Choosing the Right Type

There are two primary IRA families: Traditional and Roth. Both offer tax advantages, but they work in opposite ways.

- Traditional IRA: Contributions are often tax‑deductible, lowering your taxable income for the year you contribute. The money grows tax‑deferred, and you pay ordinary income tax when you withdraw it in retirement.

- Roth IRA: Contributions are made with after‑tax dollars, meaning you don’t get an immediate deduction. However, qualified withdrawals—including earnings—are tax‑free, which can be a huge benefit if you expect to be in a higher tax bracket later.

For many younger savers, a Roth IRA is attractive because the tax‑free growth can compound significantly over 30‑plus years. Conversely, high‑income earners who need an immediate tax break might lean toward a Traditional IRA.

Eligibility and Contribution Limits

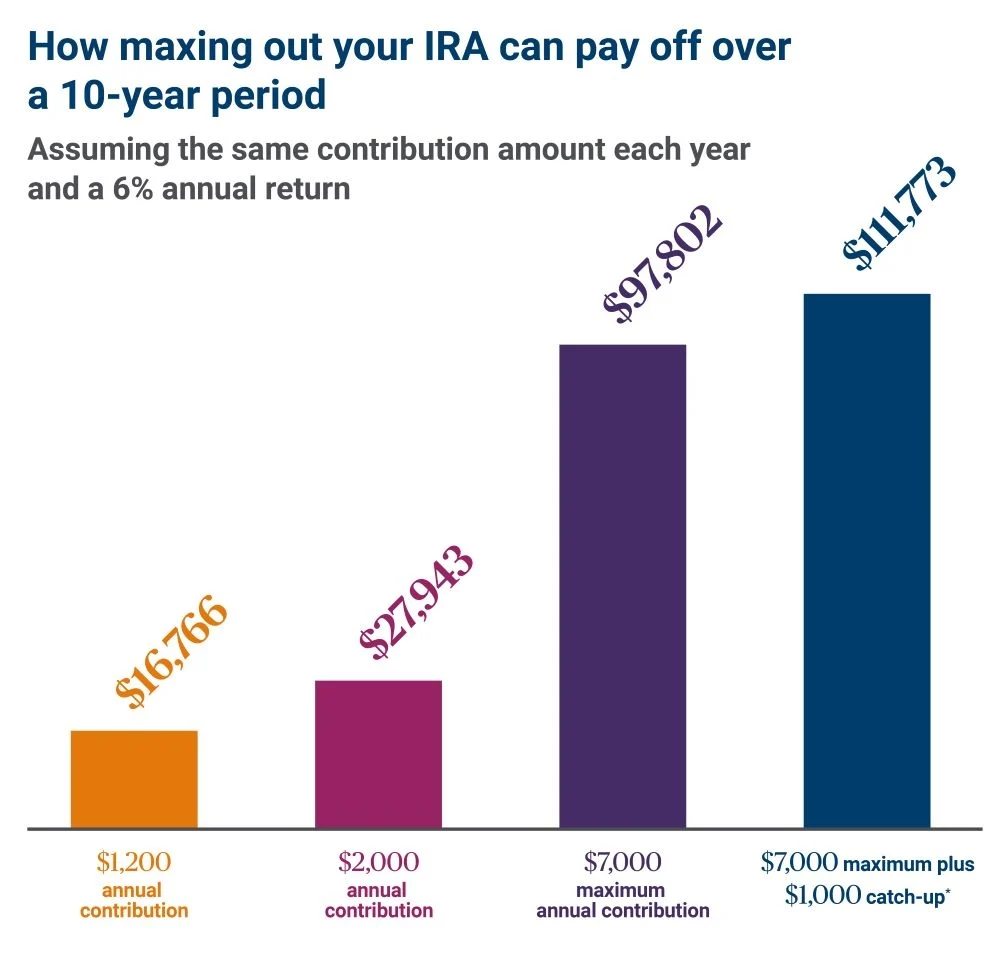

To s set up an individual retirement account, you must have earned income—wages, salary, self‑employment earnings, or alimony (if applicable). The IRS sets annual contribution limits, which for 2024 are $6,500 for individuals under 50, and $7,500 for those 50 or older (including the catch‑up contribution).

If you’re married filing jointly, you can each contribute up to the limit, effectively doubling the household’s IRA savings potential. Remember, the total contributions across all IRAs (Traditional + Roth) cannot exceed the annual limit.

Step‑by‑Step: How to s set up an individual retirement account

- Research Custodians – Not all financial institutions are created equal. Look for low fees, a wide selection of investment options, and solid customer service. Popular choices include Vanguard, Fidelity, and Charles Schwab. For example, Vanguard’s target‑date funds are a great “set it and forget it” solution for beginners; you can read more about a similar option in the Vanguard Target Retirement 2055 inv vffvx – In‑Depth Look for Future Savers article.

- Gather Personal Information – You’ll need your Social Security number, a valid ID, and banking details for funding the account. Most custodians allow electronic transfers, but you can also mail a check.

- Complete the Application – This is usually a straightforward online form. You’ll select the IRA type (Traditional or Roth), designate beneficiaries, and agree to the terms. Some platforms ask about your risk tolerance to suggest appropriate investment allocations.

- Fund the Account – You can start with a lump‑sum contribution or set up automatic monthly transfers. Automatic contributions help you stay disciplined and benefit from dollar‑cost averaging.

- Select Investments – Your IRA can hold stocks, bonds, mutual funds, ETFs, and even alternative assets in some cases. A common strategy is to allocate a portion to a diversified index fund and the rest to sector‑specific ETFs.

- Review and Adjust – Periodically check your portfolio’s performance and rebalance as needed, especially as you get closer to retirement age.

Common Pitfalls to Avoid When s set up an individual retirement account

- Missing the Contribution Deadline: The deadline for IRA contributions is typically the tax filing deadline (April 15) of the following year. Missing it means you lose that year’s tax advantage.

- Overcontributing: Exceeding the limit triggers a 6% excess contribution penalty each year the excess remains. Keep a close eye on contributions across all your IRAs.

- Ignoring Beneficiary Designations: Failing to name a beneficiary—or not updating it after life events—can cause probate delays and unwanted tax consequences for your heirs.

- Choosing High‑Fee Funds: Even a 1% annual fee can erode thousands of dollars over 30 years. Opt for low‑expense index funds whenever possible.

Tax Implications of s set up an individual retirement account

Understanding how your IRA interacts with taxes is essential for maximizing its benefits. With a Traditional IRA, you may claim a deduction on your 2024 tax return, reducing your taxable income dollar for dollar. However, withdrawals in retirement are taxed as ordinary income, and if you take distributions before age 59½, you could face a 10% early‑withdrawal penalty plus taxes.

Roth IRAs, on the other hand, provide no immediate deduction, but qualified withdrawals after age 59½ (and after the account has been open for five years) are tax‑free. This can be especially advantageous if you anticipate higher tax rates in the future—perhaps due to rising income or changes in tax policy.

If you have a high income, you might be phased out of direct Roth contributions. In that case, a “backdoor Roth” strategy—contributing to a Traditional IRA and then converting to a Roth—can be a viable workaround. Consult a tax professional before employing this technique to ensure compliance.

Integrating IRA Contributions with Other Retirement Plans

If you already participate in an employer‑sponsored plan like a 401(k), you can still s set up an individual retirement account. The contribution limits are separate, but the tax deductibility of Traditional IRA contributions may be reduced or eliminated based on your modified adjusted gross income (MAGI). Roth IRA eligibility is also subject to income thresholds.

For small business owners, there are additional options such as a Solo 401(k) or a SEP IRA, which allow higher contribution limits. The Retirement Plan Options for Small Businesses – A Complete Guide article provides a deeper dive into those alternatives.

Managing Your IRA Over Time

Opening an IRA is just the beginning. As you move through different life stages, your strategy should evolve.

- Early Career (20s‑30s): Emphasize growth—lean toward equities and target‑date funds that automatically shift toward bonds as you age.

- Mid‑Career (40s‑50s): Start to incorporate more stable assets like bonds and dividend‑paying stocks to protect gains.

- Pre‑Retirement (60s+): Focus on preserving capital, ensuring liquidity for required minimum distributions (RMDs), and planning for tax‑efficient withdrawals.

Most custodians offer tools that automatically rebalance your portfolio based on a target allocation, making it easier to stay on track without constant manual adjustments.

When to Take Distributions and How to Minimize Taxes

Traditional IRA owners must begin taking Required Minimum Distributions (RMDs) by April 1 of the year they turn 73 (as of 2024). Failing to take RMDs results in a hefty 25% penalty on the amount that should have been withdrawn. Roth IRAs, however, are not subject to RMDs during the owner’s lifetime, which can be a powerful estate planning tool.

To minimize tax impact, consider a “tax‑efficient withdrawal strategy”: pull from taxable accounts first, then tax‑deferred accounts (Traditional IRA), and finally tax‑free accounts (Roth IRA). This approach can help keep you in a lower tax bracket throughout retirement.

Finally, remember that life is unpredictable. Keep an emergency fund outside of your retirement accounts to avoid early withdrawals, which can trigger penalties and erode your long‑term savings.

Setting up an individual retirement account is a pivotal step toward financial independence. By understanding the types, eligibility rules, and tax implications, you can tailor a strategy that fits your unique situation. Start with a reputable custodian, fund your account consistently, and let compound interest do the heavy lifting. Over time, your IRA can become the cornerstone of a comfortable, worry‑free retirement.

[Finance]: Finance