Table of Contents

- Retirement Plan Options for Small Businesses: Overview of the Main Types

- SEP IRA: A Simple, Tax‑Advantaged Choice

- SIMPLE IRA: Balancing Simplicity with Employee Matching

- Traditional 401(k) & Safe Harbor 401(k): The Full‑Featured Solution

- Payroll Deduction IRA: The Ultra‑Low‑Cost Option

- How to Choose the Right Retirement Plan for Your Small Business

- 1. Assess Your Workforce Demographics

- 2. Evaluate Your Budget and Cash Flow

- 3. Consider Administrative Capacity

- 4. Look at Tax Implications

- 5. Factor in Employee Retention and Recruitment

- Implementation Tips and Common Pitfalls to Avoid

- Start with Clear Communication

- Automate Enrollment and Contributions

- Stay on Top of Compliance Calendar

- Choose the Right Investment Options

- Review Annually and Adjust as Needed

- Real‑World Examples: Small Businesses That Got It Right

- Future Trends: What’s Next for Small‑Business Retirement Plans?

- Automated Investment Platforms (Robo‑Advisors)

- ESG and Sustainable Investing Options

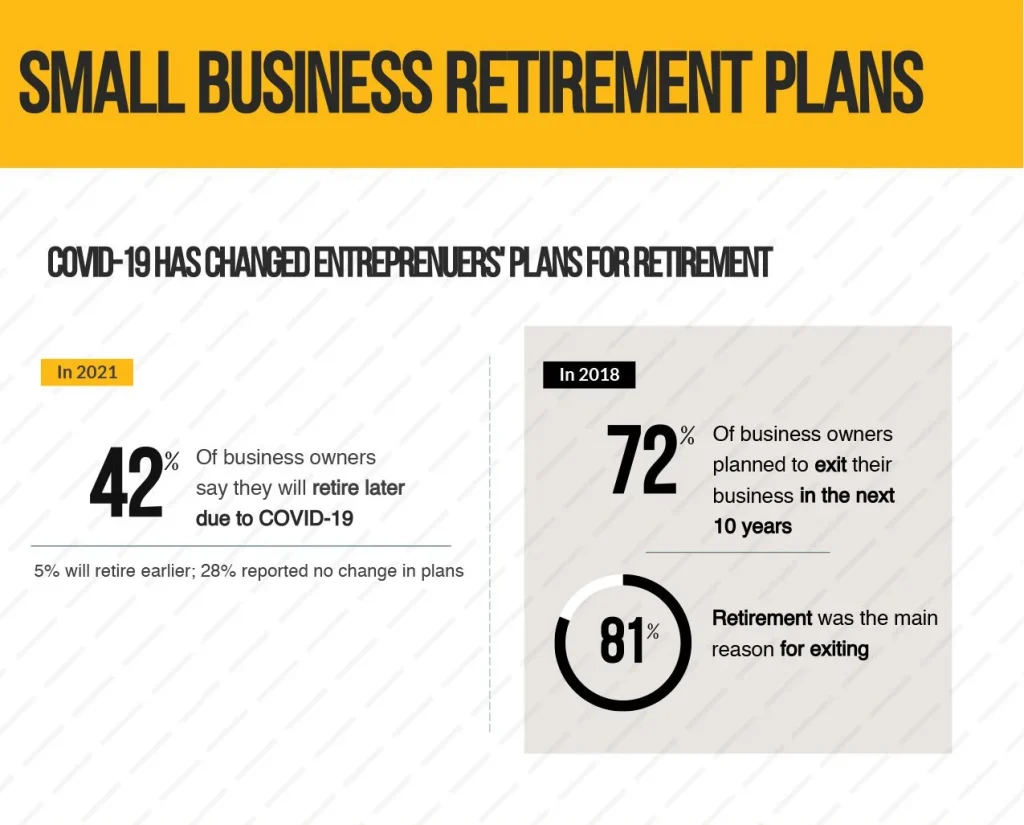

Running a small business means juggling countless priorities—cash flow, customer satisfaction, and growth strategies. Yet, one of the most rewarding—and often overlooked—investments you can make is in your employees’ retirement security. Offering a solid retirement plan not only helps attract and retain talent, but it also provides valuable tax advantages for both the employer and the employee.

When you start researching “retirement plan options for small businesses,” the sheer number of choices can feel overwhelming. From traditional 401(k) plans to more flexible SEP IRAs, each solution has its own set of rules, costs, and administrative demands. The key is to match the plan’s complexity and expense with the size of your workforce and your long‑term financial goals.

In the sections that follow, we’ll break down the most common retirement plan options for small businesses, highlight the pros and cons of each, and share practical tips to keep compliance headaches at bay. By the end, you’ll have a clear roadmap to choose the right plan and start building a more secure future for your team.

Retirement Plan Options for Small Businesses: Overview of the Main Types

Small‑business owners typically evaluate plans based on three pillars: cost, ease of administration, and employee appeal. Below is a quick snapshot of the most popular options.

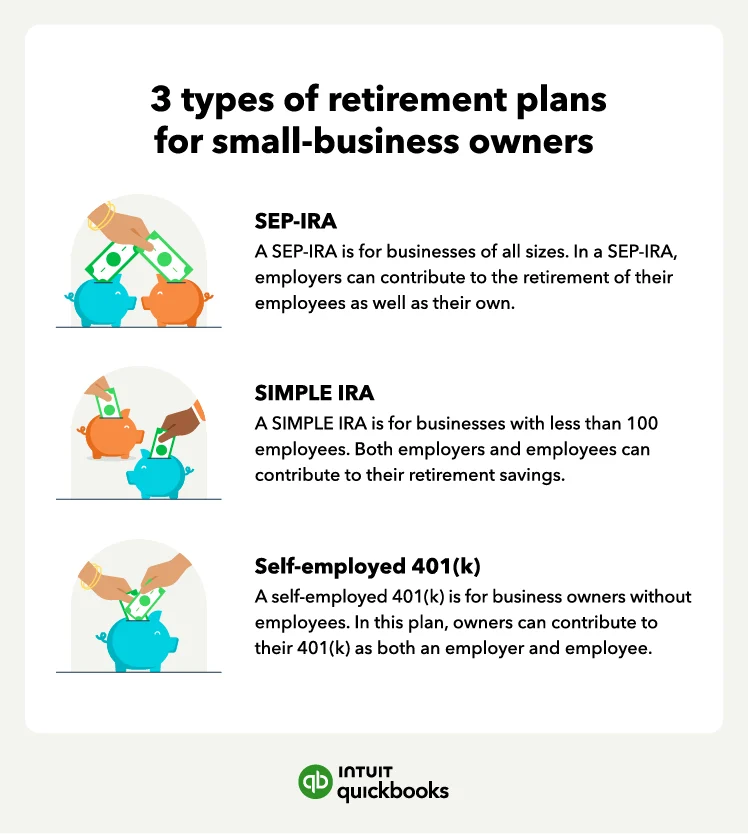

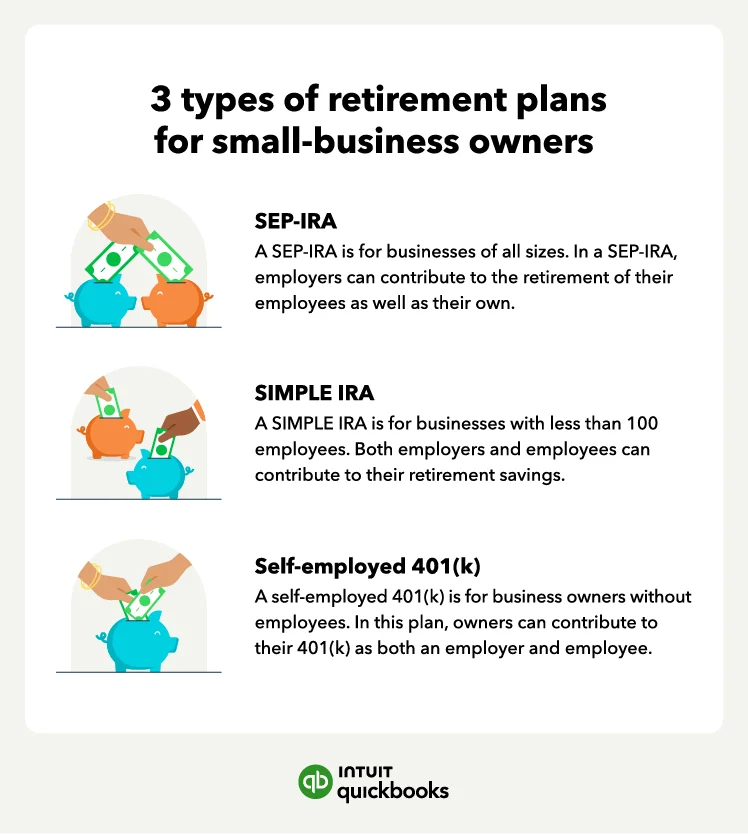

- SEP IRA (Simplified Employee Pension) – Ideal for owners who want a low‑maintenance, tax‑deductible contribution method.

- SIMPLE IRA (Savings Incentive Match Plan for Employees) – A step up from SEP with mandatory employer contributions, but still relatively simple.

- Traditional 401(k) and Safe Harbor 401(k) – More robust, allowing higher contribution limits and optional matching, but with greater administrative responsibilities.

- Payroll Deduction Plans (e.g., Payroll Deduction IRA) – The simplest form, where contributions are made directly from employee paychecks.

Each of these options can serve different business models, from solo‑owner ventures to companies with ten or twenty employees. Let’s dive deeper into the specifics.

SEP IRA: A Simple, Tax‑Advantaged Choice

The SEP IRA is often the first stop for entrepreneurs who want a straightforward, tax‑efficient way to save for retirement. Contributions are made solely by the employer, up to 25% of an employee’s compensation or $66,000 (for 2023), whichever is lower. There’s no requirement to match contributions for each employee, making it a flexible tool for businesses with fluctuating cash flow.

Key Benefits

- Low set‑up and administrative costs – often just a few minutes of paperwork.

- High contribution limits, allowing owners to shelter a significant portion of their income.

- Tax‑deductible contributions reduce the business’s taxable income.

Things to Watch

- All eligible employees must receive the same percentage of compensation as a contribution.

- No employee “catch‑up” contributions for those over 50.

- Plan documents must be filed with the IRS (Form 5305‑SEP), but no annual filing is required.

For a deeper look at how a specific fund can fit inside a SEP structure, check out our Vanguard Target Retirement 2035 Fund VTTHX – In‑Depth Review & Guide. It provides insight into investment choices that work well for SEP accounts.

SIMPLE IRA: Balancing Simplicity with Employee Matching

If you want to go a step further than a SEP IRA and offer employee matching, the SIMPLE IRA is a solid middle ground. It allows employees to contribute up to $15,500 (2023 limit) with an additional $3,500 catch‑up contribution for those 50 and older. Employers must either match employee contributions dollar‑for‑dollar up to 3% of compensation or make a flat 2% nonelective contribution for all eligible employees.

Advantages

- Lower administrative burden than a full 401(k) – no annual filing (Form 5500) required.

- Employer contributions are tax‑deductible.

- Employees can still benefit from tax‑deferred growth.

Potential Drawbacks

- Contribution limits are lower than 401(k) plans.

- Mandatory employer contributions increase costs, even if cash flow is tight.

- Early withdrawal penalties are steeper—25% if taken before age 59½ and within the first two years of participation.

Traditional 401(k) & Safe Harbor 401(k): The Full‑Featured Solution

When a small business is ready to compete with larger firms for talent, a traditional 401(k) or Safe Harbor 401(k) can be a game‑changer. These plans support higher contribution limits (up to $22,500 in 2023, plus $7,500 catch‑up) and allow for employer matching, profit‑sharing, or both. The Safe Harbor variant eliminates the need for annual nondiscrimination testing, as long as the employer meets specific matching or nonelective contribution requirements.

Why Choose a 401(k)?

- Highly attractive to employees, especially younger talent who value flexible savings options.

- Potential for Roth contributions, giving employees tax‑free growth on qualified withdrawals.

- Employer can claim a tax credit for plan setup costs (up to $5,000) if the plan is new.

Considerations

- Higher administrative fees and the need for a third‑party provider or recordkeeper.

- Annual filing requirements (Form 5500‑E) and nondiscrimination testing unless you opt for Safe Harbor.

- More complex compliance landscape—mistakes can lead to penalties.

If you’re curious about how a target‑date fund might sit inside a 401(k) offering, the Vanguard Target Retirement 2035 Trust Select – In‑Depth Look provides a thorough overview of fund performance and suitability for small‑business plans.

Payroll Deduction IRA: The Ultra‑Low‑Cost Option

For the smallest of operations—think solo entrepreneurs or businesses with fewer than five employees—a payroll deduction IRA can be the easiest route. Employees elect to have a portion of their paycheck deposited directly into a traditional or Roth IRA, with the employer simply facilitating the deduction.

Pros

- Virtually no administrative cost; the employer just needs to set up a payroll deduction.

- Employees retain control over investment choices.

- No employer contributions required, keeping overhead minimal.

Cons

- Contribution limits are lower than any employer‑sponsored plan (currently $6,500, plus $1,000 catch‑up).

- Lack of employer match may reduce perceived benefit among employees.

How to Choose the Right Retirement Plan for Your Small Business

Deciding which plan fits your organization involves a mix of quantitative analysis and qualitative judgment. Below are five practical steps to guide the selection process.

1. Assess Your Workforce Demographics

Understanding the age range, income levels, and retirement goals of your employees helps pinpoint which plan features will resonate most. Younger staff may value a Roth option, while older employees might prioritize higher contribution limits and immediate tax deductions.

2. Evaluate Your Budget and Cash Flow

Employer contributions can be a significant expense. SEP IRAs allow flexibility—contribute only in profitable years. In contrast, a SIMPLE IRA mandates a minimum contribution each year, regardless of earnings. Map out a cash‑flow projection to see what you can sustainably afford.

3. Consider Administrative Capacity

Do you have the time or expertise to handle annual nondiscrimination testing, Form 5500 filings, and ongoing compliance? If not, a low‑maintenance option like a SEP IRA or payroll deduction IRA may be preferable. Alternatively, partnering with a third‑party administrator can offload the burden for a 401(k) plan.

4. Look at Tax Implications

Employer contributions are generally tax‑deductible, reducing your taxable income. However, the tax impact varies by plan type. For example, a Safe Harbor 401(k) can provide a predictable deduction amount, while a profit‑sharing 401(k) might fluctuate with business performance.

5. Factor in Employee Retention and Recruitment

Offering a competitive retirement plan can be a decisive factor in hiring top talent. According to a recent survey, 60% of workers consider retirement benefits a “must‑have” when evaluating job offers. If your industry faces a talent shortage, investing in a more robust plan like a 401(k) could yield long‑term recruitment savings.

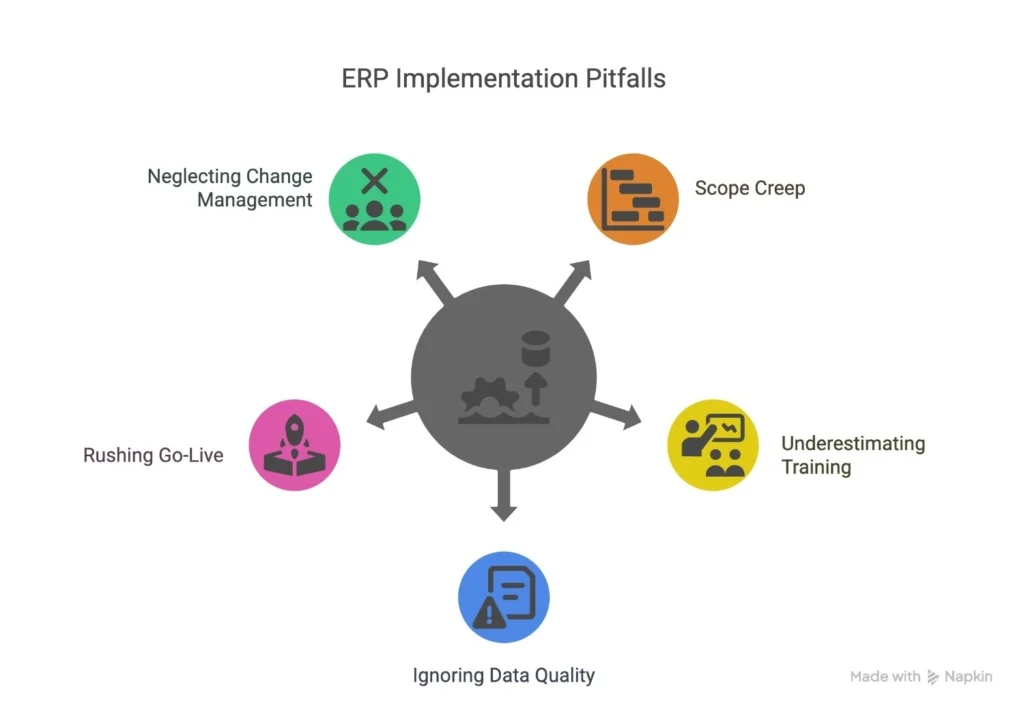

Implementation Tips and Common Pitfalls to Avoid

Even the best‑designed plan can fall flat without proper execution. Below are actionable tips to help you roll out your chosen retirement solution smoothly.

Start with Clear Communication

Employees need to understand how the plan works, the benefits they’ll receive, and the steps to enroll. Host a kickoff meeting, distribute easy‑to‑read fact sheets, and consider offering a short webinar. Transparency builds trust and boosts participation rates.

Automate Enrollment and Contributions

Automatic enrollment (where legally permissible) dramatically increases participation—often from 40% to 80%+. Set default contribution rates (e.g., 3% of salary) and let employees opt out if they wish. Automation also reduces the administrative workload for you.

Stay on Top of Compliance Calendar

Mark key filing deadlines in your calendar: Form 5500 (if applicable), annual nondiscrimination testing dates, and employee notice requirements. Missing a deadline can trigger penalties and erode employee confidence.

Choose the Right Investment Options

Offer a diversified lineup—target‑date funds, index funds, and a few stable‑value options. Too many choices can overwhelm employees, while too few can limit growth potential. A balanced approach, often recommended by plan providers, works best for small firms.

Review Annually and Adjust as Needed

Business conditions change, and so do employee needs. Conduct an annual review of contribution rates, matching formulas, and investment performance. Adjustments may involve increasing the employer match, adding a Roth component, or switching providers to lower fees.

Real‑World Examples: Small Businesses That Got It Right

Seeing how peers have succeeded can provide confidence and practical ideas.

- Tech Startup “PixelPulse” – With 12 employees, they opted for a Safe Harbor 401(k) to avoid annual testing. The firm matched 4% of each employee’s salary, resulting in a 70% participation rate within the first year.

- Family‑Owned Bakery “Sweet Crust” – The owner chose a SEP IRA because cash flow varies seasonally. Contributions are made after the holiday rush, allowing the business to maximize tax deductions when profits peak.

- Consulting Firm “Insight Edge” – They implemented a SIMPLE IRA to provide a modest match while keeping administrative costs low. Employees appreciate the simplicity, and the firm enjoys predictable contribution expenses.

These stories illustrate that the “right” plan is context‑dependent. Matching the plan’s features to your specific operational realities is the secret sauce.

Future Trends: What’s Next for Small‑Business Retirement Plans?

The retirement landscape is evolving, driven by technology, regulatory changes, and shifting worker expectations. Here are two trends to watch.

Automated Investment Platforms (Robo‑Advisors)

Many providers now integrate robo‑advisor services into 401(k) and IRA platforms, offering low‑cost, algorithm‑driven portfolio management. Small businesses can benefit from these tools to provide high‑quality investment options without the expense of a human financial advisor.

ESG and Sustainable Investing Options

Employees—especially younger generations—are increasingly interested in aligning their retirement savings with environmental, social, and governance (ESG) values. Offering ESG‑focused funds can differentiate your benefits package and enhance employee engagement.

Staying ahead of these trends not only keeps your plan competitive but also signals that your business cares about the broader impact of investing.

Choosing the optimal retirement plan for your small business is a strategic decision that pays dividends—literally and figuratively. By assessing your workforce, budget, and administrative capacity, you can select a solution that fits like a glove, fosters employee loyalty, and leverages tax advantages. Remember to communicate clearly, automate where possible, and review your plan annually. With the right approach, you’ll turn retirement planning from a compliance chore into a powerful tool for growth and goodwill.