Table of Contents

- t rowe price 2020 retirement fund: An Overview

- Key Features of the t rowe price 2020 retirement fund

- Investment Philosophy and Asset Allocation

- Risk Management in the t rowe price 2020 retirement fund

- Historical Performance and Fees

- How to Enroll and What to Expect

- Comparing t rowe price 2020 retirement fund with Other Target‑Date Options

- Practical Tips for Investors Using the t rowe price 2020 retirement fund

- Stay Disciplined with Contributions

- Reassess Your Retirement Timeline

- Watch Out for Over‑Diversification

- Consider a Small Allocation to a Pure‑Bond Fund Near Retirement

When it comes to planning for a comfortable retirement, target‑date funds have become a go‑to solution for many investors who want a set‑and‑forget approach. Among the crowd of options, the t rowe price 2020 retirement fund often pops up in discussions because it blends a disciplined glide‑path with a reputation for solid risk management. Whether you’re a seasoned saver or just starting to think about your golden years, understanding what makes this fund tick can help you decide if it belongs in your portfolio.

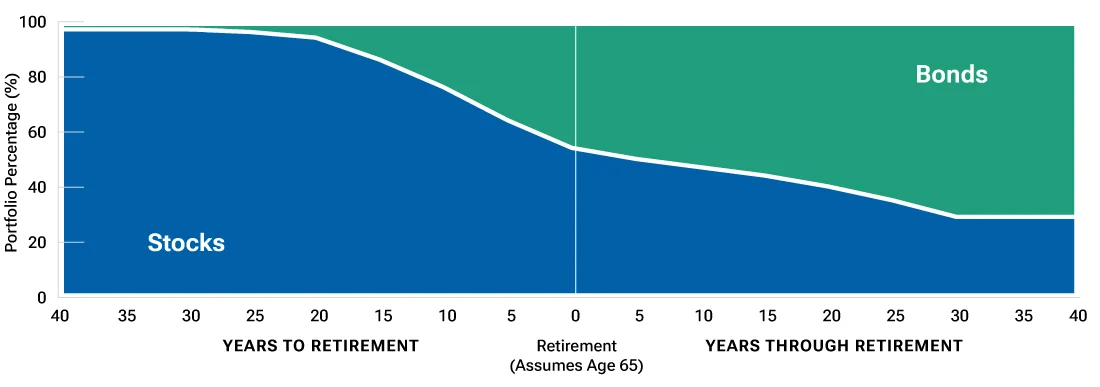

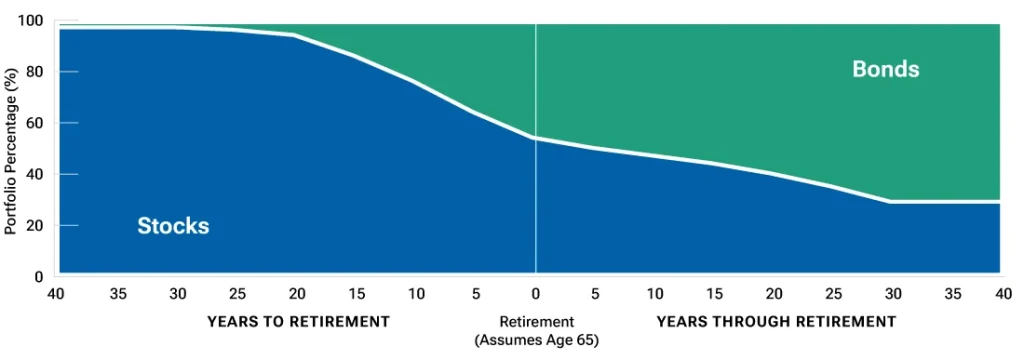

In 2020, T. Rowe Price introduced a series of retirement funds that target specific years, aiming to automatically adjust asset allocation as the target date approaches. The idea is simple: the farther you are from 2020, the more growth‑oriented the fund is; the closer you get, the more it shifts toward preservation of capital. This dynamic rebalancing is meant to reduce volatility when you need your money most—right around retirement.

But how does the t rowe price 2020 retirement fund actually perform compared to its peers? What are the fees, the underlying holdings, and the strategic nuances that set it apart? Below we dive deep into the fund’s architecture, historical results, and practical considerations for anyone thinking about adding it to their retirement plan.

t rowe price 2020 retirement fund: An Overview

The t rowe price 2020 retirement fund is a target‑date mutual fund designed for investors who plan to retire around the year 2020. Although the year has passed, the fund remains a useful benchmark for understanding how T. Rowe Price structures its retirement solutions. The fund follows a “glide‑path” that gradually reduces exposure to equities while increasing allocations to bonds and short‑term instruments as the target date nears.

Key Features of the t rowe price 2020 retirement fund

- Glide‑Path Design: Starts with roughly 80% equities and 20% fixed income, shifting to about 30% equities and 70% fixed income by 2020.

- Active Management: Unlike many index‑based target‑date funds, T. Rowe Price employs a team of analysts to select securities within each asset class.

- Low Turnover: The fund’s turnover ratio stays under 30%, indicating a relatively stable portfolio composition.

- Expense Ratio: Typically around 0.70%, which is competitive for an actively managed target‑date fund.

These characteristics make the t rowe price 2020 retirement fund appealing for investors who want professional oversight without the complexity of managing multiple individual funds themselves.

Investment Philosophy and Asset Allocation

T. Rowe Price builds its retirement funds around a core belief that diversified exposure across global markets, combined with disciplined risk control, yields better long‑term outcomes. For the 2020 fund, the asset allocation starts heavily weighted toward U.S. large‑cap equities, but also includes a modest slice of international stocks, emerging markets, and real assets.

As the fund moves closer to its target year, the allocation gradually tilts toward investment‑grade corporate bonds, U.S. Treasury securities, and short‑term cash equivalents. This shift is not a straight line; the fund’s managers adjust the glide‑path based on macroeconomic outlooks, ensuring the risk profile aligns with the anticipated retirement timeline.

Risk Management in the t rowe price 2020 retirement fund

Risk mitigation is woven into the fund’s fabric. First, the active management team conducts regular stress‑testing to gauge how the portfolio might react to market downturns. Second, the fund employs a “bottom‑up” stock selection process that seeks companies with strong balance sheets and sustainable earnings growth. Finally, the fixed‑income component is diversified across credit qualities and durations, reducing sensitivity to interest‑rate swings.

Historical Performance and Fees

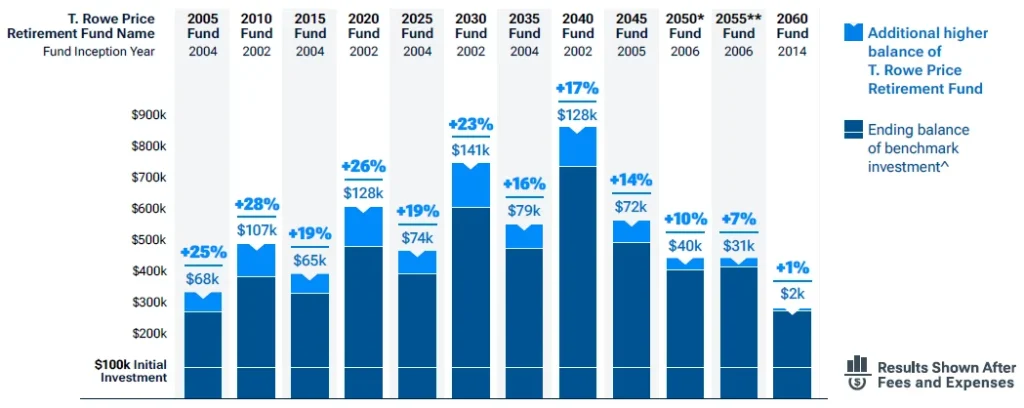

Looking back at the fund’s performance from its inception through the early 2020s, the t rowe price 2020 retirement fund delivered an average annual return of about 7.5% before fees. During the market turmoil of 2020, the fund’s equity exposure helped it recover more quickly than many pure‑bond target‑date alternatives, while its gradual shift to bonds cushioned the downside.

Fees are always a focal point for investors. At roughly 0.70% expense ratio, the fund sits comfortably below many actively managed mutual funds, though it is slightly higher than some passively managed index funds. The expense structure includes a management fee, distribution costs, and administrative expenses—all bundled into the single ratio you see on the prospectus.

How to Enroll and What to Expect

Enrolling in the t rowe price 2020 retirement fund is straightforward. Most major brokerage platforms, employer-sponsored 401(k) plans, and retirement accounts (IRAs) offer the fund as a selectable investment option. After you add it to your account, the fund automatically rebalances each quarter, aligning the portfolio with the predefined glide‑path.

Investors should anticipate a few key steps:

- Choose the fund: Locate “T. Rowe Price 2020 Retirement Fund” in your platform’s fund list.

- Allocate contributions: Decide what percentage of each paycheck or contribution will flow into the fund.

- Monitor periodically: While the fund is set‑and‑forget, an annual check‑in ensures it still matches your retirement timeline and risk tolerance.

Comparing t rowe price 2020 retirement fund with Other Target‑Date Options

To gauge whether the t rowe price 2020 retirement fund is right for you, it helps to stack it against comparable products. For instance, Vanguard’s target‑date series is known for its low‑cost, index‑driven approach. If you’re curious about a more passive alternative, take a look at the Vanguard Target Retirement 2035 Trust Select – In‑Depth Look, which offers a similar glide‑path but at a lower expense ratio.

On the other side of the spectrum, American Funds offers a more actively managed lineup, like the American Funds 2030 Target Date Retirement Fund. Compared to T. Rowe Price, American Funds tends to have a slightly higher expense ratio but may provide different sector tilts that appeal to certain investors.

When comparing, consider three primary factors:

- Cost: Lower fees can boost net returns over long horizons.

- Management Style: Active vs. passive approaches affect how the fund reacts to market changes.

- Glide‑Path Flexibility: Some providers allow you to choose a “more aggressive” or “more conservative” path within the same target year.

Practical Tips for Investors Using the t rowe price 2020 retirement fund

Stay Disciplined with Contributions

Even though the fund handles allocation, the onus is on you to keep funding it regularly. Automate contributions through your payroll or direct deposit to avoid missed savings.

Reassess Your Retirement Timeline

If your retirement plans shift—perhaps you decide to retire a few years earlier or later—consider moving to a different target‑date fund that better aligns with your new horizon. The glide‑path is calibrated to a specific year, so using the correct target date is crucial.

Watch Out for Over‑Diversification

Some investors stack multiple target‑date funds together, thinking it adds diversification. In reality, this can lead to redundant exposure and higher combined fees. One well‑chosen fund, such as the t rowe price 2020 retirement fund, often suffices when paired with a separate allocation for non‑retirement goals.

Consider a Small Allocation to a Pure‑Bond Fund Near Retirement

As you enter the final five years before retirement, you might want to shift a modest portion of your portfolio into a short‑term bond fund or a money‑market vehicle to lock in liquidity. This extra step can smooth the transition from the fund’s built‑in bond allocation to cash needed for living expenses.

Overall, the t rowe price 2020 retirement fund delivers a balanced blend of active management, a clear glide‑path, and a reasonable fee structure. While the fund’s name references a past target year, its design principles continue to influence newer T. Rowe Price target‑date offerings, making it a valuable case study for anyone evaluating retirement investments.

By understanding the fund’s strategy, performance history, and how it fits within the broader landscape of target‑date options, you can make a more informed decision about whether it should anchor your retirement savings plan. As always, pair this research with your personal risk tolerance and financial goals, and consider consulting a fiduciary advisor if you need tailored guidance.