Table of Contents

- Overview of the Teacher Retirement System of New York

- Key Features of the Teacher Retirement System of New York

- Eligibility and Service Credits

- How Benefits Are Calculated

- Cost‑Sharing and Contribution Rates

- Retirement Income Planning Tips

- 1. Consider Supplemental Savings

- 2. Explore Annuities and Target‑Date Funds

- 3. Maximize Survivor Benefits

- 4. Keep an Eye on Cost‑of‑Living Adjustments (COLA)

- Special Situations and Exceptions

- How to Apply for Retirement

- Tax Implications and Financial Planning

- Future Outlook and System Sustainability

- Common Questions Answered

- Can I retire before reaching the minimum age?

- What happens if I change jobs within the education sector?

- Is there a maximum pension amount?

- Can I receive a lump‑sum payout?

Teaching is more than a profession; it’s a lifelong commitment to shaping future generations. While the rewards are often intangible, New York State offers a concrete safety net that helps educators transition from the classroom to a comfortable retirement. This safety net is the teacher retirement system of New York, a pension plan that has evolved over decades to meet the changing needs of its members.

Understanding how this system works can feel like navigating a maze of statutes, contribution rates, and benefit calculations. Yet, the clearer you are about the mechanics, the better you can make strategic decisions—whether you’re a brand‑new teacher, a veteran educator approaching the eligibility age, or someone planning a second career after leaving the classroom.

In this article we’ll break down the essential components of the teacher retirement system of New York, walk through eligibility rules, explore benefit formulas, and share practical tips for maximizing your retirement income. Along the way, we’ll sprinkle in a few resources—like a guide on retirement accounts for small business owners—that can broaden your financial toolkit.

Overview of the Teacher Retirement System of New York

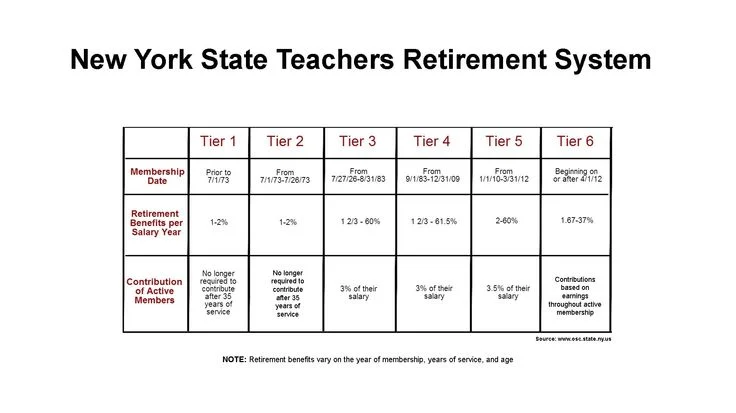

The teacher retirement system of New York, formally known as the New York State Teachers’ Retirement System (NYSTRS), is one of the nation’s largest public‑pension plans. It serves over 300,000 active members, retirees, and beneficiaries, covering teachers from public schools, charter schools, and certain private institutions that participate in the state system.

At its core, the system operates on a defined‑benefit model. That means you and your employer contribute a set percentage of your salary into a pooled fund, and when you retire you receive a predetermined monthly payment based on a formula that includes your years of service, final average salary, and a benefit multiplier.

Key Features of the Teacher Retirement System of New York

- Defined Benefit Structure: Predictable monthly income for life, adjusted for cost‑of‑living increases.

- Cost‑Sharing: Both teachers and school districts contribute; the exact rates vary by employee class and salary tier.

- Portability: If you leave teaching for another state or a private sector job, you can transfer or cash out your accrued benefits under specific conditions.

- Survivor Benefits: Options to provide a spouse or former spouse with a portion of your pension after your death.

- Health Insurance: Eligible retirees may qualify for the New York State and Local Retirement System (NYSLRS) health plan, often at reduced premiums.

Eligibility and Service Credits

To qualify for a pension from the teacher retirement system of New York, you need to meet both age and service‑credit requirements. The system recognizes two primary retirement pathways:

- Normal Retirement: Minimum age 62 with at least 10 years of credited service, or age 55 with 30 years of service.

- Early Retirement: Available for teachers who have completed 20 years of service and are at least 55, but it comes with a reduction factor applied to the benefit.

Service credits are earned each year you work a full teaching day, regardless of part‑time status, as long as you meet the minimum attendance and instructional hours set by the Department of Education. A “credited year” essentially equals one year of service toward your pension.

How Benefits Are Calculated

The benefit formula for the teacher retirement system of New York is straightforward yet powerful:

Annual Pension = Years of Service × Final Average Salary × Benefit Multiplier

Let’s unpack each component:

- Years of Service: The total number of credited years, including any prior service from other NY state public‑employee plans that are transferrable.

- Final Average Salary (FAS): Typically the average of the highest three consecutive years of base salary earned within the last ten years of service. This figure smooths out salary spikes and ensures a stable base for calculation.

- Benefit Multiplier: For most teachers, the multiplier is 2% per year of service. So a teacher with 30 years of service would receive 30 × 2% = 60% of their FAS as an annual pension.

Example: A teacher with 30 years of service, a final average salary of $85,000, and the standard 2% multiplier would receive an annual pension of $85,000 × 0.60 = $51,000, or about $4,250 per month before taxes and any survivor adjustments.

Cost‑Sharing and Contribution Rates

Both employees and employers contribute a percentage of the teacher’s salary to fund the system. As of 2024, the employee contribution rate sits around 9% of gross salary, while the employer (school district) contributes roughly 12%. These rates are periodically adjusted by the Board of Trustees based on actuarial valuations, investment performance, and demographic trends.

Contributions are automatically deducted from payroll, making the process seamless for teachers. Importantly, the contributions are pre‑tax, reducing your current taxable income while building retirement assets.

Retirement Income Planning Tips

Even though the teacher retirement system of New York guarantees a base pension, relying solely on that income can be risky. Here are a few practical strategies to supplement your retirement cash flow:

1. Consider Supplemental Savings

Many educators boost their retirement security with personal savings vehicles such as IRAs, 401(k)s (if you have a second job), or the New York State’s 457(b) deferred compensation plan. For a deeper dive on how different accounts work, check out Understanding Retirement Accounts for Small Business Owners. Even modest contributions can compound significantly over a 30‑year career.

2. Explore Annuities and Target‑Date Funds

Target‑date funds, like the Vanguard Target Retirement 2040 Fund Fact Sheet – In‑Depth Look, offer a hands‑off approach that automatically rebalances as you near retirement. Pairing a portion of your savings with an annuity can also provide a guaranteed income stream that complements your pension.

3. Maximize Survivor Benefits

If you’re married, electing a survivor benefit can ensure your spouse continues receiving a portion of your pension after your death. The trade‑off is a slight reduction in your own monthly benefit, but many find the peace of mind worth it.

4. Keep an Eye on Cost‑of‑Living Adjustments (COLA)

The teacher retirement system of New York applies annual COLA increases to pensions based on inflation and wage growth. Understanding the formula helps you anticipate future purchasing power and plan accordingly.

Special Situations and Exceptions

While the standard rules cover most educators, there are a few scenarios that merit special attention:

- Military Service: Service members who leave teaching to serve in the armed forces may receive credit for up to five years of military service toward their pension.

- Leave of Absence: A leave for health, family, or personal reasons does not necessarily break your service credit, provided you meet the department’s eligibility criteria.

- Transition to Another Public‑Employee Plan: If you move to a different public‑sector job in New York (e.g., a municipal employee), you can transfer your accrued credits to the NYSLRS, preserving your pension rights.

How to Apply for Retirement

The application process is intentionally straightforward. Here’s a step‑by‑step guide:

- Log in to the NYSTRS online portal at nystri.org and verify your service record.

- Complete the “Application for Retirement” form, selecting your desired retirement date and survivor options.

- Submit required documentation, such as proof of age and a signed oath.

- Review the benefit estimate provided by the system; you can request a “Benefit Projection” if you want to model different scenarios.

- Finalize your application at least 90 days before your intended retirement date to allow processing time.

Once approved, you’ll receive a pension award letter outlining the exact monthly amount, start date, and any applicable tax withholdings.

Tax Implications and Financial Planning

Pensions from the teacher retirement system of New York are subject to federal income tax, but New York State provides a partial exemption for qualified public‑employee pensions. As of the latest tax year, the first $20,000 of pension income is exempt for single filers and $30,000 for married couples filing jointly.

Because the pension is taxed as ordinary income, it’s wise to coordinate with a tax professional to optimize withholding and explore deductions. For a holistic view of retirement income, the Definitive Guide to Retirement Income PDF – Your Complete Roadmap offers a comprehensive framework that includes Social Security, investment income, and other streams.

Future Outlook and System Sustainability

Like many public‑pension plans, the teacher retirement system of New York faces demographic pressures—an aging workforce and longer life expectancies increase the payout horizon. The Board of Trustees conducts regular actuarial reviews to adjust contribution rates, benefit formulas, and COLA calculations, ensuring the fund remains solvent.

Recent reforms have introduced options for phased retirement, allowing teachers to reduce hours while still earning a partial pension. This flexibility can ease the transition to full retirement and help retain experienced educators on a part‑time basis.

Common Questions Answered

Can I retire before reaching the minimum age?

Early retirement is possible after 20 years of service and age 55, but a reduction factor will lower your monthly benefit. The exact factor depends on how many years you retire early.

What happens if I change jobs within the education sector?

Switching between public schools, charter schools, or other participating institutions does not reset your service credits. Your accrued benefits stay with you, and you continue contributing at the same rates.

Is there a maximum pension amount?

Yes, there is a cap on the annual pension based on a percentage of your final average salary, set by state law. This cap is periodically updated to reflect inflation and budget considerations.

Can I receive a lump‑sum payout?

The system generally does not offer lump‑sum withdrawals of accrued benefits, except in rare circumstances such as death or termination with no vested benefits. Instead, benefits are paid as a monthly annuity.

Understanding the nuances of the teacher retirement system of New York empowers you to make informed decisions, plan for a comfortable future, and enjoy the peace of mind that comes from a reliable public‑pension foundation. Whether you’re just starting your teaching career or counting down the final semesters, the strategies and insights outlined here can help you maximize the value of your hard‑earned benefits.