Table of Contents

- nuveen s&p 500 index fund retirement: Core Features and Benefits

- nuveen s&p 500 index fund retirement: How It Fits Into a Diversified Portfolio

- Comparing Nuveen’s S&P 500 Fund to Other Popular Index Options

- Understanding Fees and Their Impact Over Time

- nuveen s&p 500 index fund retirement: Practical Tips for Reducing Costs

- Tax Considerations for the Nuveen S&P 500 Index Fund Retirement Version

- Setting Up and Managing the Nuveen S&P 500 Index Fund Retirement in Your Plan

- Risks and Considerations Specific to the Nuveen S&P 500 Index Fund Retirement

- Long‑Term Outlook: Is the Nuveen S&P 500 Index Fund Retirement a Good Fit for You?

When you start thinking about retirement, the sheer number of investment choices can feel overwhelming. Stocks, bonds, target‑date funds, IRAs, 401(k)s—each option comes with its own set of rules, fees, and risk profiles. Among these, a simple, low‑cost index fund can be a solid cornerstone, especially if you value transparency and long‑term growth. That’s where the Nuveen S&P 500 Index Fund retirement version steps onto the stage.

Designed specifically for retirement accounts, this fund tracks the performance of the S&P 500, offering exposure to 500 of the largest U.S. companies. It aims to deliver the same return as the benchmark, minus the tiny tracking error and a modest expense ratio. For many investors, especially those who prefer a “set it and forget it” approach, the Nuveen S&P 500 Index Fund retirement offering can serve as a reliable growth engine within a broader retirement portfolio.

In this article we’ll break down what makes the Nuveen S&P 500 Index Fund retirement option unique, how it stacks up against competitors, and practical tips for weaving it into a retirement plan that aligns with your goals and risk tolerance.

nuveen s&p 500 index fund retirement: Core Features and Benefits

The Nuveen S&P 500 Index Fund retirement version is built around a straightforward mission: mirror the S&P 500’s total return as closely as possible while keeping costs low. Below are the key attributes that investors should know:

- Benchmark Tracking: The fund seeks to replicate the performance of the S&P 500 Index, which represents roughly 80% of the U.S. equity market’s total market capitalization.

- Expense Ratio: At around 0.05% for retirement accounts, the fee structure is competitive, especially when compared to many actively managed equity funds.

- Tax Efficiency: Because the fund’s turnover is low, capital gains distributions are minimal, a crucial factor for tax‑advantaged retirement accounts.

- Liquidity: As an open‑ended mutual fund, you can buy or sell shares at the end of any trading day at the net asset value (NAV), providing flexibility for retirement withdrawals.

- Eligibility: The fund is available within traditional IRAs, Roth IRAs, 401(k) plans, and other qualified retirement plans, making it a versatile option for many savers.

nuveen s&p 500 index fund retirement: How It Fits Into a Diversified Portfolio

No single fund should dominate an entire retirement plan. While the Nuveen S&P 500 Index Fund retirement version offers solid growth potential, it’s essential to blend it with other asset classes to manage risk. Here’s a quick framework:

- Core Equity Portion: Allocate 30‑50% of your equity exposure to the Nuveen S&P 500 Index Fund retirement version. This provides broad market coverage and aligns with historical long‑term returns.

- International Diversification: Complement the U.S. focus with a global or emerging‑markets index fund to capture growth outside the United States.

- Fixed‑Income Layer: Add bond funds or Treasury securities to dampen volatility, especially as you near retirement age.

- Alternative Assets: Consider REITs, real assets, or even a small allocation to commodities for further diversification.

By treating the Nuveen S&P 500 Index Fund retirement version as the “core” equity holding, you can maintain a simple yet robust structure that’s easy to manage and rebalance over time.

Comparing Nuveen’s S&P 500 Fund to Other Popular Index Options

When you hear “S&P 500 index fund,” the first name that comes to mind is often Vanguard’s VFIAX or the SPDR S&P 500 ETF (SPY). So why consider Nuveen’s version for retirement?

- Expense Ratio Differences: Vanguard’s investor‑share class of its S&P 500 fund sits at 0.04%, while Nuveen’s retirement share is 0.05%. The gap is minimal, but Nuveen may be the only option offered within certain employer‑sponsored plans.

- Plan Compatibility: Some 401(k) providers have a limited set of fund families. If your plan features Nuveen’s lineup, you might not have access to Vanguard or other providers without a rollover.

- Minimum Investment: Nuveen often sets a lower minimum initial investment for retirement accounts, making it more accessible for new savers.

- Management Philosophy: While all these funds are passively managed, Nuveen emphasizes a “full replication” strategy, holding every constituent stock, which can slightly reduce tracking error compared to sampling methods.

Ultimately, the best choice depends on the specific constraints of your retirement plan, fee structures, and personal preference for fund families.

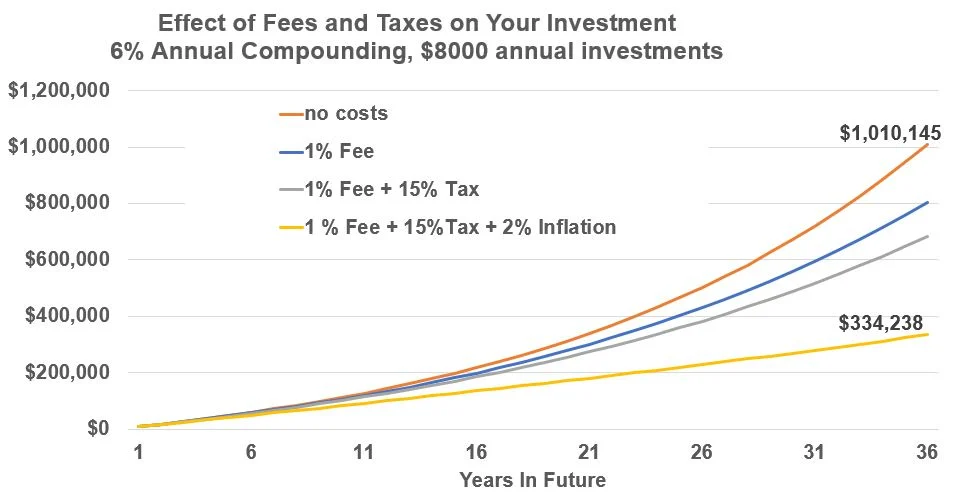

Understanding Fees and Their Impact Over Time

Even a seemingly tiny expense ratio can compound into a significant amount over a 30‑year retirement horizon. Let’s illustrate with a quick example:

- Initial investment: $10,000

- Average annual return (pre‑fees): 7%

- Nuveen S&P 500 Index Fund retirement expense ratio: 0.05%

- Competing fund expense ratio: 0.10%

After 30 years, the Nuveen fund would grow to roughly $76,122, while the higher‑fee fund would sit around $73,210. That $2,912 difference is purely the result of fee differentials—a reminder that paying attention to expenses matters.

nuveen s&p 500 index fund retirement: Practical Tips for Reducing Costs

Here are a few actionable strategies to keep your retirement costs low while using the Nuveen S&P 500 Index Fund retirement version:

- Use Automatic Rebalancing: Many retirement platforms allow you to set target percentages. Automated rebalancing avoids the need for frequent trades that could incur additional fees.

- Consolidate Accounts: If you have multiple IRAs, consider consolidating them to reduce administrative fees and simplify management.

- Stay Within the Same Fund Family: Switching between fund families may trigger transaction fees or tax implications even within a retirement account.

Tax Considerations for the Nuveen S&P 500 Index Fund Retirement Version

Because this fund is designed for tax‑advantaged retirement accounts, the usual capital gains and dividend taxes you’d face in a taxable brokerage are largely postponed. However, there are still nuances worth noting:

- Roth vs. Traditional: In a Roth IRA, qualified withdrawals are tax‑free, meaning the growth you earn in the Nuveen S&P 500 Index Fund retirement version stays completely untaxed. In a traditional IRA, withdrawals are taxed as ordinary income.

- Required Minimum Distributions (RMDs): Starting at age 73 (as of 2024), you’ll need to take RMDs from traditional IRAs and 401(k)s. Planning ahead can help you avoid large taxable bumps.

- Dividend Income: Even though dividends are reinvested in the fund, they’re still subject to ordinary income tax if withdrawn from a traditional retirement account.

If you’re curious about how other retirement income streams compare, you might enjoy reading Can Life Insurance Be Used for Retirement? A Comprehensive Look, which explores alternative vehicles for supplementing retirement cash flow.

Setting Up and Managing the Nuveen S&P 500 Index Fund Retirement in Your Plan

Getting started is usually straightforward:

- Check Eligibility: Verify that your employer’s 401(k) or your IRA custodian offers the Nuveen S&P 500 Index Fund retirement version.

- Open or Contribute: If you’re opening a new account, you’ll need to complete the standard paperwork. Existing account holders can simply allocate a portion of their contributions to the fund.

- Set Allocation: Decide what percentage of your portfolio will be devoted to the Nuveen S&P 500 Index Fund retirement version. Many financial advisors recommend a “core‑satellite” approach where the index fund acts as the core.

- Monitor and Rebalance: Review your allocation annually or after major life events. Most platforms let you set target percentages and automatically rebalance.

For small business owners looking to create retirement accounts for themselves and employees, the article Understanding Retirement Accounts for Small Business Owners provides a solid roadmap that often includes similar index‑fund options.

Risks and Considerations Specific to the Nuveen S&P 500 Index Fund Retirement

Even a low‑cost index fund isn’t without risk. Here’s what to keep in mind:

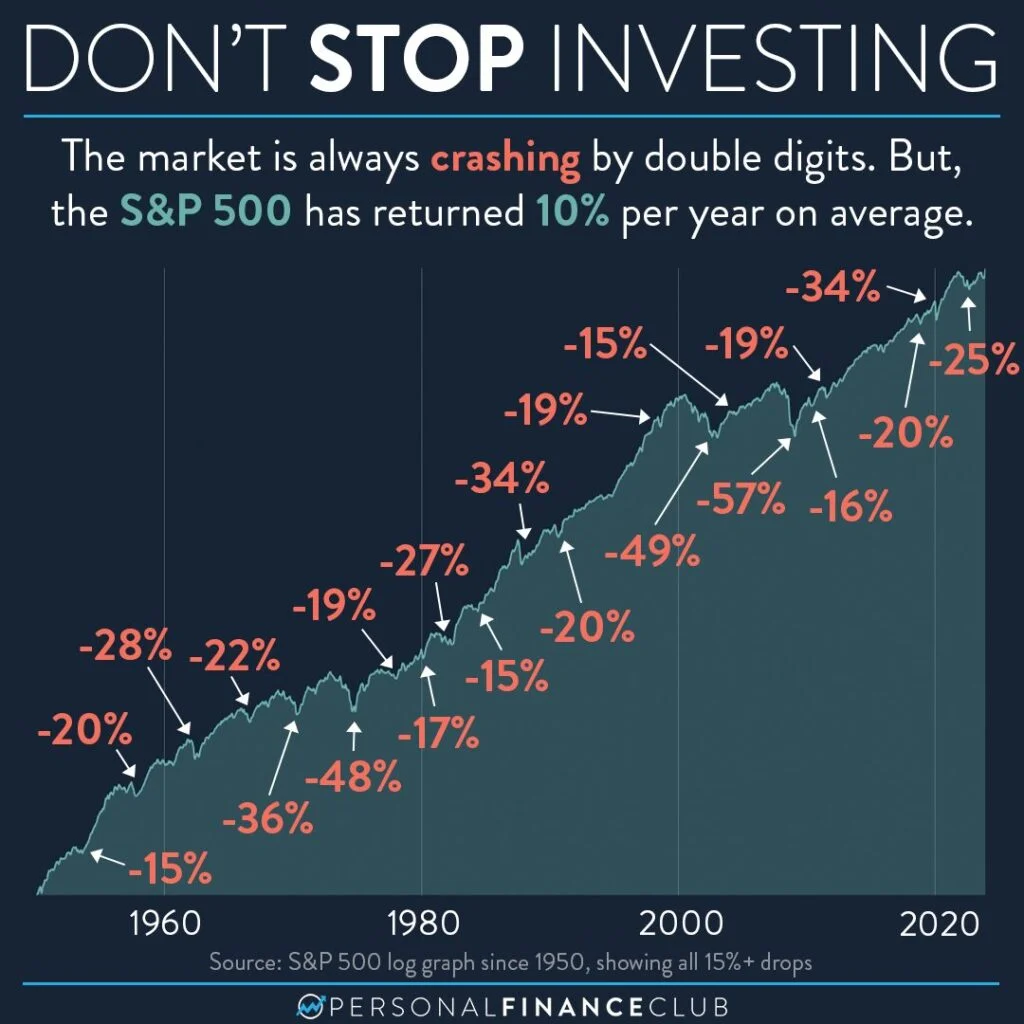

- Market Volatility: The S&P 500 can swing dramatically in short periods. A 20% decline in a single year isn’t unheard of.

- Concentration Risk: While diversified across 500 companies, the index is still heavily weighted toward large‑cap, U.S. firms. A downturn in the U.S. market could affect the entire fund.

- Interest‑Rate Sensitivity: Though primarily an equity fund, higher rates can indirectly influence stock valuations, especially for growth‑oriented sectors.

If you’re seeking a broader view of retirement benefits beyond the traditional 401(k), consider checking out the ssa potential private retirement benefit information – A Complete Guide for additional insight.

Long‑Term Outlook: Is the Nuveen S&P 500 Index Fund Retirement a Good Fit for You?

Historically, the S&P 500 has delivered an average annual return of about 9‑10% before inflation. While past performance isn’t a guarantee of future results, the long‑term upward trend suggests that a well‑managed, low‑cost index fund can be a powerful growth engine for retirement savings.

Key factors to evaluate include:

- Time Horizon: If you have 20+ years until retirement, the growth potential of the Nuveen S&P 500 Index Fund retirement version aligns well with a long‑term perspective.

- Risk Tolerance: Investors comfortable with market fluctuations may allocate a higher percentage to this fund.

- Overall Portfolio Structure: Use the fund as a core equity piece, balanced with bonds, international exposure, and perhaps a target‑date fund for the later years.

By staying disciplined, keeping expenses low, and periodically rebalancing, you can let the power of compounding work in your favor—turning modest contributions into a sizable retirement nest egg.

In the end, the Nuveen S&P 500 Index Fund retirement offering isn’t a magic bullet, but it’s a reliable, low‑cost building block that fits neatly into many retirement strategies. Pair it with thoughtful asset allocation, regular contributions, and a clear understanding of your retirement goals, and you’ll be well on your way to a financially secure future.