Table of Contents

- ssa potential private retirement benefit information: What It Really Means

- Why ssa potential private retirement benefit information Matters for Every Saver

- Key Components of ssa Potential Private Retirement Benefit Information

- 1. Your SSA Benefit Estimate

- 2. Private Retirement Accounts Overview

- 3. Timing and Coordination

- How to Gather Accurate ssa Potential Private Retirement Benefit Information

- Step‑by‑Step Checklist

- Strategies to Maximize Your ssa Potential Private Retirement Benefit Information

- 1. Delay SSA Benefits When Possible

- 2. Use Tax‑Efficient Withdrawal Sequencing

- 3. Consider a Hybrid Annuity

- 4. Leverage Employer Matching Contributions

- Common Pitfalls and How to Avoid Them

- Overestimating Future SSA Benefits

- Neglecting Health Care Costs

- Ignoring Required Minimum Distributions (RMDs)

- Tools and Resources to Keep Your ssa Potential Private Retirement Benefit Information Up‑to‑Date

- Recommended Resources

- Putting It All Together: A Sample Roadmap

Planning for retirement can feel like solving a massive puzzle—especially when you try to blend what the Social Security Administration offers with the myriad of private options out there. The term “ssa potential private retirement benefit information” might sound like a mouthful, but it’s really just a shorthand for understanding how public benefits and private savings can work together to give you a comfortable post‑work life.

In this article we’ll break down the basics, walk through the key steps you should take, and share practical tips to help you make the most of every dollar you put aside. Whether you’re a fresh graduate, a mid‑career professional, or approaching the golden years, the insights here will help you see the big picture and act on the details that matter most.

Before we dive into the nitty‑gritty, remember that every retirement plan is unique. The strategies that work for a small‑business owner might differ from those best suited for a teacher in New York. Feel free to explore related reads such as Teacher Retirement System of New York – A Complete Guide for sector‑specific guidance.

ssa potential private retirement benefit information: What It Really Means

The phrase “ssa potential private retirement benefit information” combines two major pillars of retirement security: the Social Security Administration (SSA) and private retirement vehicles like IRAs, 401(k)s, and annuities. Understanding this blend is crucial because relying solely on one source can leave gaps, while a well‑balanced approach can smooth out income volatility and protect against unexpected life events.

At its core, the SSA provides a baseline of guaranteed income based on your lifetime earnings. However, the amount you receive—often referred to as “SSA benefits”—might only cover a portion of your expected expenses. That’s where private retirement benefits step in, offering flexibility, tax advantages, and the potential for higher returns.

Why ssa potential private retirement benefit information Matters for Every Saver

- It helps you set realistic expectations about future cash flow.

- It highlights the interaction between taxable, tax‑deferred, and tax‑free accounts.

- It guides you in timing when to claim Social Security versus when to draw from private accounts.

Getting a clear picture of this information early can prevent costly mistakes—like claiming SSA benefits too soon or under‑investing in private accounts. The sooner you align your personal goals with the data, the smoother the transition to retirement will be.

Key Components of ssa Potential Private Retirement Benefit Information

Let’s break down the main elements you should examine when gathering your ssa potential private retirement benefit information.

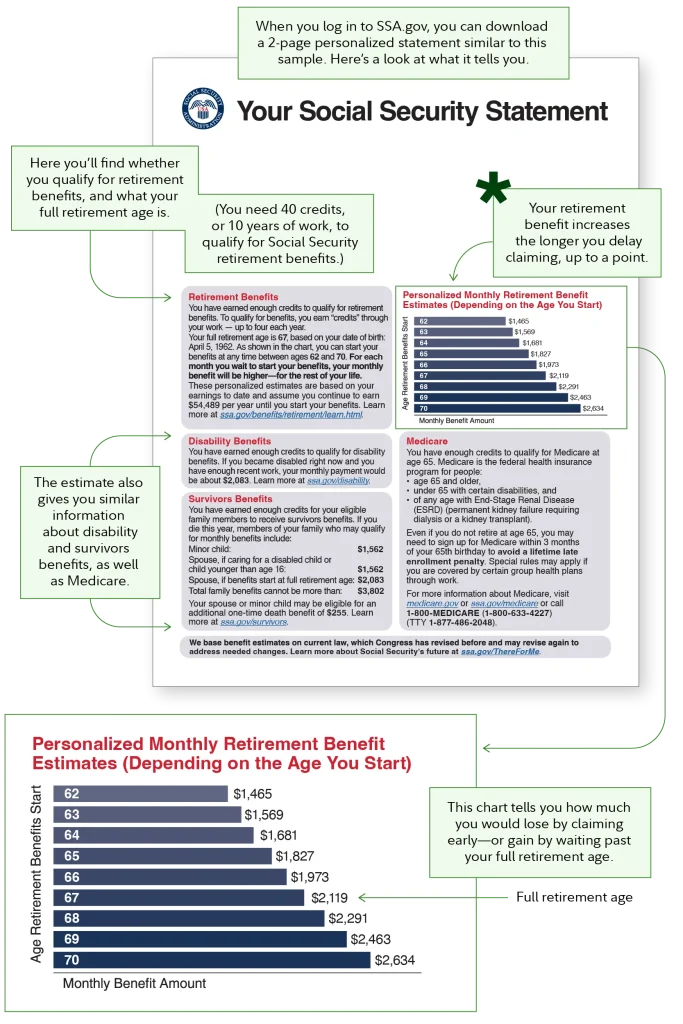

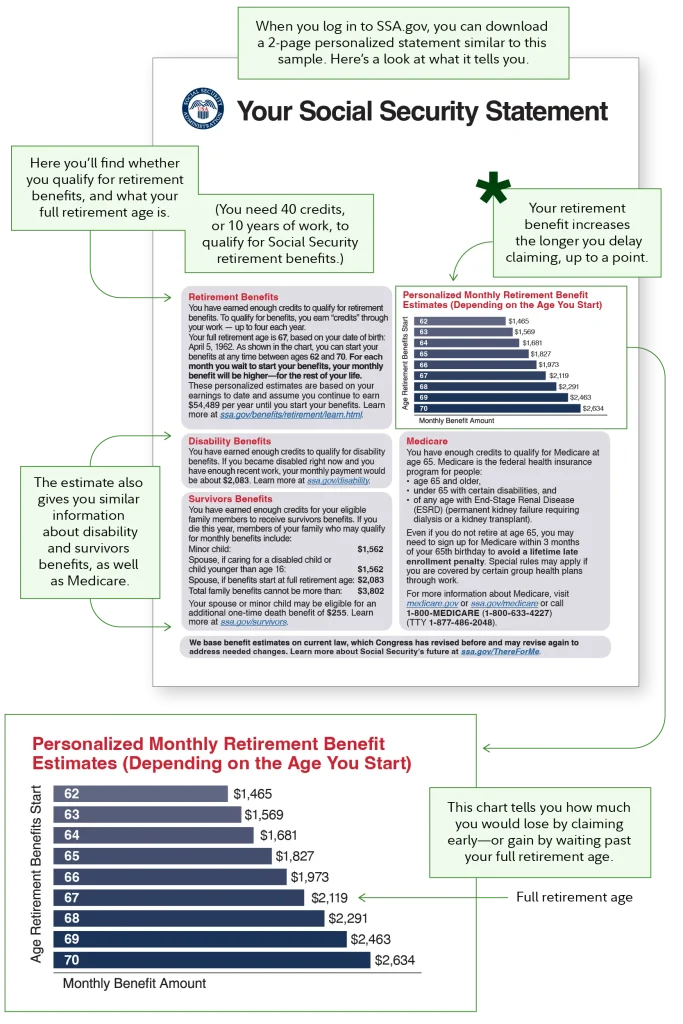

1. Your SSA Benefit Estimate

The first step is to log into my Social Security and request a personalized benefit statement. This document gives you a clear estimate of monthly income at various claiming ages (62, 66, 70, etc.). Keep this estimate handy; it’s the anchor point for all further calculations.

2. Private Retirement Accounts Overview

Next, list every private account you hold:

- Traditional and Roth IRAs

- Employer‑sponsored 401(k) or 403(b) plans

- Defined benefit pensions, if applicable

- Annuities and other investment vehicles

For each account, note the current balance, contribution limits, tax status, and projected growth rate. If you own a small business, the Understanding Retirement Accounts for Small Business Owners guide offers a deep dive into options like Solo 401(k)s and SEP IRAs.

3. Timing and Coordination

The art of retirement planning lies in timing. Delaying SSA benefits by a few years can boost your monthly check by up to 8% per year, but doing so may also mean you need to draw more from private accounts sooner. Conversely, tapping private savings early can preserve higher SSA payments later on. Modeling different scenarios helps you find the sweet spot.

How to Gather Accurate ssa Potential Private Retirement Benefit Information

Collecting reliable data is easier than you think if you follow a systematic approach. Below are practical steps you can take right now.

Step‑by‑Step Checklist

- Log into SSA’s online portal and download your “my Social Security” statement.

- Gather recent statements from all private retirement accounts, either through your provider’s portal or a consolidated spreadsheet.

- Calculate projected growth using a realistic annual return assumption (3‑5% for conservative portfolios, 6‑8% for aggressive ones).

- Identify tax implications for each withdrawal source; this influences net income.

- Run multiple “what‑if” scenarios—for example, claiming SSA at 62 versus 70 while drawing different percentages from private accounts.

Tools like retirement calculators, spreadsheet models, or professional financial software can simplify this process. The goal is to have a clear, numbers‑driven picture that reflects both public and private sources.

Strategies to Maximize Your ssa Potential Private Retirement Benefit Information

Now that you have the data, let’s explore how to turn it into a robust retirement income plan.

1. Delay SSA Benefits When Possible

If your health permits and you have sufficient private savings, consider postponing Social Security until age 70. The increased monthly benefit can serve as a “longevity insurance,” especially valuable if you expect a longer-than‑average retirement.

2. Use Tax‑Efficient Withdrawal Sequencing

Generally, the optimal order is:

- Taxable accounts (e.g., brokerage, non‑qualified annuities)

- Tax‑deferred accounts (Traditional IRA, 401(k))

- Tax‑free accounts (Roth IRA, Roth 401(k))

This sequence helps minimize taxes over the course of retirement, preserving more of your total income.

3. Consider a Hybrid Annuity

Hybrid annuities combine a guaranteed base benefit with a variable component tied to market performance. They can supplement SSA benefits while offering some upside potential. Review the fine print and compare expense ratios before committing.

4. Leverage Employer Matching Contributions

If your employer offers a matching contribution on a 401(k) plan, contribute at least enough to capture the full match. This “free money” directly boosts your private retirement pool, enhancing the overall ssa potential private retirement benefit information you’ll later rely on.

Common Pitfalls and How to Avoid Them

Even well‑intentioned savers can stumble into traps that erode their retirement security. Below are frequent mistakes and proactive fixes.

Overestimating Future SSA Benefits

Many assume the SSA will automatically increase benefits with inflation at a high rate. In reality, cost‑of‑living adjustments (COLAs) have been modest in recent years. Keep your expectations realistic and plan for a buffer in private savings.

Neglecting Health Care Costs

Medicare covers many medical expenses, but out‑of‑pocket costs, supplemental insurance premiums, and long‑term care can still be substantial. Factoring these into your ssa potential private retirement benefit information ensures you won’t be forced to withdraw more than planned.

Ignoring Required Minimum Distributions (RMDs)

Starting at age 73 (as of 2024), traditional retirement accounts require annual RMDs. Failing to take them can result in hefty penalties—up to 25% of the amount that should have been withdrawn. Incorporate RMD schedules into your cash‑flow model.

Tools and Resources to Keep Your ssa Potential Private Retirement Benefit Information Up‑to‑Date

Retirement planning isn’t a “set it and forget it” exercise. Your financial landscape evolves—salary changes, market swings, policy updates—so your data must stay current.

Recommended Resources

- Social Security Potential Private Retirement Benefit Information – What You Need to Know – A deeper dive into SSA calculations and private integration.

- Vanguard’s Target Retirement Funds (e.g., the Vanguard Target Retirement 2040 Fund Fact Sheet) – Simplify asset allocation for long‑term growth.

- The Definitive Guide to Retirement Income PDF – A comprehensive roadmap for building a sustainable retirement cash flow.

Regularly reviewing these materials, especially after major life events, helps you keep the ssa potential private retirement benefit information aligned with reality.

Putting It All Together: A Sample Roadmap

Below is a simplified illustration of how someone might combine SSA and private benefits over a 30‑year retirement horizon.

- Age 60: Estimate SSA benefit at full retirement age (66) – $2,200/month.

- Age 62: Begin part‑time work; contribute $5,000 annually to a Roth IRA.

- Age 66: Claim SSA benefits; total monthly income $2,200 plus $1,000 from Roth withdrawals.

- Age 70: If health permits, delay SSA for an extra four years, increasing benefit to $2,800/month. Private accounts cover living expenses during the delay.

- Age 75‑90: Use a blend of RMDs from a Traditional IRA, systematic withdrawals from a taxable brokerage, and the higher SSA benefit to fund lifestyle and health expenses.

This roadmap demonstrates how timing, tax efficiency, and strategic use of both public and private sources can create a resilient retirement income stream.

Remember, every plan should be tailored to your unique situation. The key takeaway is that “ssa potential private retirement benefit information” isn’t just a data point—it’s a dynamic toolkit that, when understood and applied correctly, can turn uncertainty into confidence.

Take the first step today: log into your SSA account, gather your private retirement statements, and start mapping out scenarios. With clear information and disciplined execution, you’ll be well on your way to a retirement that feels both secure and fulfilling.