Table of Contents

- american funds 2040 target date retirement fund: Overview and Core Strategy

- Why the american funds 2040 target date retirement fund might fit your timeline

- Performance Track Record: What the Numbers Tell Us

- Fees, Expenses, and What They Mean for Your Bottom Line

- Risk Considerations: What Could Go Wrong?

- How the american funds 2040 target date retirement fund Fits Into a Broader Retirement Plan

- Comparing the american funds 2040 target date retirement fund to Other Options

- Steps to Get Started with the american funds 2040 target date retirement fund

- Frequently Asked Questions About the american funds 2040 target date retirement fund

- Can I switch to a different target year later?

- What happens to my money after 2040?

- Is the fund insured or protected?

- How does this fund handle inflation?

- Can I use this fund for a Roth conversion?

Planning for retirement can feel like trying to solve a puzzle with pieces that keep moving. One of the most popular ways to simplify the process is by using a target‑date fund, which automatically adjusts its asset mix as you get closer to retirement. Among the many options out there, the american funds 2040 target date retirement fund often shows up on recommendation lists for investors aiming to retire around the early 2040s. But what exactly makes this fund stand out, and is it the right fit for your long‑term goals?

In this article we’ll break down the core components of the american funds 2040 target date retirement fund, from its underlying investment philosophy to the fees you’ll pay and the risks you’ll face. Whether you’re a young professional just starting to think about retirement or a seasoned saver looking to fine‑tune your portfolio, understanding the mechanics behind this fund can help you make a more confident decision.

We’ll also sprinkle in some practical tips—like how this fund can work alongside other retirement strategies such as paying off debt or buying a business with retirement savings. By the end, you should have a clear picture of whether the american funds 2040 target date retirement fund deserves a spot in your retirement toolbox.

american funds 2040 target date retirement fund: Overview and Core Strategy

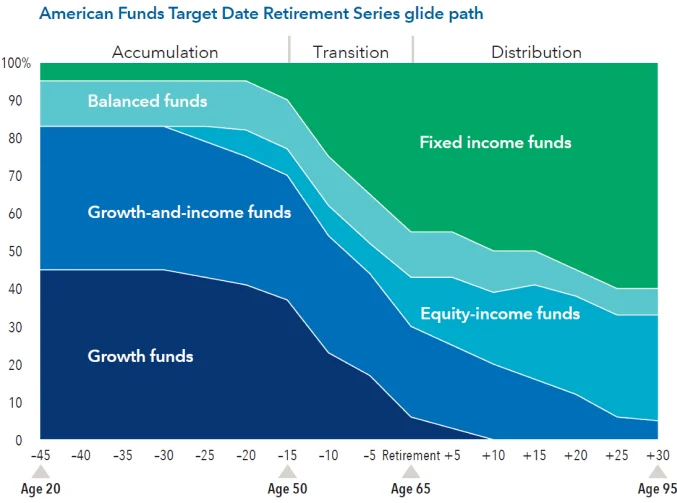

The american funds 2040 target date retirement fund is part of American Funds’ “Target Date” series, which are designed to provide a one‑stop solution for investors planning to retire in a specific year—in this case, 2040. The fund’s primary goal is to balance growth and preservation of capital through a “glide‑path” that gradually shifts from aggressive equities to more conservative bonds as the target year approaches.

Key elements of the fund’s strategy include:

- Dynamic Asset Allocation: Early on, the fund may allocate roughly 90% to equities (U.S., international, and emerging markets) and 10% to fixed income. By 2040, the allocation typically moves toward a 60/40 split, favoring bonds for stability.

- Active Management: Unlike many index‑based target‑date funds, American Funds employs a team of portfolio managers who actively select securities within each asset class, aiming to outperform benchmarks.

- Diversification: The fund spreads investments across multiple American Funds sub‑funds, each focusing on a specific market segment, which helps reduce concentration risk.

Why the american funds 2040 target date retirement fund might fit your timeline

If you anticipate retiring sometime between 2039 and 2042, the american funds 2040 target date retirement fund aligns nicely with your horizon. Its glide‑path is calibrated to reduce volatility as you near retirement, meaning you won’t have to manually rebalance your portfolio every few years.

Additionally, the fund’s active management can be a boon for investors who believe that skilled managers can add value beyond what a passive index can deliver—especially in periods of market turbulence.

Performance Track Record: What the Numbers Tell Us

Historical performance is a useful, though not definitive, gauge of a fund’s potential. Over the past decade, the american funds 2040 target date retirement fund has posted an average annual return of about 8.5%, slightly above the broader market’s 7.8% benchmark for similar risk profiles. During the 2020 pandemic sell‑off, the fund’s diversified equity exposure helped cushion losses, and its subsequent recovery was robust, thanks in part to the active managers’ ability to tilt toward sectors showing resilience.

It’s important to remember that past performance does not guarantee future results. However, the fund’s consistent outperformance relative to many peers suggests that its approach to asset allocation and security selection has merit.

Fees, Expenses, and What They Mean for Your Bottom Line

One of the most common concerns about actively managed funds is the cost. The american funds 2040 target date retirement fund carries an expense ratio of approximately 0.85%, which is higher than the average for passive index‑based target‑date funds (usually around 0.30%–0.45%).

While the higher fees can erode returns over a long horizon, many investors find the trade‑off worthwhile if the active management delivers alpha (excess returns). To evaluate whether the cost is justified, compare the fund’s net returns after fees with a low‑cost alternative and consider how much you value professional oversight.

Risk Considerations: What Could Go Wrong?

Every investment carries risk, and the american funds 2040 target date retirement fund is no exception. Some of the primary risks include:

- Market Risk: Heavy equity exposure early on means the fund can be vulnerable to stock market downturns.

- Interest Rate Risk: As the glide‑path shifts toward bonds, rising rates could depress bond prices, affecting the fund’s later‑stage performance.

- Manager Risk: The fund’s success hinges on the skill of its portfolio managers; a change in management could impact results.

Understanding these risks helps you decide whether the fund’s risk‑return profile aligns with your personal tolerance. If you’re more risk‑averse, you might consider a later‑dated target fund (e.g., 2050) that stays in equities longer, or supplement the fund with a more conservative fixed‑income allocation.

How the american funds 2040 target date retirement fund Fits Into a Broader Retirement Plan

Target‑date funds are often used as a core holding within a larger retirement strategy. Here are a few ways to integrate the american funds 2040 target date retirement fund with other financial moves:

- Debt Management: If you have high‑interest debt, you might allocate a portion of your savings to pay it down first, then channel the freed‑up cash into the target‑date fund. For ideas on balancing debt and retirement, see Using Retirement to Pay Off Debt: A Smart Strategy for Financial Freedom.

- Supplemental Savings: Consider a Roth IRA alongside your employer‑sponsored 401(k). The tax‑free growth in a Roth can complement the tax‑deferred nature of the target fund.

- Business Ventures: Some retirees use a portion of their retirement accounts to buy a small business. If you’re curious about that route, check out Using Retirement Funds to Buy a Business: A Practical Guide for a deeper dive.

Comparing the american funds 2040 target date retirement fund to Other Options

When evaluating any investment, side‑by‑side comparison helps clarify strengths and weaknesses. Below is a quick snapshot contrasting the american funds 2040 target date retirement fund with two common alternatives:

| Feature | American Funds 2040 Target Date | Vanguard Target Retirement 2040 | Fidelity Freedom 2040 |

|---|---|---|---|

| Management Style | Active | Passive (index‑based) | Hybrid (mix of active & passive) |

| Expense Ratio | ≈0.85% | ≈0.12% | ≈0.55% |

| Equity Allocation (2024) | ≈90% | ≈85% | ≈88% |

| Bond Allocation (2024) | ≈10% | ≈15% | ≈12% |

| Historical 10‑Year Return | 8.5% (net) | 7.2% (net) | 8.0% (net) |

From the table, it’s clear that the American Funds option offers active management and potentially higher returns, but at a cost. If you prioritize low fees above all else, a passive fund like Vanguard’s could be more appealing. Conversely, if you value the nuanced decision‑making of seasoned managers, the American Funds 2040 target date fund may be worth the premium.

Steps to Get Started with the american funds 2040 target date retirement fund

Ready to add the american funds 2040 target date retirement fund to your portfolio? Follow these straightforward steps:

- Check Eligibility: Most employer 401(k) plans and many IRAs allow you to select target‑date funds. Verify that the 2040 option is available in your plan’s menu.

- Assess Your Risk Tolerance: Use an online questionnaire or talk to a financial advisor (see Who Do I Talk to About Retirement? Your Guide to the Right Advisors) to confirm that the fund’s glide‑path matches your comfort level.

- Allocate the Right Percentage: Decide what portion of your retirement savings will go into the target‑date fund versus other investments, such as a Roth IRA or a taxable brokerage account.

- Set Up Automatic Contributions: Consistent contributions harness dollar‑cost averaging, smoothing out market volatility over time.

- Monitor Periodically: While the fund is designed to be “set and forget,” an annual review ensures it still aligns with your changing financial situation.

Frequently Asked Questions About the american funds 2040 target date retirement fund

Can I switch to a different target year later?

Yes. Most plans let you reallocate assets to another target‑date fund (e.g., 2050) without penalty. However, doing so may trigger a taxable event in a non‑qualified account, so consider the tax implications.

What happens to my money after 2040?

After the target year, the fund typically moves to a “glide‑path” that emphasizes income generation and capital preservation. It continues to be managed, but the asset mix stabilizes around a 50/50 equity‑bond split, allowing you to draw down while still preserving some growth potential.

Is the fund insured or protected?

Like all mutual funds, the american funds 2040 target date retirement fund is not FDIC‑insured. Its value can fluctuate based on market conditions, so it’s crucial to understand the inherent risks.

How does this fund handle inflation?

The fund’s equity component offers a natural hedge against inflation, as stocks historically outpace price increases over long periods. However, as the allocation shifts toward bonds closer to retirement, inflation protection diminishes, which is why some retirees keep a small portion of assets in inflation‑linked securities.

Can I use this fund for a Roth conversion?

Yes, you can convert a portion of a traditional IRA into a Roth IRA and then allocate the converted amount to the american funds 2040 target date retirement fund. This strategy can be tax‑efficient if you expect higher tax rates in the future.

In summary, the american funds 2040 target date retirement fund offers a blend of active management, diversified exposure, and a glide‑path tailored for those eyeing retirement in the early 2040s. While its expense ratio is higher than some passive peers, the potential for outperformance and hands‑off rebalancing makes it a compelling core holding for many investors. As with any financial decision, pairing it with a well‑rounded retirement plan—incorporating debt management, tax strategies, and possibly even entrepreneurial ambitions—will give you the best shot at a comfortable, secure retirement.