Table of Contents

- Why a Tailored Retirement Plan for Non Profit Organizations Matters

- Key Benefits of a Retirement Plan for Non Profit Organizations

- Choosing the Right Type of Retirement Plan for Non Profit Organizations

- 403(b) Plans: The Classic Non Profit Choice

- 457(b) Plans: For Government and Certain Non Profits

- SEP IRA and SIMPLE IRA: Low‑Cost Alternatives

- Hybrid Models: Combining Features for Flexibility

- Steps to Implement a Retirement Plan for Non Profit Organizations

- 1. Conduct a Needs Assessment

- 2. Evaluate Provider Options

- 3. Secure Funding and Matching Policies

- 4. Draft Plan Documents and Obtain Legal Review

- 5. Communicate the Plan to Employees

- 6. Monitor and Adjust Annually

- Maximizing Tax Benefits with a Retirement Plan for Non Profit Organizations

- Employer Contributions Are Tax‑Deductible

- Employee Salary Deferral Reduces Payroll Taxes

- Utilize the Small Business Retirement Plan Tax Credit

- Consider Roth Contributions for After‑Tax Savings

- Investment Options and Fiduciary Responsibility

- Target‑Date Funds: A Hands‑Free Approach

- Index Funds and ETFs: Low Fees, Broad Exposure

- Socially Responsible Investing (SRI)

- Addressing Common Challenges

- Limited Administrative Capacity

- Low Employee Participation

- Funding Constraints

- Regulatory Complexity

- Integrating Retirement Planning with Overall Financial Strategy

- Link Retirement Contributions to Budget Forecasts

- Leverage Fundraising for Matching Contributions

- Educate Board Members on Retirement Benefits

- Use Retirement Savings as a Retention Tool

Running a non profit organization means juggling a mission that serves the community with the practicalities of payroll, compliance, and long‑term sustainability. While many leaders focus on fundraising and program impact, one critical piece often gets sidelined: how to secure a stable retirement future for staff. A well‑designed retirement plan for non profit organizations not only attracts and retains talent but also reflects the organization’s commitment to its people.

In this article we’ll dive deep into the unique challenges and opportunities that non profit leaders face when building a retirement plan. From understanding the legal landscape to leveraging tax credits and choosing the right investment options, you’ll walk away with a clear roadmap to protect your team’s golden years without jeopardizing your mission.

Whether you’re a small charity with a handful of employees or a larger foundation with hundreds of staff, the principles below can be adapted to fit your budget, culture, and long‑term goals.

Why a Tailored Retirement Plan for Non Profit Organizations Matters

Non profit organizations operate under different fiscal constraints than for‑profit businesses, yet they compete for the same skilled workforce. Offering a competitive retirement plan signals that you value employees beyond their day‑to‑day contributions. It can also improve morale, reduce turnover, and ultimately enhance program delivery.

Moreover, certain retirement plans come with tax advantages that align well with the non profit’s exempt status. By carefully selecting a plan, you can maximize these benefits while keeping administrative costs in check.

Key Benefits of a Retirement Plan for Non Profit Organizations

- Talent attraction and retention: A solid retirement offering is often a deciding factor for candidates considering multiple job offers.

- Tax deductions: Contributions made by the organization are generally deductible, reducing overall tax liability.

- Employee morale: Knowing they have a safety net for the future can boost productivity and loyalty.

- Compliance credibility: Properly structured plans meet ERISA and IRS regulations, protecting the organization from penalties.

Choosing the Right Type of Retirement Plan for Non Profit Organizations

There isn’t a one‑size‑fits‑all solution. The best retirement plan for non profit organizations depends on size, budget, and administrative capacity. Below are the most common options, each with its own pros and cons.

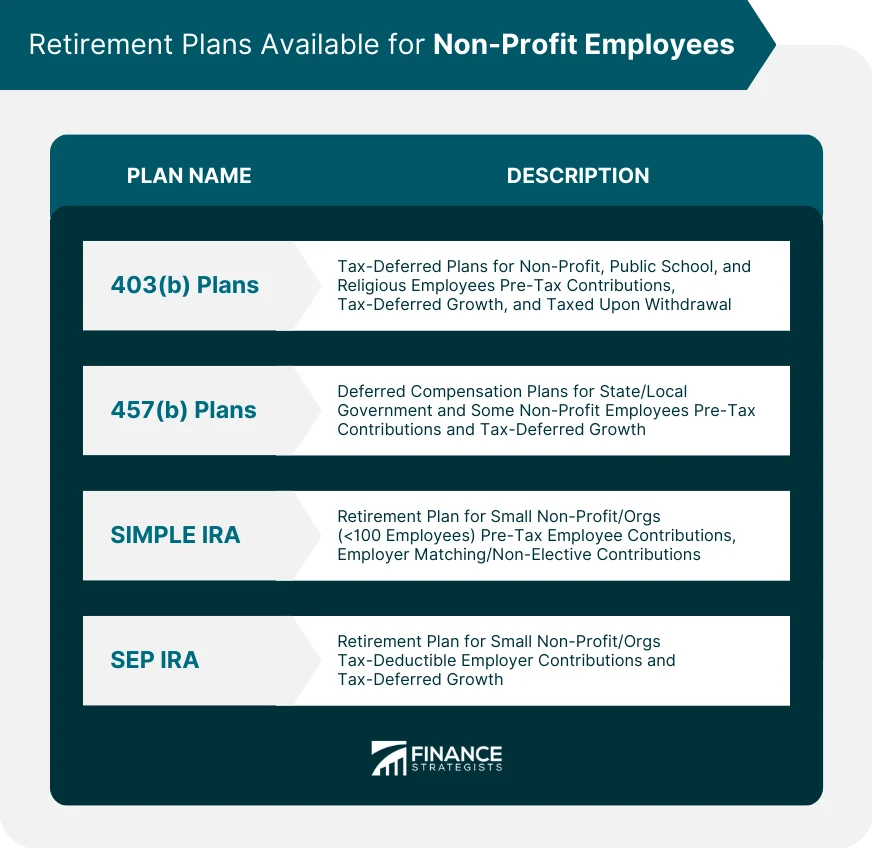

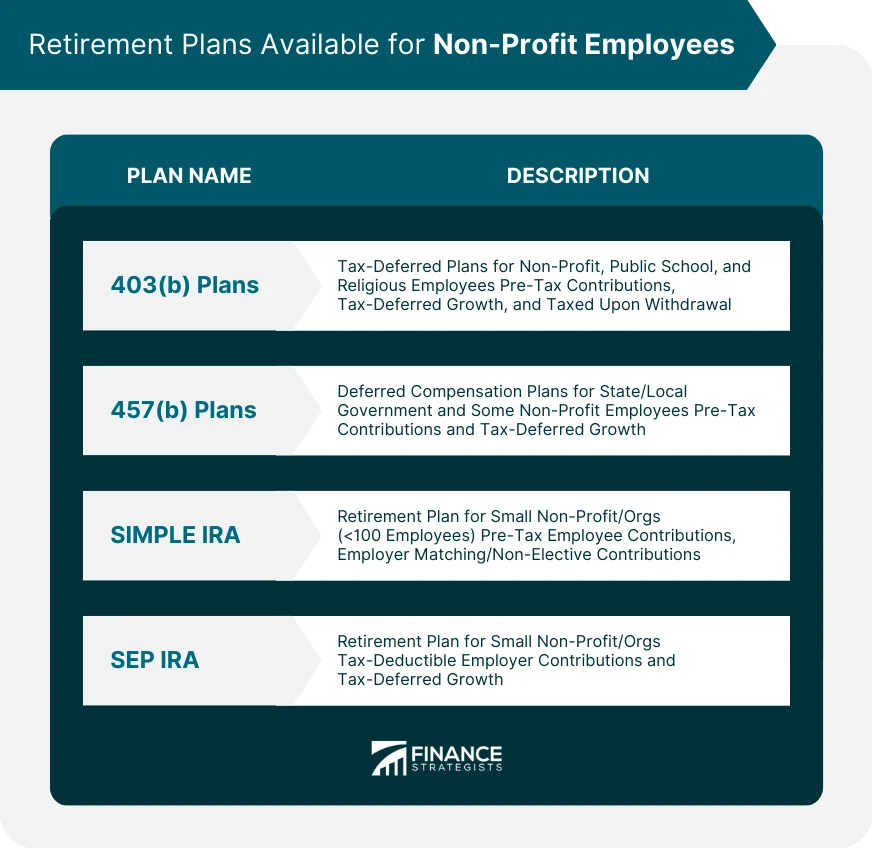

403(b) Plans: The Classic Non Profit Choice

The 403(b) is often the go‑to plan for schools, hospitals, and charities. It works similarly to a 401(k) but is tailored for tax‑exempt entities. Employees can defer a portion of their salary on a pre‑tax basis, and many employers provide matching contributions.

- Low set‑up cost and simple administration.

- Eligible for the Small Business Retirement Plan Tax Credit, which can offset up to $5,000 of plan‑related expenses in the first three years.

- Limited investment choices compared to 401(k) plans, but many providers now offer a broad range of mutual funds.

457(b) Plans: For Government and Certain Non Profits

If your organization is a governmental agency or a non profit that qualifies under specific IRS rules, a 457(b) plan may be an option. Unlike 403(b)s, 457(b) contributions are not subject to the “early withdrawal penalty” if the employee separates from service before age 59½, making it attractive for staff who anticipate early retirement.

SEP IRA and SIMPLE IRA: Low‑Cost Alternatives

For smaller nonprofits with limited administrative bandwidth, a SEP IRA or SIMPLE IRA can be a cost‑effective way to offer retirement benefits. Contributions are made by the employer only, simplifying payroll deductions.

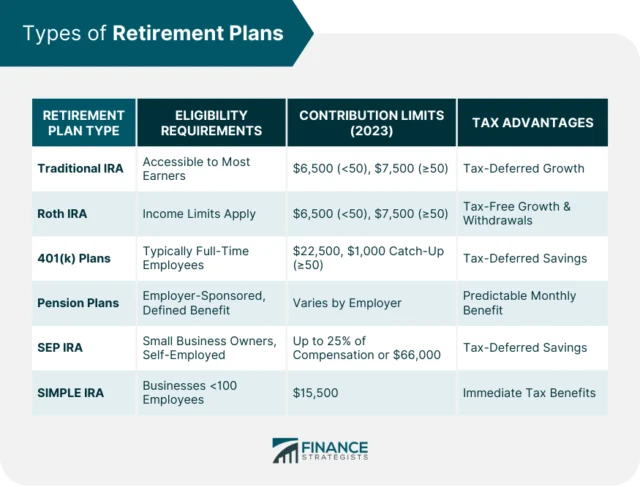

- SEP IRA allows contributions up to 25% of compensation (or $66,000 in 2024).

- SIMPLE IRA caps employee contributions at $15,500 (2024) with a mandatory employer match.

Hybrid Models: Combining Features for Flexibility

Some organizations layer a 403(b) with a SIMPLE IRA or a separate profit‑sharing component. This hybrid approach can cater to both entry‑level staff and senior leadership, offering varying contribution limits and matching formulas.

Steps to Implement a Retirement Plan for Non Profit Organizations

Implementing a retirement plan is more than just signing a contract with a provider. Follow these structured steps to ensure compliance, employee buy‑in, and long‑term success.

1. Conduct a Needs Assessment

Survey your staff to gauge interest, preferred contribution levels, and desired investment options. Understanding employee expectations helps you choose a plan that will actually be utilized.

2. Evaluate Provider Options

Look for providers that specialize in the non profit sector. Compare fees, investment menus, and fiduciary support. Many providers offer free educational webinars—a valuable tool for onboarding employees.

3. Secure Funding and Matching Policies

Decide on the matching formula (e.g., 50% of employee contributions up to 6% of salary). Align the match with your budget and the Small Business Retirement Plan Tax Credit to reduce net costs.

4. Draft Plan Documents and Obtain Legal Review

All retirement plans must be documented in a written plan document and filed with the IRS (Form 5500). Engage a legal expert familiar with non profit tax law to avoid costly mistakes.

5. Communicate the Plan to Employees

Transparency is key. Host a kickoff meeting, distribute clear FAQs, and provide calculators so staff can see the impact of contributions. A well‑communicated plan improves participation rates dramatically.

6. Monitor and Adjust Annually

Review participation, investment performance, and administrative costs each year. Adjust matching contributions or investment options as needed to stay competitive.

Maximizing Tax Benefits with a Retirement Plan for Non Profit Organizations

Tax efficiency is a major reason why non profit organizations can afford robust retirement benefits despite limited budgets. Here are the primary tax strategies you should leverage.

Employer Contributions Are Tax‑Deductible

All contributions your organization makes on behalf of employees are deductible as charitable expenses, reducing the organization’s taxable income.

Employee Salary Deferral Reduces Payroll Taxes

When employees defer a portion of their salary into a 403(b) or 457(b), those earnings are not subject to payroll (FICA) taxes, lowering the overall payroll tax burden.

Utilize the Small Business Retirement Plan Tax Credit

Eligible non profit employers can claim a credit of up to 50% of plan‑setup costs, capped at $5,000 per year for the first three years. This credit applies to most 403(b), 457(b), SEP IRA, and SIMPLE IRA plans.

Consider Roth Contributions for After‑Tax Savings

Many 403(b) providers now allow Roth (after‑tax) contributions. While these don’t reduce current taxable income, qualified withdrawals in retirement are tax‑free—a valuable option for employees who anticipate higher tax rates later.

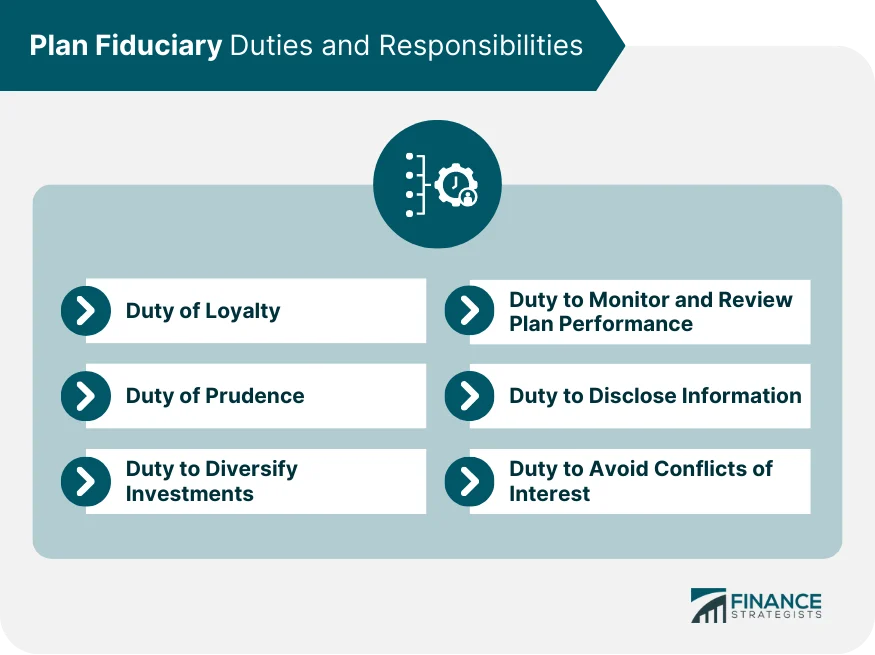

Investment Options and Fiduciary Responsibility

Choosing the right investment lineup is as important as selecting the plan type. Non profit organizations have a fiduciary duty to act in the best interest of participants, which means offering diversified, low‑cost options.

Target‑Date Funds: A Hands‑Free Approach

Target‑date funds automatically adjust asset allocation as participants near retirement. For example, the American Funds 2040 Target Date Retirement Fund provides a balanced glide path for employees expected to retire around 2040.

Index Funds and ETFs: Low Fees, Broad Exposure

Including a mix of U.S. equity, international equity, and bond index funds keeps costs low and performance competitive. Non profit boards should regularly review expense ratios to ensure they stay within industry benchmarks.

Socially Responsible Investing (SRI)

Many non profit staff are drawn to investments that align with the organization’s mission. Offering SRI options can boost participation and reinforce the organization’s values.

Addressing Common Challenges

Even with a solid framework, non profit organizations encounter hurdles. Below are practical solutions to the most frequent obstacles.

Limited Administrative Capacity

Outsource plan administration to a third‑party provider that offers full fiduciary services. This reduces the burden on staff and ensures compliance.

Low Employee Participation

Implement automatic enrollment with a modest default contribution (e.g., 3% of salary). Studies show participation rates jump from 30% to over 80% with auto‑enrollment.

Funding Constraints

If cash flow is tight, consider a phased match. Start with a modest 3% match and increase it as the organization’s financial health improves.

Regulatory Complexity

Stay current on IRS Form 5500 filing deadlines and annual nondiscrimination testing. Using a compliance service can prevent costly penalties.

Integrating Retirement Planning with Overall Financial Strategy

A retirement plan should not exist in isolation. Align it with your broader financial planning, budgeting, and fundraising strategies.

Link Retirement Contributions to Budget Forecasts

When drafting annual budgets, include projected employer contributions as a line item. This ensures that the plan is financially sustainable year after year.

Leverage Fundraising for Matching Contributions

Some foundations allow donors to earmark gifts for employee benefits, including retirement matching. Explore grant opportunities that specifically support workforce development.

Educate Board Members on Retirement Benefits

Board members often approve the plan and its funding. Providing them with clear, concise briefings—similar to the guide on Who to Talk to About Retirement Planning—helps secure ongoing support.

Use Retirement Savings as a Retention Tool

When key staff consider new opportunities, highlight the value of the organization’s retirement match and vesting schedule. This can be a decisive factor in retention negotiations.

By thoughtfully integrating a retirement plan for non profit organizations into the overall financial architecture, you not only safeguard your employees’ futures but also reinforce the organization’s reputation as a responsible and attractive employer.

In the end, the investment you make today in a robust retirement plan pays dividends in staff loyalty, program continuity, and compliance confidence. Take the first step, involve your team, and watch how a well‑structured retirement benefit can become a cornerstone of your non profit’s long‑term success.