Table of Contents

- How to Set Up Retirement Account: Choose the Right Type

- How to Set Up Retirement Account: Open the Account

- Funding Your New Retirement Account

- How to Set Up Retirement Account: Choose Investments Wisely

- Managing and Optimizing Your Retirement Account

- How to Set Up Retirement Account: Avoid Common Pitfalls

- Integrating Retirement Savings with Overall Financial Goals

**

Planning for retirement can feel like navigating a maze, especially when you’re just starting out. You might wonder where to begin, which account type fits your goals, or how much you should be saving each month. The good news is that setting up a retirement account isn’t rocket science—it’s a series of clear, manageable steps. In this article we’ll walk through everything you need to know, from picking the right vehicle to making your first contribution.

Whether you’re a recent graduate, a mid‑career professional, or someone who’s finally decided it’s time to get serious about the future, the process is fundamentally the same: you choose a plan, open the account, fund it, and then let compounding do its magic. Along the way, you’ll discover tips that can boost your savings, avoid costly mistakes, and even align your retirement strategy with other financial goals like debt repayment or insurance protection.

Ready to take control of your golden years? Let’s dive into the practical steps on how to set up retirement account that works for you.

How to Set Up Retirement Account: Choose the Right Type

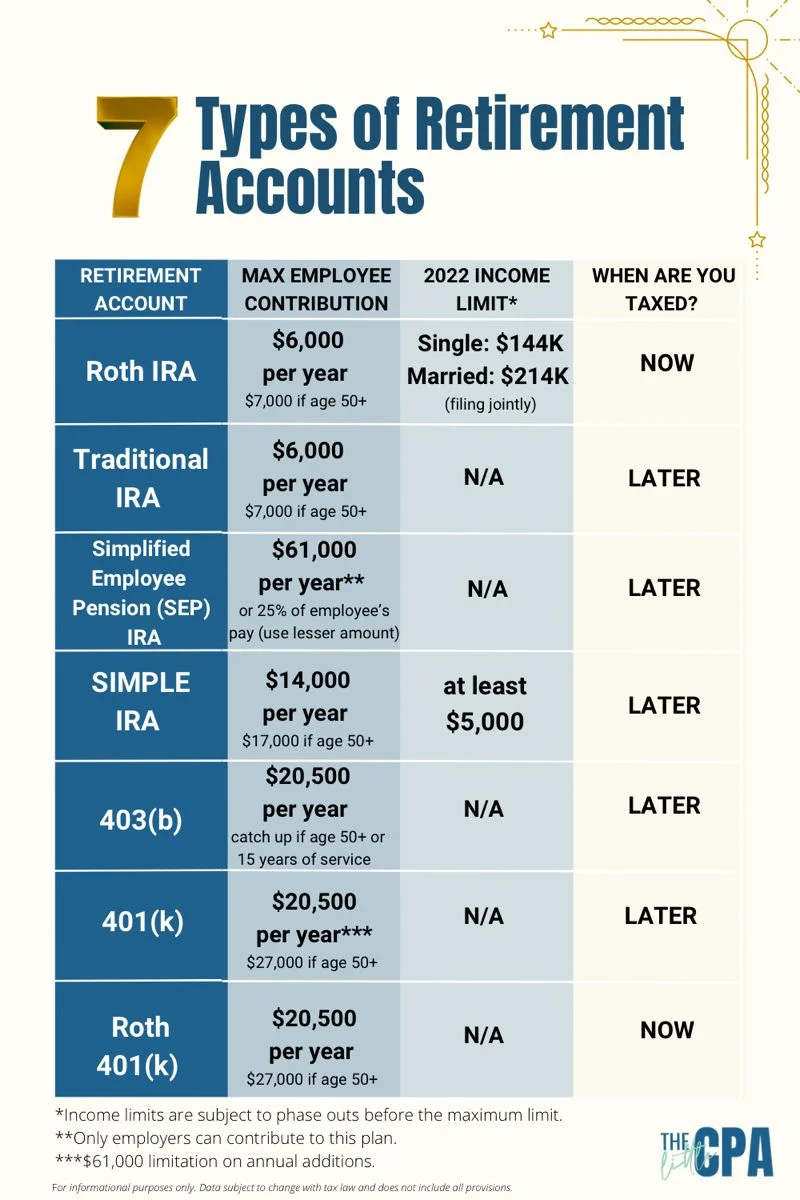

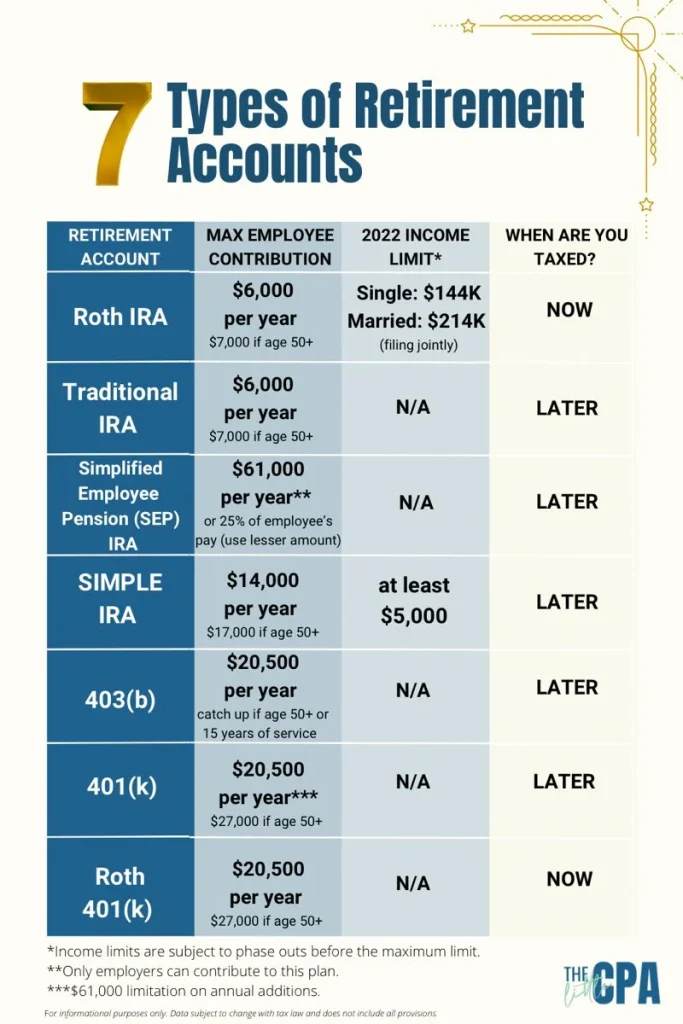

The first decision in how to set up retirement account is selecting the type of account that matches your employment situation, tax preferences, and investment horizon. Below are the most common options:

- Employer‑Sponsored Plans – 401(k), 403(b), or 457 plans are offered by many companies. They often come with matching contributions, which is essentially free money.

- Individual Retirement Accounts (IRAs) – Traditional IRA (tax‑deductible contributions) and Roth IRA (tax‑free withdrawals) are available to anyone with earned income.

- Self‑Employed Plans – Solo 401(k), SEP IRA, and SIMPLE IRA cater to freelancers, contractors, and small‑business owners.

If your employer provides a 401(k) with a match, that’s usually the best place to start. You can still open an IRA later to diversify tax treatment.

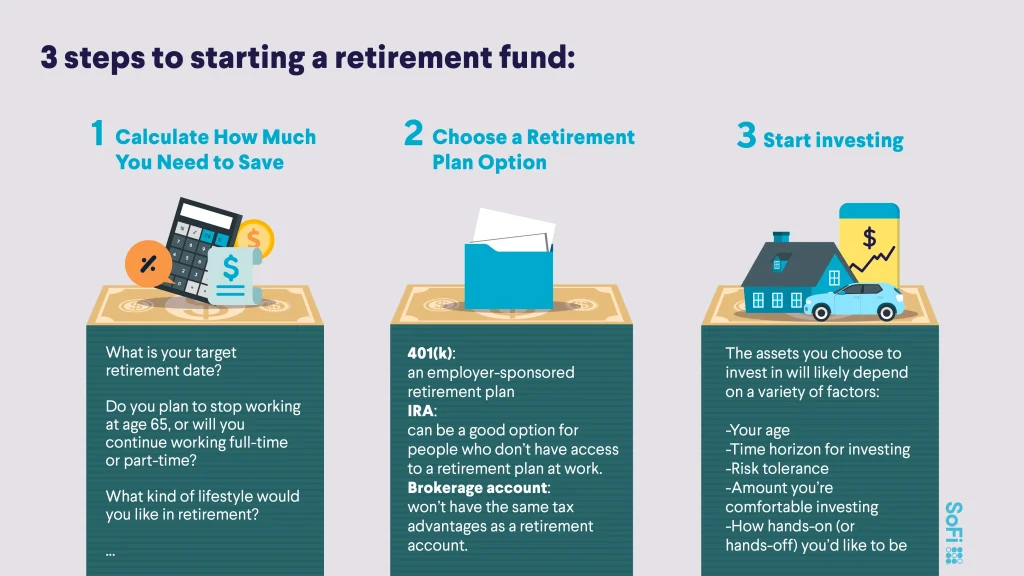

How to Set Up Retirement Account: Open the Account

Once you’ve chosen the right vehicle, the next step in how to set up retirement account is the actual opening process. Most financial institutions now allow you to complete the entire procedure online in just a few minutes:

- Gather personal information (Social Security number, driver’s license, employment details).

- Decide on a beneficiary – someone who will inherit the assets if something happens to you.

- Select your investment lineup – many platforms offer target‑date funds, which automatically adjust risk as you age. For a deeper look at target‑date funds, check out this article on American Funds 2040 Target Date Retirement Fund.

Most providers will ask you to set up a username and password, and you’ll receive a confirmation email once the account is active. Keep that login info safe; you’ll need it to make contributions, rebalance, and monitor performance.

Funding Your New Retirement Account

Now that the account is live, you need to start feeding it. Here’s how to make the most of your contributions:

- Automatic Payroll Deductions – If you’re using an employer plan, set your contribution percentage in the HR portal. Aim for at least enough to capture the full employer match.

- Direct Bank Transfers – For IRAs, link your checking account and schedule recurring transfers. Even $50 a month can grow significantly over decades.

- Lump‑Sum Contributions – Whenever you receive a bonus, tax refund, or inheritance, consider funneling a portion directly into your retirement account.

Remember the IRS contribution limits: for 2024, the limit is $23,000 for 401(k)s (including catch‑up contributions for those 50+) and $7,000 for IRAs. Staying under these caps avoids penalties.

How to Set Up Retirement Account: Choose Investments Wisely

Choosing the right investments is a core part of how to set up retirement account that actually works. If you’re not comfortable picking individual stocks, consider these low‑maintenance options:

- Target‑Date Funds – They automatically shift from aggressive to conservative as your target retirement year approaches.

- Index Funds – Low‑cost funds that track major market indices like the S&P 500.

- Exchange‑Traded Funds (ETFs) – Offer diversification and can be bought and sold like stocks.

For a deeper dive into a specific target‑date fund, see the article on American Funds 2040 Target Date Retirement Fund – A Deep Dive for Future Retirees. It explains why such funds can be a smart core holding for many investors.

Managing and Optimizing Your Retirement Account

Opening and funding the account are just the beginning. Ongoing management ensures you stay on track and adapt to life changes. Here are some best practices:

- Review Annually – Check your asset allocation, contribution rate, and beneficiary designations each year.

- Rebalance When Needed – If stocks have outperformed and now make up a larger share than intended, shift some into bonds or other assets.

- Take Advantage of Tax Strategies – Consider Roth conversions in low‑income years to diversify tax exposure.

If you’re a nonprofit employee, you might explore a Retirement Plans for Non‑Profit Organizations that offer unique contribution limits and matching rules.

How to Set Up Retirement Account: Avoid Common Pitfalls

Even with a solid plan, a few missteps can erode your future wealth. Watch out for these traps:

- Leaving money in a low‑interest savings account instead of investing it.

- Failing to capture the full employer match – it’s free money you’d be leaving on the table.

- Making early withdrawals – penalties and lost compound growth can be severe.

- Neglecting to update beneficiaries after major life events.

One surprising mistake is overlooking the role of insurance in retirement. For those interested in combining protection with savings, Life Insurance as a Retirement Plan offers an alternative perspective worth exploring.

Integrating Retirement Savings with Overall Financial Goals

Retirement planning doesn’t happen in a vacuum. It should complement other financial priorities such as debt repayment, emergency savings, and education funding. One strategic approach is using retirement assets to pay off high‑interest debt once you’ve built a solid cushion. Learn more about this tactic in Using Retirement to Pay Off Debt.

If you’re uncertain about where to start, consider speaking with a certified financial planner. The article Who Do I Talk to About Retirement? offers guidance on picking the right advisor who can tailor a plan to your unique situation.

In summary, mastering how to set up retirement account boils down to three core actions: choose the appropriate account type, fund it consistently, and manage it wisely over time. By following the steps outlined above, you’ll build a retirement nest egg that grows with you, adapts to market changes, and ultimately provides the financial freedom you deserve.

Take the first step today—open that account, set up an automatic contribution, and watch your future self thank you.