Table of Contents

- Understanding life insurance as a retirement plan

- Why choose life insurance as a retirement plan?

- Key types of policies that work as retirement tools

- Whole life insurance

- Universal life insurance

- Indexed universal life (IUL)

- Variable universal life (VUL)

- How to integrate life insurance with your broader retirement strategy

- Step‑by‑step integration checklist

- Real‑world scenario: blending with a 401(k)

- Tax considerations you can’t ignore

- Policy loans vs. withdrawals

- Impact on estate taxes

- Required Minimum Distributions (RMDs)

- Potential pitfalls and how to avoid them

- High premiums and opportunity cost

- Policy lapse risk

- Complexity and fees

- Over‑borrowing

- Choosing the right advisor and resources

- Real‑life success stories

- Final thoughts on making life insurance work for your retirement

When people think about retirement, the first thing that pops into mind is usually a 401(k) or an IRA. Yet there’s a financial tool that often flies under the radar but can play a starring role in a well‑rounded retirement strategy: life insurance. Not only does it protect your loved ones if the unexpected happens, it can also act as a reliable source of income, a tax‑advantaged savings vehicle, and even a way to leave a legacy.

In this article we’ll walk through why and how you might consider life insurance as a retirement plan, break down the different types that work best for this purpose, and share practical tips for integrating it with your other retirement accounts. By the end, you’ll have a clearer picture of whether this approach fits your long‑term goals, and how to make it work without over‑complicating your financial picture.

Understanding life insurance as a retirement plan

The phrase life insurance as a retirement plan may sound contradictory at first—after all, life insurance is primarily about protection, while retirement planning is about accumulation. The magic happens when you look at the cash‑value component of permanent life policies, such as whole life or universal life. These policies build a tax‑deferred savings element that you can tap into during retirement, often with fewer restrictions than traditional retirement accounts.

Unlike term insurance, which expires after a set period, permanent policies stay in force for life (as long as premiums are paid). Part of each premium goes toward the death benefit, and the rest fuels the policy’s cash value. Over time, that cash value grows at a predictable rate, and you can borrow against it, withdraw it, or even use it to pay future premiums. This flexibility makes it a viable supplement—or even an alternative—to more conventional retirement vehicles.

Why choose life insurance as a retirement plan?

- Tax advantages: Cash value growth is tax‑deferred, and policy loans are generally tax‑free as long as the policy remains in force.

- Liquidity when you need it: You can access the cash value without the early‑withdrawal penalties that hit 401(k)s and IRAs before age 59½.

- Protection for loved ones: The death benefit remains intact, offering a financial safety net for heirs.

- Predictable growth: Many whole‑life policies guarantee a minimum interest rate, providing a stable, low‑volatility component in a retirement portfolio.

- Legacy planning: You can designate beneficiaries to receive the death benefit, which can be used to pay estate taxes or fund charitable gifts.

It’s not a one‑size‑fits‑all solution, but for people who value both protection and a steady, tax‑advantaged source of funds, life insurance as a retirement plan can be a compelling addition.

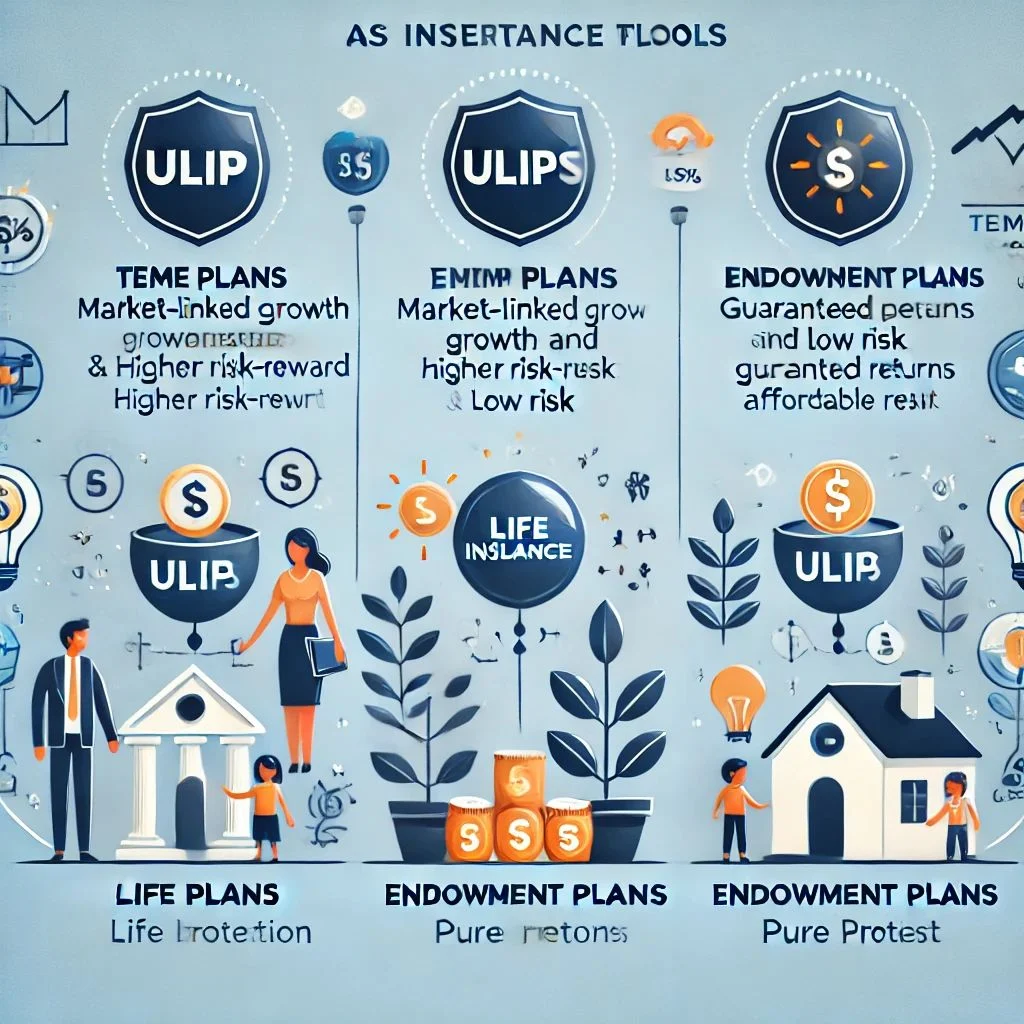

Key types of policies that work as retirement tools

Not every life insurance product is created equal when it comes to retirement planning. Below are the main categories that merit a closer look.

Whole life insurance

Whole life is the classic “set‑it‑and‑forget‑it” permanent policy. Premiums are fixed, and the cash value grows at a guaranteed rate plus dividends (if the insurer is a mutual company). Because the growth is predictable, whole life can act like a low‑risk bond in your retirement mix.

Universal life insurance

Universal life offers more flexibility. You can adjust premium payments and death benefits within certain limits, and the cash value is tied to a declared interest rate that can fluctuate. This policy can be attractive if you want to tailor contributions as your income changes over the years.

Indexed universal life (IUL)

IUL policies link cash‑value growth to a stock market index (like the S&P 500) while capping both gains and losses. For retirees who want a bit of market upside without the full downside risk, an IUL can provide a middle ground.

Variable universal life (VUL)

With VUL, the cash value is invested in sub‑accounts similar to mutual funds, offering the highest growth potential—but also the most risk. If you’re comfortable with market volatility and have a long time horizon, a VUL can serve as a “self‑directed” retirement account.

How to integrate life insurance with your broader retirement strategy

Adding life insurance as a retirement plan doesn’t mean you abandon your 401(k) or IRA. Think of it as an extra layer that can fill gaps, provide liquidity, or hedge against market downturns. Here are some ways to blend the two.

Step‑by‑step integration checklist

- Assess your protection needs first: Calculate how much death benefit you’d need to cover debts, mortgage, college costs, and income replacement for your spouse.

- Determine your cash‑value goals: Decide how much you’d like the policy to contribute to your retirement income stream.

- Choose the right policy type: If you prefer stability, whole life may be best; if you want flexibility, universal life could suit you.

- Fund the policy strategically: Many advisors recommend paying the premium for the first 10‑15 years, then using the cash value to cover later premiums.

- Plan for policy loans: Establish a loan repayment plan to keep the policy from lapsing and to protect the death benefit.

- Coordinate with other accounts: Use the cash value as a bridge during market dips, or as a source of tax‑free income after you’ve maxed out Roth contributions.

For example, imagine a couple in their early 60s who have maxed out their Roth IRA contributions and are concerned about required minimum distributions (RMDs) from traditional retirement accounts. By borrowing against a whole‑life policy, they can meet living expenses without triggering additional taxable income, preserving the tax‑advantaged portion of their retirement savings.

Real‑world scenario: blending with a 401(k)

Suppose you have a 401(k) balance of $500,000 and a whole‑life policy with a $200,000 cash value. In a year when the stock market is down, you could take a loan against the policy to cover part of your expenses, allowing your 401(k) investments to stay fully invested for a potential rebound. When the market recovers, you repay the loan using the 401(k) withdrawals, effectively using the policy as a “financial buffer.”

Tax considerations you can’t ignore

One of the biggest draws of life insurance as a retirement plan is the tax treatment. However, it’s essential to understand the rules to avoid unintended consequences.

Policy loans vs. withdrawals

When you borrow against the cash value, the loan is not considered taxable income—as long as the policy remains in force. The interest you pay goes back into the policy, further boosting cash value. In contrast, if you withdraw more than your cost basis (the total premiums you’ve paid), the excess is taxable as ordinary income.

Impact on estate taxes

The death benefit is generally income‑tax free to beneficiaries, but it can be included in the estate for estate tax purposes if you own the policy directly. To keep the benefit out of the estate, many retirees use an irrevocable life insurance trust (ILIT). This is an advanced strategy, so consulting an estate planning attorney is wise.

Required Minimum Distributions (RMDs)

Traditional retirement accounts force you to take RMDs after age 72, which can push you into a higher tax bracket. Using life insurance as a supplemental income source can help you manage your cash flow and potentially reduce the size of required withdrawals, keeping your overall tax burden lower.

Potential pitfalls and how to avoid them

While life insurance as a retirement plan offers many perks, it’s not without drawbacks. Being aware of the common traps can save you from costly mistakes.

High premiums and opportunity cost

Permanent policies are more expensive than term policies. If you allocate too much of your budget to premiums, you might miss out on higher‑return investments elsewhere. A balanced approach often involves using a modest death benefit combined with other retirement vehicles.

Policy lapse risk

If you stop paying premiums and the cash value isn’t sufficient to cover them, the policy can lapse, resulting in loss of both coverage and accumulated cash value. Setting up automatic premium payments and monitoring the policy’s health can mitigate this risk.

Complexity and fees

Universal and variable policies come with fees—administrative, cost‑of‑insurance, and investment management charges. Read the policy illustration carefully, and ask your advisor to walk you through each line item.

Over‑borrowing

Taking out large loans can erode the death benefit and the cash value growth. A good rule of thumb is to keep outstanding loans below 25% of the cash value, ensuring the policy remains robust.

Choosing the right advisor and resources

Because life insurance as a retirement plan straddles both insurance and investment realms, it’s crucial to work with professionals who understand both sides. Look for a certified financial planner (CFP) or a chartered life underwriter (CLU) who has experience designing integrated retirement strategies.

Don’t forget to explore related topics that can complement your planning. For instance, if you’re facing an unexpected early retirement due to injury, you might want to read Early Retirement Due to Injury at Work – A Complete Guide to see how insurance and retirement savings can intersect. Likewise, the article Do Retired Teamsters Have Life Insurance? A Complete Guide offers a practical look at how retirees can leverage existing coverage for their later years.

Real‑life success stories

Many retirees have quietly used life insurance as part of their retirement income mix. One couple in their late 60s, both former teachers, purchased a $500,000 whole‑life policy in their early 50s. Over 15 years, the policy accumulated a cash value of $150,000. When the husband retired, they borrowed $30,000 to cover a home renovation, paying it back over five years with minimal impact on the death benefit. The couple now enjoys a steady, tax‑free supplement to their Social Security and pension income.

Another example involves a small‑business owner who used an indexed universal life policy to fund a buy‑sell agreement with his partner. The policy’s cash value grew enough to buy out his partner’s share without forcing the business to liquidate assets, illustrating the dual role of protection and financial flexibility.

Final thoughts on making life insurance work for your retirement

Integrating life insurance as a retirement plan can bring peace of mind, tax efficiency, and a reliable source of cash when you need it most. The key is to approach it methodically: determine your protection needs, select the appropriate policy type, fund it wisely, and monitor its performance alongside your traditional retirement accounts.

Remember, no single product can replace a diversified portfolio, but when used thoughtfully, life insurance can fill gaps that other vehicles leave open—especially around liquidity, tax‑free income, and legacy planning. If you’re unsure where to start, schedule a conversation with a qualified financial advisor who can tailor a solution to your unique situation. With the right strategy, life insurance as a retirement plan can become a powerful pillar supporting your golden years.