Table of Contents

- the changing world of retirement planning: Why Traditional Models No Longer Fit

- New Investment Vehicles Shaping Retirement

- Embracing the changing world of retirement planning with Robo‑Advisors

- The Role of Health and Longevity in Modern Retirement Strategies

- How the changing world of retirement planning Impacts Social Security Decisions

- Flexible Income Streams and the Gig Economy

- Technology, Education, and Ongoing Adaptation

Retirement used to be a simple equation: work for 30‑40 years, save a portion of your paycheck, and then enjoy a leisurely life on a fixed pension or Social Security check. Today, that picture looks very different. Longer life expectancies, volatile markets, and a gig‑based economy mean that the old playbook no longer guarantees peace of mind. In this article we’ll dive deep into the forces reshaping how people think about their golden years and what practical steps you can take to stay ahead.

One of the biggest shifts is the move from defined‑benefit plans—those traditional pensions that promised a set monthly amount—to defined‑contribution accounts like 401(k)s and IRAs. While those vehicles give you more control, they also place the investment risk squarely on your shoulders. That change alone is a cornerstone of the changing world of retirement planning, and it forces us to become more proactive, more educated, and more flexible.

But it isn’t just about numbers on a screen. The way we view work, health, and even purpose after the 65‑year mark is evolving. Some retirees are launching startups, others are volunteering abroad, and many are blending part‑time gigs with travel. All of these trends intersect, creating a complex, dynamic landscape that demands a fresh approach.

the changing world of retirement planning: Why Traditional Models No Longer Fit

Decades ago, a reliable pension plus Social Security was enough to cover most retirees’ basic needs. Today, three major forces make that safety net insufficient for many:

- Longevity risk: The average life expectancy in many developed countries now exceeds 80 years, meaning retirees must fund 20‑30 years of post‑work living, not just a decade.

- Market volatility: The last two decades have seen rapid swings—from the dot‑com bust to the 2008 crisis, and the recent pandemic‑driven turbulence.

- Changing career patterns: More workers switch jobs, freelance, or take on gig work, which often lack employer‑sponsored retirement plans.

Because of these pressures, the changing world of retirement planning pushes you to think beyond “just saving.” It asks you to consider how you’ll generate income, manage risk, and preserve health over an extended retirement horizon.

New Investment Vehicles Shaping Retirement

Traditional stock‑bond allocations are still important, but investors now have a richer toolbox. Here are a few options gaining traction:

- Target‑date funds: These automatically adjust the asset mix as you approach a chosen retirement year, simplifying the rebalancing process. For a deep dive into a specific offering, check out the Vanguard Target Retirement 2040 Trust Select – In‑Depth Review & Tips article.

- Robo‑advisors: Algorithms create diversified portfolios at a fraction of the cost of human advisors, making them a popular choice for tech‑savvy retirees.

- Real‑asset exposure: Real estate, infrastructure, and even farmland can act as inflation hedges, providing steady cash flow while diversifying risk.

- ESG and impact investing: Many retirees want their money to reflect personal values, supporting sustainable projects that also offer competitive returns.

These alternatives can help you address the changing world of retirement planning by reducing reliance on a single income source and smoothing out market bumps over time.

Embracing the changing world of retirement planning with Robo‑Advisors

Robo‑advisors have become a game‑changer for people who want a hands‑off approach. After you set your risk tolerance, the platform automatically rebalances, harvests tax losses, and even suggests withdrawals that minimize tax impact. Because they use sophisticated modeling, they can project how long your savings might last under various scenarios—a crucial capability in the changing world of retirement planning.

If you’re just starting, a solid first step is to understand how to open an account. The guide on how to get a retirement account – a practical step‑by‑step guide walks you through the paperwork, contribution limits, and tax implications, making the process less intimidating.

The Role of Health and Longevity in Modern Retirement Strategies

Living longer is a blessing, but it also means you’ll likely face more medical expenses. In the changing world of retirement planning, health care costs are no longer an afterthought; they’re a central pillar of any robust strategy.

- Health Savings Accounts (HSAs): If you’re eligible, an HSA lets you save pre‑tax dollars for qualified medical expenses, and the funds roll over year after year.

- Long‑term care insurance: While pricey, this product can protect your assets from the potentially devastating cost of assisted living or nursing home care.

- Wellness investing: Some modern funds focus on companies that promote preventive health, giving you indirect exposure to the upside of a healthier retiree population.

Integrating these elements early—perhaps while you’re still employed—helps you avoid a scenario where a health crisis erodes your retirement savings, a risk amplified by the changing world of retirement planning.

How the changing world of retirement planning Impacts Social Security Decisions

Social Security remains a cornerstone of retirement income for most Americans, but the optimal claiming age is no longer a one‑size‑fits‑all answer. With longer life expectancies, delaying benefits can significantly boost monthly payouts, yet for some, taking benefits early provides essential cash flow for health expenses or debt repayment.

When you run the numbers, consider:

- Your projected longevity based on family health history.

- Current and anticipated medical costs.

- The presence of other guaranteed income streams, such as annuities or pension payouts.

Financial planning software or a qualified advisor can model these variables, helping you decide whether to claim at 62, 70, or somewhere in between.

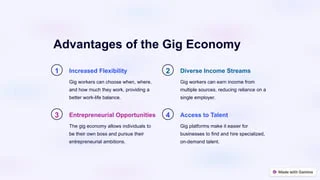

Flexible Income Streams and the Gig Economy

One of the most visible signs of the changing world of retirement planning is the rise of part‑time or freelance work after age 65. Whether you’re a seasoned accountant offering consulting services, a teacher tutoring online, or a craftsman selling on Etsy, these gigs can supplement your savings and keep you mentally engaged.

There are tax advantages, too. Income earned after retirement can be offset by deductions for home office expenses, mileage, or retirement‑age business expenses. Additionally, certain self‑employment income can be contributed to a Solo 401(k) or a Simplified Employee Pension (SEP) IRA, allowing you to keep saving even while you’re technically “retired.”

If you have entrepreneurial ambitions, the guide on using retirement funds to start a business – a practical guide explains how to leverage a Roth IRA or a self‑directed 401(k) without incurring penalties, provided you follow the rules.

Technology, Education, and Ongoing Adaptation

Technology is both a driver and a solution in the changing world of retirement planning. From mobile budgeting apps that sync with your investment accounts to virtual financial advisors that use AI to suggest optimal withdrawal strategies, the digital landscape empowers retirees to stay informed and agile.

Education remains the cornerstone. Many retirees now attend webinars, join online communities, or take short courses on topics like “tax‑efficient retirement withdrawals” or “cryptocurrency for seniors.” The more you understand, the better you can navigate the shifting terrain.

Finally, remember that retirement planning is not a set‑it‑and‑forget‑it exercise. Review your portfolio at least annually, adjust for any life‑changing events (like a health diagnosis or a major inheritance), and stay open to new income ideas. The changing world of retirement planning rewards those who treat their future as a living project, not a static destination.

In summary, the landscape of retirement today is a mosaic of longer lives, diversified investments, health‑focused budgeting, and flexible work opportunities. By embracing these trends, you can design a retirement that is secure, adaptable, and aligned with the lifestyle you truly want.