Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Ever wondered why you’re asked to pay a monthly or yearly amount just to keep a safety net in place? That amount is called a premium, and it’s the lifeblood of every insurance company. While most of us accept the cost as a necessary expense, the mechanics behind why insurers charge premiums are far more intricate than a simple “we need money” explanation.

In this article we’ll peel back the layers of insurance pricing, from the mathematics of risk to the business realities that keep a company solvent. By the end, you’ll not only grasp why premiums exist, but also how you can influence the amount you pay and where you might find savings.

why do insurance companies charge premiums: the core reasons

The short answer is simple: premiums fund the claims that policyholders file. But there’s a cascade of strategic, actuarial, and regulatory reasons that shape the exact number you see on your bill.

why do insurance companies charge premiums – covering expected losses

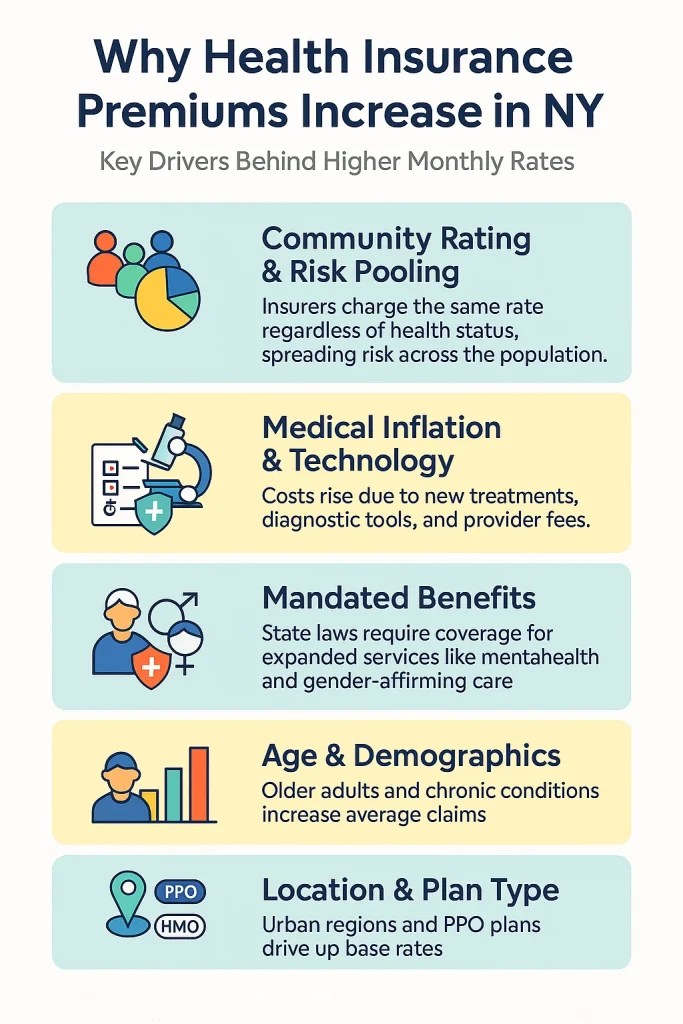

At the heart of every policy lies the principle of risk pooling. Insurers collect premiums from a large group of people, then use that pool to pay the few who experience a covered loss. Actuaries—specialists in statistics and finance—calculate the “expected loss” for each type of coverage. This expected loss is the average cost the insurer anticipates paying out per policyholder, based on historical data, trends, and predictive models.

For example, if a car insurer determines that, on average, a driver in a certain zip code files a claim worth $1,200 each year, the premium must at least cover that amount, plus a margin for other expenses and profit. This is the baseline reason why insurance companies charge premiums.

Risk assessment and underwriting: tailoring the price to you

Not every driver, homeowner, or business faces the same risk. Underwriting is the process insurers use to evaluate each applicant’s unique profile. Factors such as age, driving record, credit score, location, and even the type of vehicle you drive can shift your premium up or down.

Think of it like a gym membership: you pay more if you want access to premium equipment and personal trainers. Similarly, a policyholder with a clean driving history and a low‑risk vehicle will generally see a lower premium than someone with multiple accidents and a high‑performance sports car.

Want a concrete example? If you’re looking for a cost‑effective solution for a fleet, reading about cheap car insurance for business use can give you insight into how bundling and risk management lower premiums for commercial drivers.

The business side: operating costs and profit margins

Insurance is a business, and like any other, it incurs operating expenses—staff salaries, technology platforms, marketing, regulatory compliance, and reinsurance (insurance for insurers). These costs must be covered before the company can turn a profit.

Reinsurance, in particular, is a crucial piece of the puzzle. Insurers purchase reinsurance to protect themselves against catastrophic losses, such as a natural disaster that generates thousands of claims at once. The cost of this protection is baked into the premium you pay.

Profit isn’t just a nice‑to‑have; it’s essential for growth, innovation, and maintaining solvency. Regulators require insurers to hold a certain level of capital, and a healthy profit margin ensures they can meet those requirements even during tough loss years.

External influences: market competition and regulations

Even with solid actuarial data, insurers can’t set premiums in a vacuum. Competitive forces push companies to price aggressively to attract customers, while regulatory bodies set limits on how much can be charged for certain lines of business.

In many states, the Department of Insurance reviews rates to ensure they’re not excessive, inadequate, or unfairly discriminatory. This oversight can force insurers to adjust premiums up or down, depending on the findings.

If you’re curious about regional price differences, checking resources like the cheapest car insurance in Florida can illustrate how local market dynamics and state regulations shape premium structures.

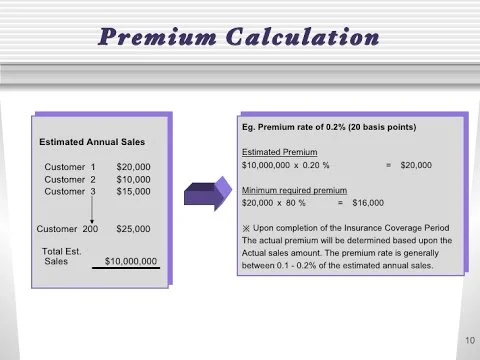

How premiums are calculated: the formula behind the number

While the exact formulas are proprietary, most insurers follow a general framework:

- Base rate: Derived from historical loss data for a specific risk class.

- Exposure rating: Adjusts the base rate based on the level of exposure (e.g., vehicle value, property size).

- Risk modifiers: Add or subtract points for specific risk factors (e.g., claim history, safety features).

- Loadings: Incorporates administrative costs, commissions, and profit margins.

- Discounts: Applies incentives like multi‑policy bundles, good driver discounts, or safety device credits.

The sum of these components yields the final premium. Understanding each piece helps you see where you might influence the outcome—by improving your risk profile, opting for higher deductibles, or bundling policies.

Strategies to lower your premium without sacrificing coverage

Now that you know why insurance companies charge premiums, let’s explore actionable ways to reduce what you pay:

- Shop around: Use tools like how to get multiple car insurance quotes to compare rates across carriers.

- Increase your deductible: A higher out‑of‑pocket amount shifts more risk to you, lowering the premium.

- Bundle policies: Combining home and auto, or adding renters to a homeowner policy, often unlocks multi‑policy discounts.

- Maintain a clean record: Safe driving, prompt bill payment, and no recent claims all signal lower risk.

- Invest in safety: Installing anti‑theft devices, fire alarms, or advanced driver‑assist systems can earn discounts.

Bundling isn’t just about convenience; it directly impacts the premium calculation. For a deeper dive on the benefits of bundling, see homeowners insurance and car insurance bundle for a comprehensive look.

Future trends: how premiums may evolve

Technology is reshaping risk assessment. Telematics devices in cars provide real‑time driving data, allowing insurers to price policies based on actual behavior rather than broad demographics. This “pay‑as‑you‑drive” model could make premiums more personalized and potentially lower for low‑risk drivers.

Similarly, climate change is influencing property and casualty premiums. As extreme weather events become more frequent, insurers may raise rates in high‑risk regions or adjust underwriting criteria to reflect the new landscape.

Artificial intelligence is also entering the underwriting arena, processing massive data sets faster than human actuaries. While AI can improve pricing accuracy, it may also introduce new regulatory challenges around fairness and transparency.

All these shifts circle back to the core question: why do insurance companies charge premiums? The answer evolves with risk, cost structures, and market forces, but the underlying principle remains—collecting enough funds to honor claims while staying financially sound.

In practice, your premium is a reflection of your personal risk, the insurer’s operational costs, and the broader market environment. By staying informed, regularly reviewing your policy, and taking proactive steps to lower your risk, you can keep the price you pay in line with the protection you receive.

Remember, a premium isn’t just a bill—it’s a promise that, when you need it most, the insurer will step in to help you recover. Understanding the why behind it empowers you to make smarter choices, negotiate better terms, and ultimately, safeguard your financial future.