Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Running a small business is a juggling act. You’re wearing many hats—manager, marketer, accountant, and often, chief HR officer. Among the many responsibilities, offering health care insurance to your team can feel like climbing a steep hill, especially when budgets are tight and regulations seem ever‑changing. Yet, providing health benefits isn’t just a nice‑to‑have; it’s a powerful tool for attracting talent, boosting morale, and staying competitive.

In recent years, the landscape of health care insurance for small business has evolved dramatically. From the Affordable Care Act’s employer mandate to a surge in “shop‑around” marketplaces, today’s owners have more options—and more complexity—than ever before. The good news? With the right knowledge, you can craft a benefits package that protects your employees without breaking the bank.

This guide walks you through the essential steps, from assessing your needs and navigating legal requirements to comparing plan types and leveraging cost‑saving tricks. Whether you have five staff members or fifty, you’ll find actionable insights to make informed decisions about health care insurance for small business. Let’s dive in.

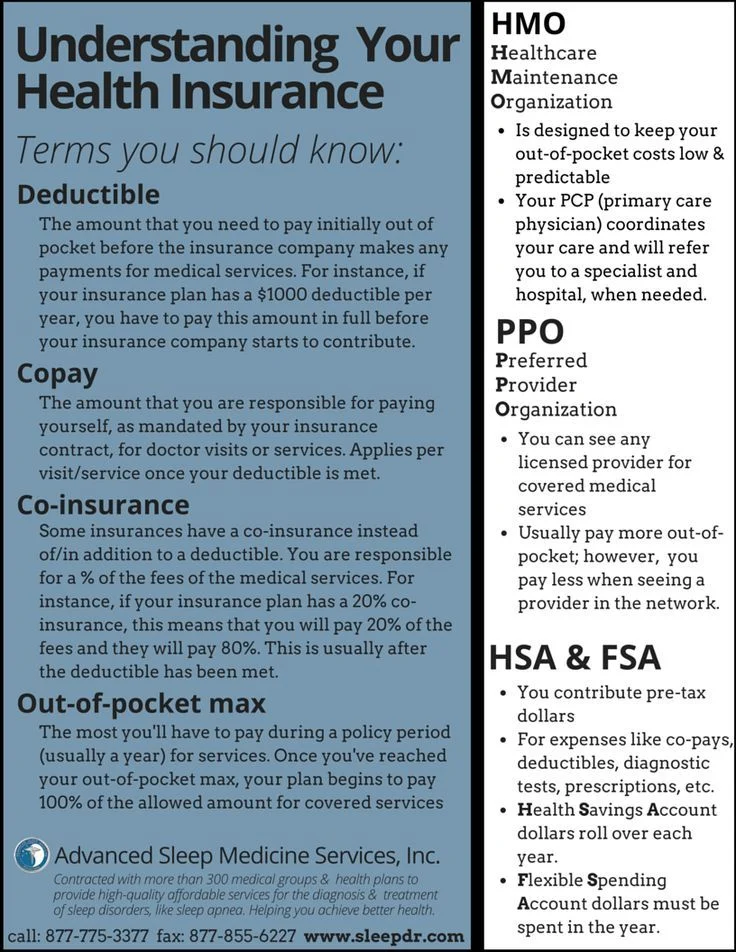

Understanding health care insurance for small business

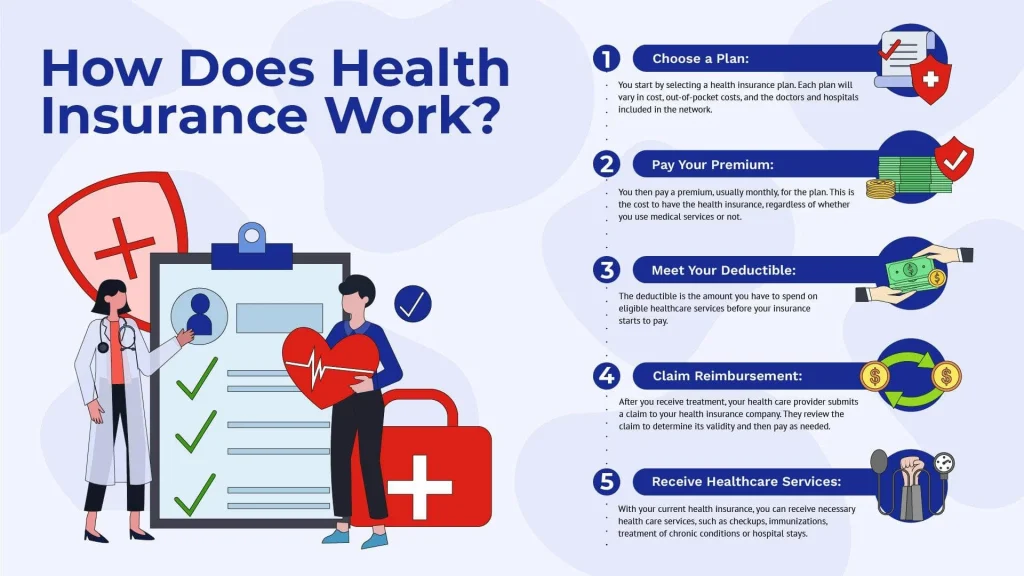

Before you start shopping for a plan, it’s crucial to grasp the basics of how health care insurance works for smaller employers. Unlike large corporations that can negotiate directly with insurers, small businesses often rely on group plans offered through state or federal exchanges, professional associations, or even private brokers. These plans bundle employees together, which can lower the per‑person premium compared to purchasing individual policies.

Key concepts to know:

- Group vs. Individual Coverage: Group plans usually provide better rates and broader networks, while individual policies may be more flexible but often come with higher premiums.

- Employer Contribution: Most small businesses cover a portion of the premium (commonly 50‑70%), leaving employees to pay the rest.

- Tax Advantages: Premiums paid by the employer are typically tax‑deductible, and employee contributions can be made pre‑tax, reducing overall payroll taxes.

Key considerations when choosing health care insurance for small business

Choosing the right plan isn’t just about the price tag. You’ll need to balance cost, coverage quality, and employee preferences. Here are the top factors to weigh:

- Employee Demographics: Younger staff may prioritize lower premiums, while families with children often look for comprehensive coverage and lower out‑of‑pocket costs.

- Network Size: A wide network means employees can see more doctors without referrals, which can be a decisive factor for retention.

- Plan Types: Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), and High‑Deductible Health Plans (HDHPs) each have distinct trade‑offs.

- Regulatory Compliance: Ensure the plan meets the Affordable Care Act (ACA) requirements for employer‑sponsored coverage, especially if you have 50 or more full‑time equivalents.

Popular plan options for small businesses

Now that you know what to look for, let’s explore the most common plan structures you’ll encounter.

Fully Insured Group Plans

In a fully insured arrangement, the insurer assumes the financial risk. You pay a predictable monthly premium, and the carrier handles claims, networks, and compliance. This model is straightforward and works well for businesses that prefer stability over flexibility.

Self‑Funded (or Self‑Insured) Plans

Self‑funded plans involve the employer paying claims directly, often using a third‑party administrator (TPA) to manage the paperwork. While this can lower costs for healthier workforces, it also exposes the business to higher risk and typically requires a larger employee base to be viable.

Health Reimbursement Arrangements (HRAs)

An HRA allows employers to reimburse employees for qualified medical expenses, including individual policy premiums. This hybrid approach offers flexibility and can be paired with a high‑deductible health plan (HDHP) to keep costs manageable.

Professional Association or Chamber of Commerce Plans

Joining a professional association can grant access to group rates that would otherwise be unavailable to small employers. These “association health plans” (AHPs) are especially attractive in industries with strong trade groups.

How to obtain accurate quotes and compare plans

Getting the best deal starts with gathering reliable quotes. Here’s a step‑by‑step process that keeps you organized:

- Identify your workforce profile: Count full‑time equivalents (FTEs), note dependents, and estimate average ages.

- Set a budget ceiling: Decide how much of the premium you’re willing to cover.

- Reach out to multiple carriers: Use brokers, online marketplaces, and association channels.

- Request detailed breakdowns: Look beyond the headline premium—consider copays, deductibles, and out‑of‑pocket maximums.

- Use comparison tools: Many sites let you juxtapose plan features side‑by‑side. For a quick illustration, see how payroll companies that offer health insurance can simplify the process.

When you compare, keep the following checklist in mind:

- Does the plan meet ACA minimum essential coverage?

- What are the total out‑of‑pocket costs for an average employee?

- How extensive is the provider network in your region?

- Are prescription drug benefits adequate?

- What wellness incentives or telehealth options are included?

Cost‑saving strategies without sacrificing coverage

Even with a limited budget, there are several tactics to stretch every dollar:

Leverage a High‑Deductible Health Plan (HDHP) with an HSA

Pairing an HDHP with a Health Savings Account (HSA) lets employees save pre‑tax dollars for medical expenses. Employers can contribute to the HSA as a perk, reducing the overall premium while still offering robust coverage.

Offer Tiered Plans

Provide a “baseline” plan that meets legal requirements and a premium tier with extra perks. Employees can choose based on their personal needs, and the employer only funds the baseline cost.

Encourage Preventive Care

Plans that cover annual exams, vaccinations, and screenings at no cost can lower long‑term claim expenses. Promote a wellness culture—think on‑site health fairs or subsidized gym memberships.

Shop Around Annually

Insurance markets are dynamic. Reviewing quotes each renewal period can uncover better rates or new plan features. Remember to factor in any changes to the why insurance companies charge premiums—such as shifts in medical inflation or regulatory updates.

Compliance checklist for small business owners

Staying on the right side of the law is non‑negotiable. Here’s a quick compliance rundown:

- ACA Employer Mandate: If you have 50+ FTEs, you must offer affordable, minimum‑essential coverage or face potential penalties.

- HIPAA Privacy Rule: Protect employee health information; limit access to authorized personnel only.

- ERISA Reporting: For group plans, file Form 5500 annually and provide Summary Plan Descriptions (SPDs) to participants.

- State‑Specific Regulations: Some states have “mini‑ACA” requirements that apply to smaller employers.

Consulting a knowledgeable broker or a payroll service that specializes in health benefits can help you navigate these obligations efficiently.

Real‑world examples: Small businesses that nailed their health benefits

Seeing how peers have succeeded can inspire your own approach. Below are two brief case studies:

Tech Startup in Austin, TX

The company adopted a tiered HDHP with an HSA contribution of $500 per employee. By negotiating a group rate through a local tech association, they reduced the employer share to 55% of the premium. The result? A 12% drop in overall benefits cost and a 30% increase in employee satisfaction scores.

Family‑Owned Restaurant in Detroit, MI

With only 12 staff members, the owner partnered with a regional payroll provider that bundled health insurance administration. They selected a fully insured PPO with a modest employer contribution. By promoting preventive care and offering on‑site flu shots, the restaurant saw a 15% reduction in claims during the first year.

Steps to launch health care insurance for your small business

Ready to take action? Follow this streamlined roadmap:

- Assess employee needs: Conduct a short survey to gauge interest, preferred plan types, and budget expectations.

- Set a contribution policy: Decide the percentage or fixed amount you’ll cover.

- Gather quotes: Reach out to at least three carriers or brokers.

- Compare and select: Use the comparison checklist above to choose the optimal plan.

- Enroll employees: Provide clear enrollment materials, deadlines, and FAQs.

- Educate the workforce: Host a benefits workshop or share an easy‑to‑read guide on using the new plan.

- Monitor and adjust: Review utilization reports annually and be ready to tweak contributions or switch plans if needed.

Throughout this process, remember that communication is key. Transparent discussions about costs, coverage, and the value of benefits foster trust and encourage higher participation rates.

In the end, offering health care insurance for small business is an investment—not just in your employees’ health, but in the long‑term stability and growth of your company. With the right plan, you’ll attract top talent, reduce turnover, and create a workplace culture that values wellbeing.

Take the first step today: evaluate your workforce, explore the options, and start building a benefits package that aligns with both your budget and your team’s needs. The right coverage is within reach, and the payoff—both financial and human—will be well worth the effort.