Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Running a business on your own can feel both exhilarating and daunting. You’re the boss, the marketer, the accountant, and often the front‑line service provider—all rolled into one. While the freedom of being a sole proprietor is a major perk, it also means that any mistake you make can directly impact your personal finances. That’s where professional liability insurance for sole proprietorship steps in, offering a safety net that lets you focus on growing your brand without constantly looking over your shoulder.

Think about the last time a client asked for a refund because a project didn’t meet expectations, or when a misunderstanding led to a lawsuit alleging negligence. Even if you’re confident in your expertise, the legal costs and potential settlements can be overwhelming. Professional liability insurance—sometimes called errors and omissions (E&O) insurance—covers the financial fallout from claims that you failed to deliver a professional service as promised.

In this article, we’ll unpack the nuts and bolts of professional liability insurance for sole proprietorships, explore who really needs it, and give you practical tips on picking a policy that won’t break the bank. By the end, you’ll have a clear roadmap to protect yourself, your reputation, and your wallet.

Understanding Professional Liability Insurance for Sole Proprietorship

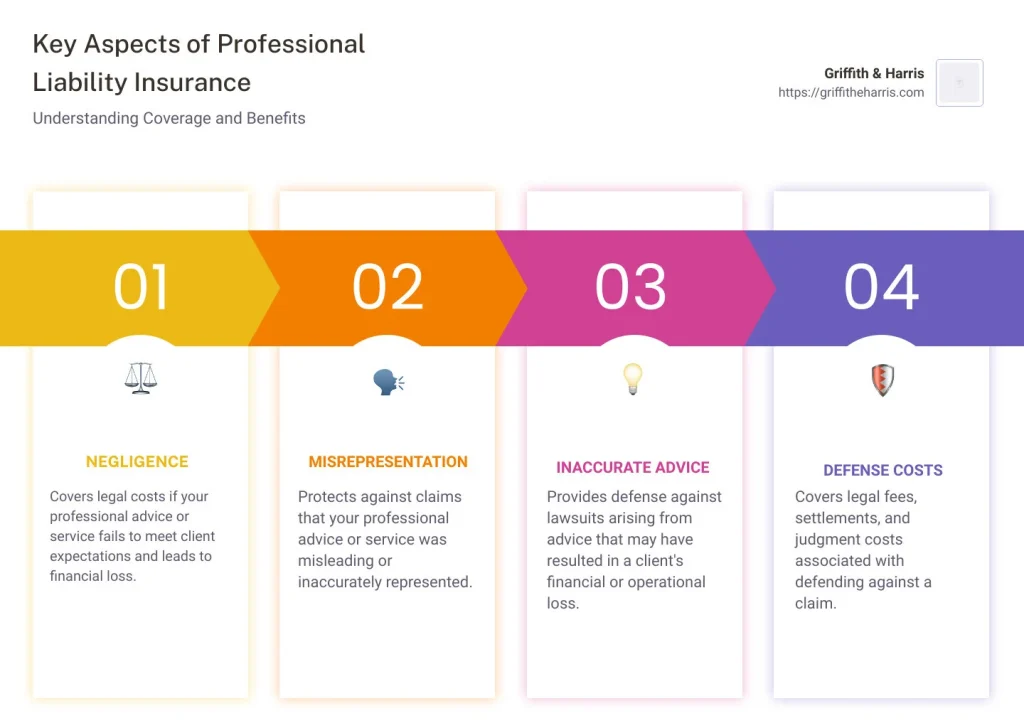

At its core, professional liability insurance for sole proprietorship is designed to protect individuals who provide specialized services—think consultants, designers, accountants, and even freelance developers. Unlike general liability insurance, which covers physical injuries or property damage, this coverage focuses on claims arising from mistakes, omissions, or negligence in the delivery of professional services.

Key elements of a typical policy include:

- Coverage limits: The maximum amount the insurer will pay per claim and in aggregate for the policy period.

- Deductibles: The amount you’ll need to pay out of pocket before the insurance kicks in.

- Defense costs: Legal fees, court costs, and settlement amounts are usually covered, often in addition to the policy limit.

- Exclusions: Most policies won’t cover intentional wrongdoing, criminal acts, or claims related to bodily injury.

Why Professional Liability Insurance for Sole Proprietorship Matters

Even if you’re the most diligent professional out there, human error is inevitable. One misplaced decimal, a misunderstood contract term, or a delayed deliverable can spiral into a costly lawsuit. For sole proprietors, there’s no corporate veil separating personal assets from business liabilities. That means your home, car, savings, and even retirement accounts could be at risk if you’re sued and can’t cover the damages.

Beyond the financial protection, having professional liability insurance can also boost credibility with clients. Many contracts now require proof of coverage before they’ll sign on the dotted line, especially in industries like consulting, IT services, and financial planning.

Who Should Consider Professional Liability Insurance for Sole Proprietorship?

While any solo professional can benefit, certain occupations are higher‑risk and often face contractual mandates for coverage. Here are some common examples:

- Consultants (business, management, HR)

- Financial advisors and accountants

- IT professionals and software developers

- Architects, engineers, and designers

- Legal practitioners and paralegals

- Healthcare consultants and wellness coaches

If you fall into any of these categories, or if you provide advice or services that could directly affect a client’s financial or operational outcomes, professional liability insurance for sole proprietorship is a smart investment.

How to Choose the Right Professional Liability Policy

Picking the perfect policy can feel like navigating a maze, but focusing on a few core criteria will simplify the process. Below are actionable steps to help you land a policy that aligns with your risk profile and budget.

Assess Your Risk Exposure

Start by mapping out the services you offer and the potential errors that could arise. For instance, a freelance graphic designer might worry about copyright infringement claims, whereas a freelance tax preparer would be more concerned about errors in filing returns. Understanding the specific risks helps you determine the appropriate coverage limits and deductible levels.

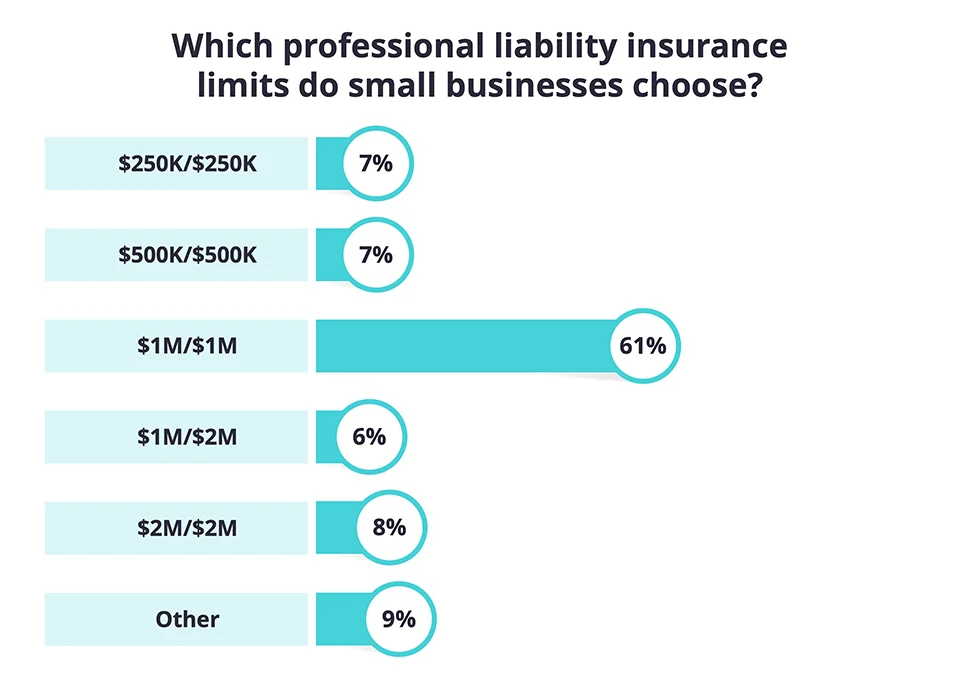

Compare Coverage Limits and Deductibles

Higher limits provide more protection but often come with higher premiums. A typical sole proprietor might opt for $1 million per claim with a $2 million aggregate limit, but if you handle high‑value contracts, you may need $2 million or more. Pair this with a deductible you can comfortably afford—$500 to $2,000 is common.

Check for Industry‑Specific Endorsements

Some insurers offer endorsements tailored to niche professions. For example, a tech consultant may need coverage for cyber‑related errors, while a health coach might want protection for advice that could be interpreted as medical guidance. Ensure any necessary endorsements are explicitly listed in the policy.

Read the Fine Print on Exclusions

Every policy has exclusions, and missing a critical one can leave you exposed. Look out for clauses that exclude “contractual liability” or “claims arising from services performed before the policy start date.” If anything seems vague, ask the insurer for clarification or a written endorsement.

Consider Bundling with Other Insurance

If you already have general liability, property, or even health insurance for your solo practice, ask about bundling discounts. Some insurers provide multi‑policy discounts that can shave a few hundred dollars off your annual premium. For a quick look at how bundling works, see our guide on Homeowners Insurance and Car Insurance Bundle: Save Money & Simplify Coverage.

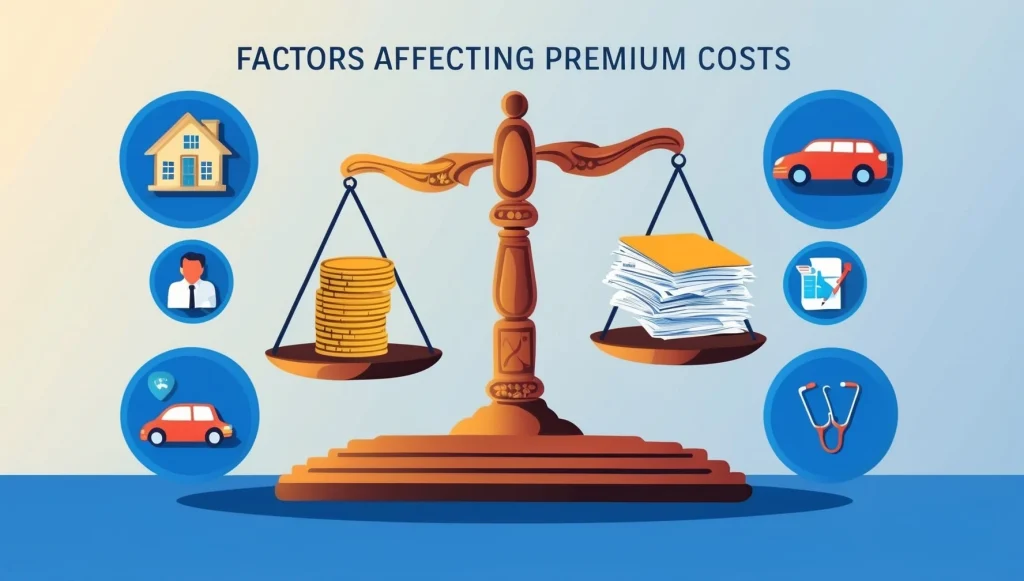

Cost Factors: What Determines Your Premium?

Professional liability insurance for sole proprietorship isn’t a one‑size‑fits‑all product. Premiums are influenced by a blend of personal and business factors, including:

- Industry risk level: High‑risk professions (e.g., financial advisory) typically see higher rates.

- Revenue and claim history: Higher annual revenue often means higher premiums, while a clean claim history can earn discounts.

- Geographic location: Some states have higher litigation rates, affecting premiums.

- Policy limits and deductibles: As mentioned, higher limits and lower deductibles raise costs.

- Experience and credentials: Demonstrated expertise, certifications, and professional memberships may lower rates.

Understanding these factors helps you negotiate better terms and avoid overpaying. For a deeper dive into how premiums are calculated across insurance types, check out Why Do Insurance Companies Charge Premiums? Understanding the Basics.

Filing a Claim: What to Expect

Even the best policies involve a claims process, and being prepared can make the difference between a smooth settlement and a prolonged headache.

Step‑by‑Step Claim Process

- Notify your insurer promptly: Most policies require you to report a claim within a certain timeframe, often 30 days.

- Gather documentation: Collect contracts, communications, work samples, and any evidence that supports your side of the story.

- Cooperate with investigators: Insurers will likely assign a claims adjuster to evaluate the situation. Provide honest, thorough information.

- Legal defense: Your insurer will usually cover attorney fees and court costs, but you may need to approve legal strategies.

- Settlement or judgment: If the case settles, the insurer pays up to your policy limits. If it goes to trial, the insurer may cover the verdict, subject to the policy terms.

Remember, the goal of professional liability insurance for sole proprietorship isn’t just to pay out claims—it’s to protect your reputation and help you navigate the legal landscape with confidence.

Common Misconceptions About Professional Liability Insurance

There are a few myths that tend to discourage sole proprietors from getting coverage. Let’s bust them:

- “I’m too small to be sued.” Even a single disgruntled client can file a lawsuit. The cost of defending yourself can dwarf any potential settlement.

- “My general liability policy is enough.” General liability covers bodily injury and property damage, not professional errors or advice.

- “It’s too expensive.” While premiums vary, many policies start as low as $300–$500 per year for modest limits. Bundling or opting for higher deductibles can lower costs further.

- “I don’t need it because I have contracts.” Contracts may shift risk to you, but they don’t replace insurance. In fact, many contracts require proof of professional liability coverage.

How to Save Money on Professional Liability Insurance for Sole Proprietorship

If budget constraints are a concern, consider these cost‑saving tactics:

- Shop around: Obtain quotes from at least three reputable insurers.

- Maintain a clean claim record: Insurers reward low‑risk clients with lower rates.

- Increase your deductible: A higher deductible reduces your premium.

- Take risk‑management courses: Some carriers offer discounts for completing accredited training.

- Bundle policies: Combine professional liability with general liability or property insurance for a multi‑policy discount.

For more budgeting tips on insurance, you might find the article on Cheap Car and Home Insurance Quotes – How to Find the Best Deals useful, as many of the principles apply across insurance types.

Real‑World Scenarios: When Professional Liability Insurance Saved the Day

Consider Sarah, a freelance web developer who accidentally deleted a client’s database during a migration. The client sued for $150,000 in lost revenue. Sarah’s professional liability policy covered legal fees and the settlement, saving her from personal bankruptcy.

Or look at Michael, an independent tax preparer who missed a critical deduction, leading to an audit and a $30,000 penalty for his client. His errors‑and‑omissions policy paid for the client’s penalty and the attorney fees, preserving Michael’s reputation and allowing him to continue his practice.

These stories highlight why professional liability insurance for sole proprietorship isn’t a luxury—it’s a practical tool that enables entrepreneurs to take calculated risks without fearing catastrophic financial fallout.

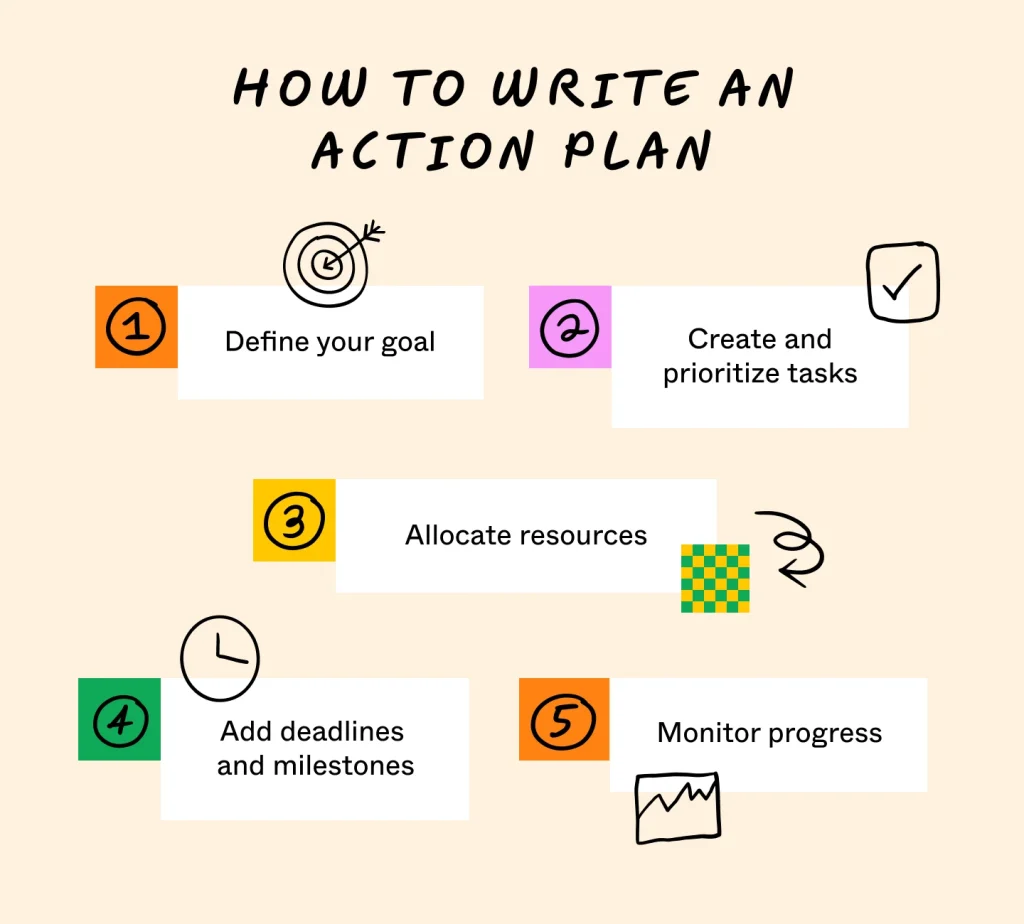

Getting Started: Your Action Plan

Ready to protect your solo venture? Follow this quick checklist:

- Identify the specific services you provide and the associated risks.

- Determine appropriate coverage limits based on contract values and potential losses.

- Gather quotes from at least three insurers, asking about industry‑specific endorsements.

- Review policy exclusions carefully—ask for written clarifications.

- Consider bundling with other policies you already hold to reduce costs.

- Finalize the policy that offers the best balance of protection and affordability.

- Keep your policy documents handy and set reminders for renewal dates.

By taking these steps, you’ll secure a safety net that lets you focus on delivering exceptional service, confident that a single mistake won’t jeopardize everything you’ve built.

Professional liability insurance for sole proprietorship may feel like just another line item on your expense sheet, but its true value lies in the peace of mind it brings. Whether you’re a seasoned consultant or just launching your first freelance gig, the protection it offers can be the difference between thriving and surviving. So, assess your risks, shop smart, and get covered—your future self will thank you.