Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Student loans can feel like a heavy backpack you’re forced to carry long after graduation. The good news? You don’t have to shoulder that weight forever. One popular strategy to lighten the load is refinancing a student loan with Sallie Mae. Whether you’re eyeing a lower interest rate, a shorter repayment term, or simply want to consolidate multiple loans into one tidy monthly payment, Sallie Mae offers a suite of options that can fit a range of financial situations.

In this guide we’ll walk through the nitty‑gritty of how Sallie Mae’s refinancing program works, who qualifies, what to watch out for, and how to maximize your chances of landing a deal that actually saves you money. By the end, you’ll have a clear roadmap for turning that burdensome student loan into a more manageable, cost‑effective financial instrument.

Understanding Refinancing a Student Loan with Sallie Mae

Refinancing, in the context of student loans, means replacing your existing loan(s) with a new loan that typically offers a lower interest rate or better repayment terms. When you choose to refinance a student loan with Sallie Mae, you’re essentially taking out a new private loan from Sallie Mae and using the funds to pay off your original loans—whether they’re federal, private, or a mix of both.

Sallie Mae, now part of the Navient family, has been a major player in the private student loan market for decades. Their refinancing platform is built on a straightforward online application, flexible repayment options, and a reputation for competitive rates—especially for borrowers with solid credit histories or a steady income stream.

Key Benefits of Refinancing a Student Loan with Sallie Mae

- Potentially Lower Interest Rates: If market rates have dropped since you first took out your loan, or if your credit score has improved, you could lock in a significantly lower APR.

- Single Monthly Payment: Consolidating multiple loans into one simplifies budgeting and reduces the chance of missed payments.

- Flexible Repayment Terms: Choose a term that aligns with your financial goals—shorter terms for faster payoff, or longer terms for lower monthly bills.

- Customizable Payment Options: Some borrowers can set up automatic payments for an extra rate discount.

When to Consider Refinancing a Student Loan with Sallie Mae

- You have a stable job and a reliable income source.

- Your credit score has risen to 700+ (the sweet spot for the best rates).

- You’re comfortable moving from federal loan protections (like income‑driven repayment) to a private loan.

- You’ve already paid off a portion of your loan and can demonstrate a positive payment history.

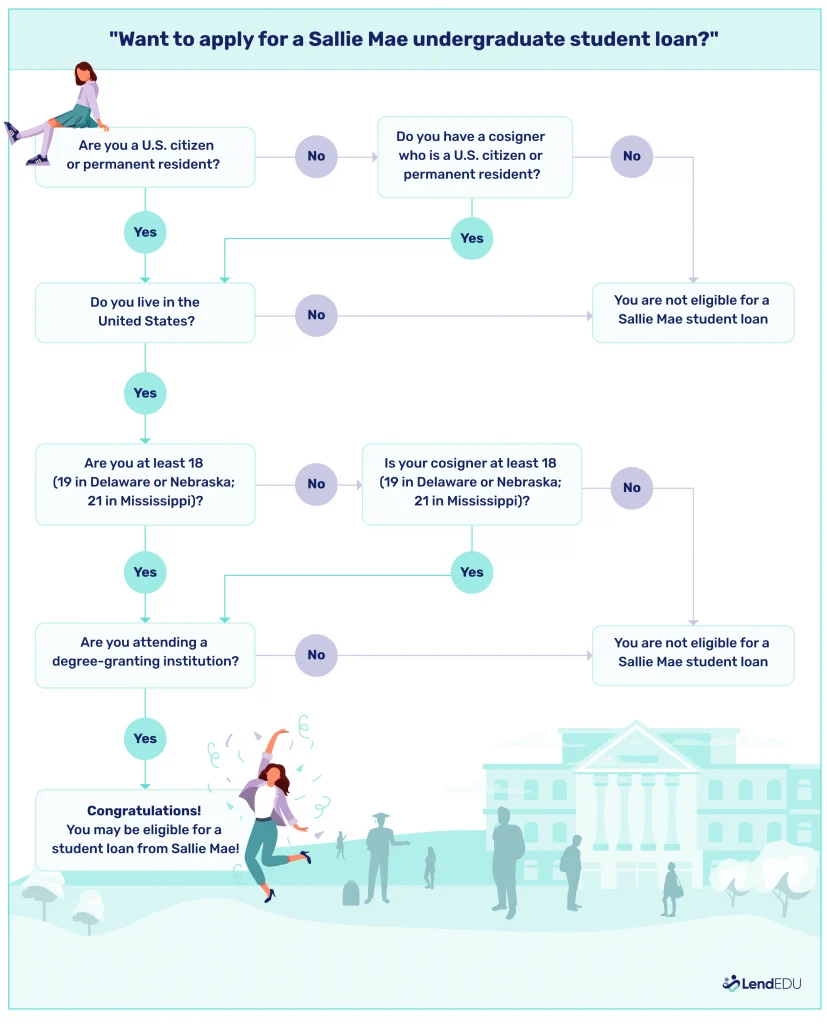

Eligibility Criteria and What Sallie Mae Looks For

While Sallie Mae’s exact underwriting algorithm is proprietary, the main factors that influence approval and rate offers include:

- Credit Score: Generally, a score of 680 or higher positions you for the most favorable rates.

- Debt‑to‑Income (DTI) Ratio: A DTI below 35% is ideal, showing you can handle additional debt.

- Employment History: Consistent employment for at least two years, especially with the same employer, boosts confidence.

- Loan Balance and Type: Larger balances may attract better rates, but Sallie Mae also considers whether the loan is federal or private.

It’s worth noting that refinancing a student loan with Sallie Mae does not require a cosigner for most qualified borrowers, though having one can still improve your rate if your credit profile is borderline.

How to Prepare Your Application

Before you dive into the online form, gather these documents to speed up the process:

- Recent pay stubs or proof of income (W‑2s, tax returns).

- Current student loan statements showing balances, interest rates, and servicer details.

- Bank statements for the past 30 days.

- Identification (driver’s license or passport).

Having everything at hand not only reduces friction but also helps you compare offers accurately. For instance, you might find that a lower rate from Sallie Mae aligns better with your cash flow than a higher‑rate private loan from another lender, a point explored in depth in Business Loans Based on Cash Flow – A Complete Guide.

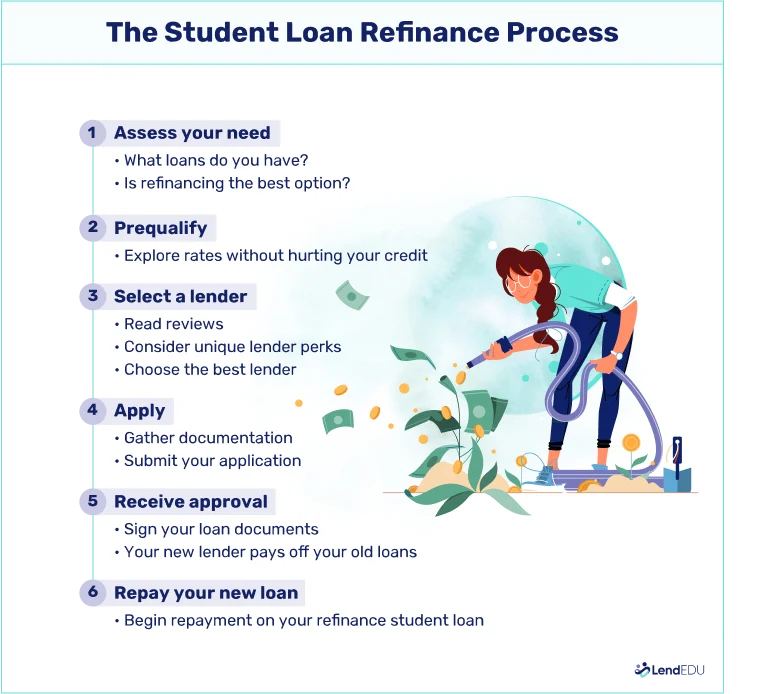

Step‑by‑Step Process for Refinancing a Student Loan with Sallie Mae

- Check Your Credit: Pull a free credit report to verify your score and spot any errors.

- Use the Sallie Mae Calculator: Input your current loan details to see potential savings.

- Submit the Online Application: Fill out personal, employment, and loan information. Upload the documents you prepared earlier.

- Review the Offer: Sallie Mae will provide a rate, term, and monthly payment estimate. Compare this with your existing obligations.

- Accept and Sign: If you’re satisfied, electronically sign the agreement.

- Loan Disbursement: Sallie Mae pays off your existing loans directly. You’ll start making payments to Sallie Mae according to the new schedule.

During the “Review the Offer” stage, pay special attention to any origination fees. While Sallie Mae often advertises “no fees,” some promotional rates might include a small upfront cost that could affect the overall savings.

Tips to Get the Best Rate When Refinancing a Student Loan with Sallie Mae

- Set Up Automatic Payments: Many lenders, including Sallie Mae, shave off 0.25%–0.5% APR for autopay.

- Consider a Shorter Term: Even a modest reduction in term can lower the total interest paid, though it raises monthly dues.

- Lock in Rates Quickly: Interest rates can fluctuate; if you receive a competitive quote, act fast.

- Maintain a Low DTI: Paying down other debts before applying can improve your rate eligibility.

Potential Drawbacks and What to Watch Out For

Refinancing isn’t a silver bullet. While refinancing a student loan with Sallie Mae offers many perks, there are trade‑offs to consider:

- Loss of Federal Protections: Federal loans come with income‑driven repayment plans, deferment, forbearance, and forgiveness options. Switching to a private Sallie Mae loan eliminates these safeguards.

- Variable vs. Fixed Rates: Some Sallie Mae products are variable. If rates rise, your payment could increase.

- Credit Impact: A hard inquiry will slightly dip your credit score. Multiple applications across lenders can compound the effect.

If you’re unsure whether giving up federal benefits is worth the potential rate cut, it can help to run the numbers side‑by‑side. Tools like the Does Rocket Mortgage Do VA Loans? A Complete Guide illustrate how different loan structures affect long‑term costs.

Comparing Sallie Mae to Other Private Lenders

When you’re refinancing a student loan with Sallie Mae, it’s wise to shop around. Here’s a quick snapshot of how Sallie Mae stacks up against a few competitors:

| Lender | Typical APR Range | Minimum Credit Score | Cosigner Allowed? |

|---|---|---|---|

| Sallie Mae | 3.00% – 9.00% (fixed) | 680 | Yes, optional |

| SoFi | 2.75% – 8.25% (fixed) | 700 | No |

| Earnest | 2.99% – 7.99% (fixed & variable) | 660 | Yes |

| CommonBond | 3.10% – 8.80% (fixed) | 680 | Yes |

While Sallie Mae’s rates are competitive, your personal profile will ultimately determine the exact offer. Using a side‑by‑side calculator can help you see whether the convenience of staying with a familiar lender outweighs a marginally lower rate elsewhere.

Case Study: How One Graduate Saved $5,000 by Refinancing with Sallie Mae

Emily, a 28‑year‑old software engineer, had $35,000 in federal student loans at 5.05% interest. After a promotion, her credit score rose to 720. She decided to refinance a student loan with Sallie Mae for a 5‑year term at 3.75% APR. The monthly payment dropped from $662 to $644, and over the life of the loan she saved roughly $5,000 in interest. The key moves she made:

- Paid off a small credit card balance to lower her DTI.

- Enabled autopay for an extra 0.25% discount.

- Locked in a fixed rate before market rates nudged upward.

This real‑world example underscores how timing, credit health, and strategic use of autopay can magnify the benefits of refinancing a student loan with Sallie Mae.

FAQs About Refinancing a Student Loan with Sallie Mae

Can I refinance only part of my loan?

Yes. Sallie Mae allows partial refinancing, letting you keep a portion of your original loan—useful if you want to retain federal benefits on a segment of the balance.

Do I need a cosigner?

A cosigner isn’t required for borrowers with strong credit and income. However, adding a cosigner can improve your rate if you fall below the preferred credit threshold.

What happens to my loan servicer?

Once Sallie Mae disburses the new loan, your previous servicer closes out the original account. You’ll receive a final payoff statement and then begin making payments directly to Sallie Mae.

Is there a prepayment penalty?

No. Sallie Mae does not charge penalties for early repayment, giving you flexibility to pay off the loan faster if your financial situation improves.

How long does the refinancing process take?

From application submission to funding, the timeline is typically 7‑14 business days, assuming all documents are in order and there are no underwriting issues.

Understanding these common questions can smooth the journey and help you avoid surprises after you decide to move forward with refinancing a student loan with Sallie Mae.

Bottom Line: Is Refinancing a Student Loan with Sallie Mae Right for You?

Ultimately, the decision hinges on a balance between savings potential and the value you place on federal loan protections. If you have a solid credit profile, a stable income, and are comfortable taking on a private loan, refinancing a student loan with Sallie Mae can shave off a few percent in interest, streamline your payments, and free up cash flow for other financial goals.

Conversely, if you anticipate needing income‑driven repayment, potential loan forgiveness, or you’re uncertain about future earnings, it might be wiser to keep your federal loans as they are and explore other strategies like income‑driven repayment plans.

Take the time to crunch the numbers, compare offers, and consider both short‑term and long‑term implications. With a clear picture, you’ll be equipped to make a choice that aligns with your financial roadmap, whether that means locking in a lower rate today or preserving flexibility for tomorrow.

Ready to explore your options? Start by checking your credit score, running a quick Sallie Mae refinance quote, and seeing how the numbers stack up against your current payment schedule. The sooner you act, the more likely you are to capture the best rates before market shifts occur.

Good luck on the journey to a lighter financial load—your future self will thank you.

[Finance]: Finance