Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Student loan debt has become a defining financial burden for many millennials and Gen Zers. While the average borrower carries tens of thousands of dollars in debt, the pressure to make monthly payments can feel relentless. At the same time, many workers are building up balances in their employer‑sponsored 401k plans, watching those contributions grow tax‑deferred year after year. It’s no surprise that the idea of tapping a 401k loan to pay off student loans pops up in financial forums, social media groups, and even casual dinner conversations.

Before you rush to the HR department and ask for a loan, it’s worth stepping back and asking some hard questions: Does borrowing from retirement savings really make sense? How does a 401k loan compare to other debt‑reduction tools? And most importantly, what are the hidden costs that could turn a seemingly smart move into a long‑term regret? This article unpacks the mechanics, the risks, and the potential rewards of a 401k loan to pay off student loans, giving you a clear roadmap to decide if it’s the right strategy for your financial picture.

We’ll walk through the eligibility criteria, the tax implications, and the impact on both your retirement timeline and credit profile. Along the way, you’ll find actionable tips, real‑world scenarios, and links to related resources—like why paying student loans with a credit card can be a risky alternative, or how a home equity loan might fit into a broader debt‑repayment plan.

How a 401k Loan to Pay Off Student Loans Actually Works

A 401k loan lets you borrow from your own retirement account, typically up to 50 % of your vested balance or $50,000—whichever is lower. The loan must be repaid with interest, but the interest goes straight back into your 401k, essentially paying yourself. Most plans require repayment over five years, though longer terms are allowed if the loan is used to purchase a primary residence.

When you take a 401k loan to pay off student loans, you’re essentially consolidating high‑interest, non‑tax‑deductible student debt into a lower‑interest, tax‑advantaged loan. The appeal is clear: your student loan interest rates often hover around 4‑7 % (or higher for private loans), while 401k loan interest is usually a modest 3‑5 % based on the prime rate plus a small margin.

Eligibility Requirements for a 401k Loan to Pay Off Student Loans

- Employer‑sponsored 401k plan that permits loans.

- At least one year of service with the employer (some plans may have a shorter waiting period).

- Vested balance sufficient to meet the 50 % or $50,000 cap.

- Ability to set up automatic payroll deductions for repayment.

If any of these boxes are unchecked, you’ll need to explore other debt‑relief options—perhaps a student loan credit‑card strategy (though that comes with its own set of cautions) or a traditional personal loan.

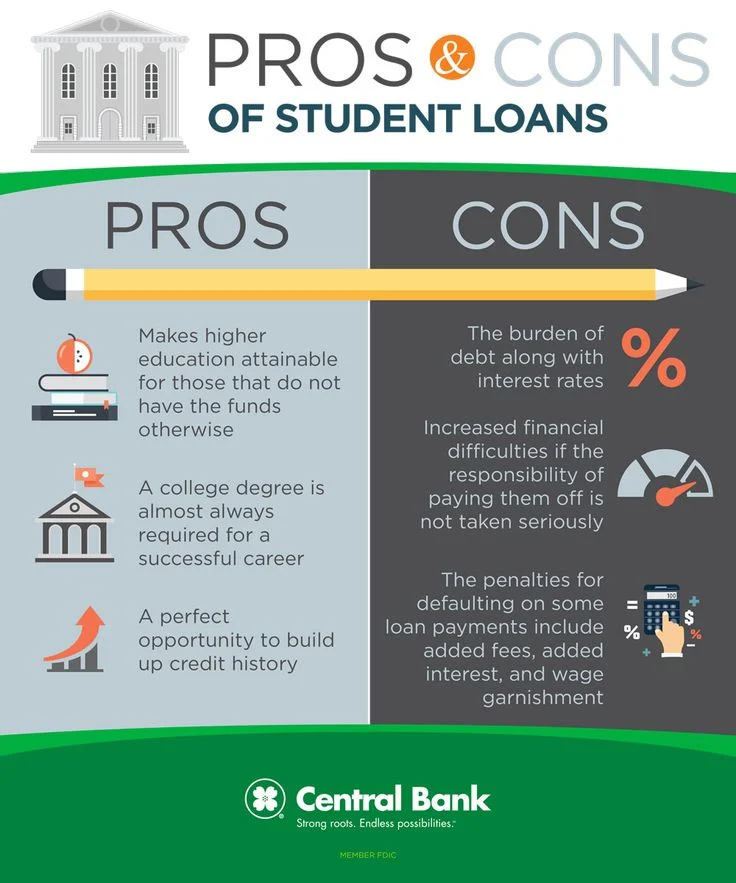

Pros of Using a 401k Loan to Pay Off Student Loans

When evaluated in isolation, a 401k loan can appear as a financial win‑win. Here are the most compelling advantages:

- Lower interest rate: You’re essentially paying yourself, which can be cheaper than federal or private student loan rates.

- Tax‑free repayment: Since the loan isn’t considered taxable income, you avoid the extra tax hit that a distribution would trigger.

- No credit check: Your borrowing limit is based on your vested balance, not your credit score, so a poor credit history won’t block you.

- Streamlined payments: Repayment is automatically deducted from your paycheck, reducing the risk of missed payments.

- Potential to boost retirement growth: The interest you pay goes back into your account, effectively increasing your retirement balance over time.

Cons and Risks of a 401k Loan to Pay Off Student Loans

Every financial decision carries trade‑offs, and a 401k loan is no exception. Below are the major pitfalls you should weigh before pulling the trigger.

Impact on Retirement Savings

While the interest you pay returns to your 401k, the principal you borrowed is no longer invested in the market. This “out‑of‑the‑market” period can cost you, especially if the market experiences strong growth during the loan term. A study from Vanguard showed that missing just one year of market returns could shave off 7‑10 % of a retirement portfolio’s final value.

Repayment Pressure and Job Loss

Loans must be repaid via payroll deductions. If you change jobs or lose your job, most plans require the outstanding balance to be repaid in full—usually within 60 days. Failure to do so turns the loan into a taxable distribution, and if you’re under 59½, you’ll also face a 10 % early‑withdrawal penalty.

Opportunity Cost of Tax‑Deferred Growth

Even though the interest is “paid to yourself,” the loan reduces the amount of money growing tax‑deferred. Over a 30‑year horizon, that compounding loss can outweigh the savings on student‑loan interest, especially if you’re in a high‑growth investment strategy.

Limited Loan Amounts

If your 401k balance is modest—say, $30,000—you can only borrow up to $15,000. This might not cover the full amount of your student loans, leaving you to juggle two separate debt streams.

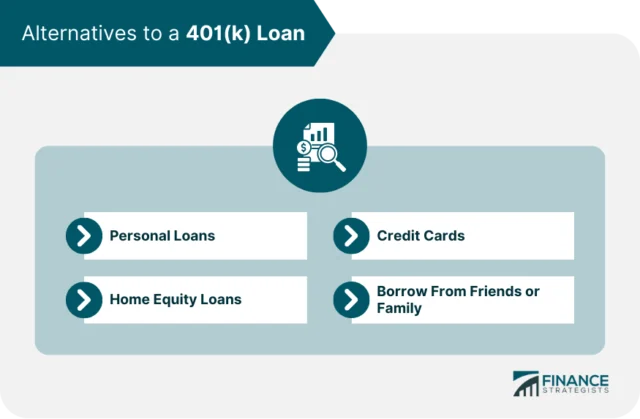

Comparing Alternatives: When a 401k Loan Isn’t the Best Choice

Before committing to a 401k loan to pay off student loans, explore other avenues that might preserve your retirement nest egg while still delivering debt relief.

- Refinancing with a private lender can lower your interest rate and extend the repayment term, but it may involve a credit check.

- A home equity loan often offers rates lower than student loans, though it puts your house at risk if you default.

- Income‑driven repayment (IDR) plans for federal loans can reduce monthly payments based on earnings, potentially freeing cash for other financial goals.

- Some employers offer student‑loan repayment assistance as a benefit—check with HR to see if that’s an option.

Step‑by‑Step Guide: Taking a 401k Loan to Pay Off Student Loans

If after weighing pros, cons, and alternatives you still feel confident, follow this structured approach to maximize the benefits and minimize the drawbacks.

Step 1: Verify Your Plan’s Loan Policy

Not all 401k plans allow loans. Review the Summary Plan Description (SPD) or ask your HR representative. Confirm the maximum loan amount, interest rate, and repayment schedule.

Step 2: Calculate the Break‑Even Point

Use a simple spreadsheet to compare the total interest you’d pay on your student loans versus the interest (plus lost market gains) on the 401k loan. Include the tax impact of a potential distribution if you default.

Step 3: Apply for the Loan

Most plans provide an online portal. You’ll need to specify the loan amount and the purpose—some plans require a statement that the loan is for “debt consolidation.” Submit any required paperwork, and the funds are usually deposited within a few business days.

Step 4: Pay Off the Student Loans

Once the 401k loan is in your bank account, send a lump‑sum payment to your loan servicer. Make sure to get a confirmation that the loan is fully satisfied, and keep the documentation for your records.

Step 5: Set Up Automatic Repayment

Payroll deductions will start on your next pay period. Double‑check that the amount matches the agreed‑upon schedule, and monitor your 401k statements to see the interest being credited back.

Step 6: Re‑Evaluate Your Financial Plan Annually

Each year, review your retirement projections. If your investments performed well, you might consider making additional contributions to recover the growth you missed while the loan was outstanding.

Real‑World Scenarios: Who Benefits Most?

Understanding the profile of borrowers who typically profit from a 401k loan to pay off student loans can help you see if you fit the mold.

- High‑earning professionals with sizable 401k balances: They can afford to take a loan without jeopardizing retirement, and the lower interest rate makes a noticeable dent in their debt.

- Individuals with unstable credit: Since the loan doesn’t require a credit check, it can be a lifeline for those denied conventional refinancing.

- People expecting a job change soon: If you anticipate a new job with a higher salary, you can repay the loan faster and rebuild retirement contributions quickly.

Conversely, if you’re early in your career, have a modest 401k balance, or work in an industry with high turnover, the risks may outweigh the benefits.

Tax Implications You Can’t Ignore

While a 401k loan isn’t taxable as income, the repayment structure has subtle tax effects. The interest you pay is not deductible on your tax return, unlike mortgage interest. Moreover, if you fail to repay and the loan is deemed a distribution, you’ll owe ordinary income tax on the amount plus a 10 % early‑withdrawal penalty if you’re under 59½.

To stay on the safe side, treat the loan like any other debt: keep meticulous records, set reminders for repayment, and consider consulting a tax professional if you’re unsure about the consequences of a potential default.

Strategic Tips to Maximize the Benefits

- Pay the loan faster than the schedule: Extra payments reduce the period your money is out of the market, preserving compounding growth.

- Increase your 401k contributions after the loan is repaid: This helps you catch up on any missed growth and keeps your retirement on track.

- Combine with a budgeting overhaul: Use the cash‑flow relief from eliminating student loan payments to fund an emergency fund or invest in a Roth IRA.

- Stay employed with the same employer for the loan term: This eliminates the risk of a forced distribution due to job change.

Frequently Asked Questions About a 401k Loan to Pay Off Student Loans

Can I take a 401k loan if I have both federal and private student loans?

Yes. The loan can be used to pay off any type of student debt, but be mindful that federal loans offer forgiveness and income‑driven repayment options that you’ll lose if you pay them off early.

What happens if my employer changes the loan policy mid‑term?

Generally, existing loans remain intact, but you should review any plan amendments. Some employers may add fees or change interest rates, affecting your repayment cost.

Is there a limit on how many times I can take a 401k loan?

Most plans allow only one outstanding loan at a time, but you can take a new loan after the previous one is fully repaid.

Will a 401k loan affect my credit score?

No. Since the loan is not reported to credit bureaus, it won’t appear on your credit report. However, defaulting and converting the loan to a distribution can have indirect credit consequences if it triggers financial strain.

Can I use the loan to pay off student loans and still contribute to my 401k?

Yes, but your contribution limit may be reduced because the loan amount is considered part of your account balance. Verify with your plan administrator.

In the end, the decision to tap a 401k loan for student‑loan repayment is highly personal. It hinges on your current retirement balance, job stability, interest‑rate differential, and long‑term financial goals. By thoroughly analyzing the numbers, understanding the tax landscape, and planning for worst‑case scenarios, you can make an informed choice that aligns with both your present cash‑flow needs and your future retirement aspirations.

Remember, the goal isn’t just to eliminate debt—it’s to do so in a way that keeps your overall financial health on an upward trajectory. Whether you decide to go ahead with a 401k loan, refinance your student debt, or explore a home‑equity option, the key is to stay proactive, keep learning, and adjust your plan as life evolves.