Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Table of Contents

- Step‑by‑Step Guide for applying for a VA home loan

- 1. Verify Your Eligibility Before applying for a VA home loan

- 2. Choose a VA‑Savvy Lender When applying for a VA home loan

- 3. Gather Your Financial Documents for applying for a VA home loan

- 4. Get Pre‑Qualified and Then Pre‑Approved

- 5. Find the Right Property

- 6. Submit Your Loan Application

- 7. VA Appraisal and Underwriting

- 8. Closing the Deal

- Key Tips to Strengthen Your Application When applying for a VA home loan

- Common Mistakes to Avoid while applying for a VA home loan

- Understanding Costs Beyond the Mortgage

- What Happens After You Close?

For many veterans, the prospect of owning a home feels like a distant dream—until they discover the power of a VA loan. The Department of Veterans Affairs backs these mortgages, offering zero‑down financing, competitive interest rates, and flexible credit requirements. If you’re a service‑member or a veteran wondering how to turn that dream into reality, the first step is applying for a VA home loan. Understanding the process, gathering the right paperwork, and knowing where to look for help can make the journey smoother and faster.

Unlike conventional mortgages, a VA loan is a benefit you earned through service, and it comes with unique rules that protect you from many of the pitfalls that first‑time buyers face. Whether you’re buying your first home, refinancing an existing mortgage, or looking to purchase a second property, the basics of applying for a VA home loan stay the same: you need to prove eligibility, demonstrate your ability to repay, and work with a lender who’s experienced in VA financing.

In this article we’ll walk you through every stage of the application process, from confirming eligibility to closing day. We’ll also sprinkle in practical tips, common mistakes to avoid, and a few insider tricks that can shave weeks off your timeline. By the end, you’ll have a clear roadmap for turning your VA loan entitlement into a set of keys.

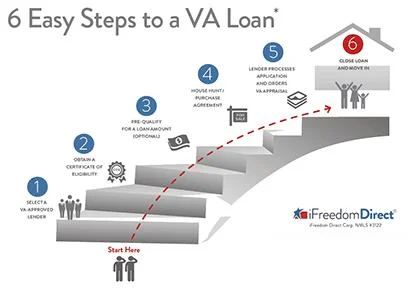

Step‑by‑Step Guide for applying for a VA home loan

The VA loan application isn’t a single, monolithic event—it’s a series of milestones that build on each other. Below is a logical sequence that most borrowers follow, with each step explained in plain language.

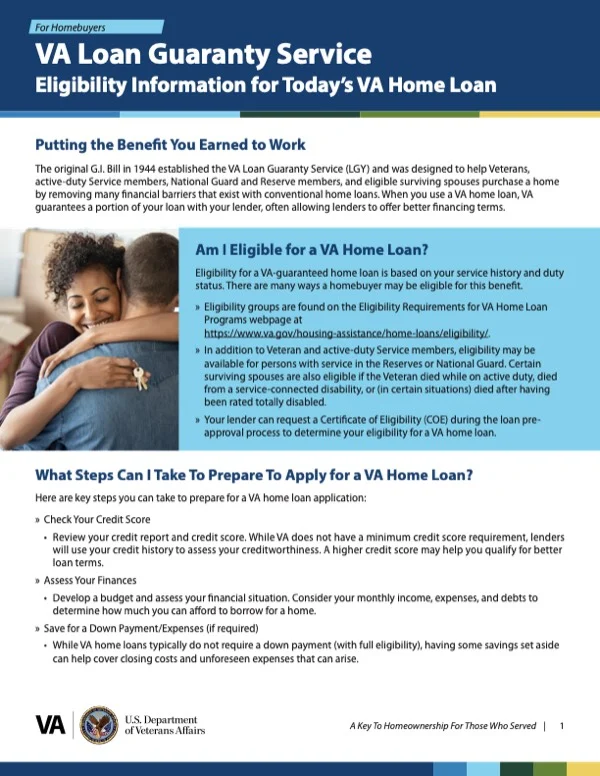

1. Verify Your Eligibility Before applying for a VA home loan

- Service requirements: You must have served 90 consecutive days of active duty during wartime, 181 days during peacetime, or at least six years in the National Guard or Reserve. Surviving spouses of service members who died in combat or from a service‑connected disability may also qualify.

- Certificate of Eligibility (COE): This is your golden ticket. You can obtain it online through the VA’s eBenefits portal, by mail, or via your lender who can request it on your behalf.

Having a valid COE is a prerequisite for applying for a VA home loan. Without it, lenders can’t verify that you’re entitled to the benefit.

2. Choose a VA‑Savvy Lender When applying for a VA home loan

Not every mortgage broker is familiar with VA guidelines. Look for lenders who advertise “VA‑approved” or “VA‑specialist” status. These lenders know the nuances—like how to calculate the VA funding fee, how to handle property appraisals, and which documentation is required.

Pro tip: ask for references from fellow veterans. A lender who consistently works with the VA will usually have a streamlined process that can reduce paperwork and speed up approval.

3. Gather Your Financial Documents for applying for a VA home loan

Even though VA loans are more forgiving on credit scores, lenders still need to see a solid financial picture. Common documents include:

- Recent pay stubs (last 30 days)

- Two years of tax returns (personal and, if self‑employed, business)

- Bank statements (last two months)

- Proof of any additional income (rental, bonuses, etc.)

- Debt statements (student loans, credit cards, car loans)

If you have existing student loans, you might wonder how they affect your VA loan application. For a deeper dive on this topic, check out Does Student Loan Appear on Credit Report? Everything You Need to Know. Understanding how these debts appear on your credit report can help you plan a stronger application.

4. Get Pre‑Qualified and Then Pre‑Approved

Pre‑qualification is a quick, informal estimate of how much you might be able to borrow based on the information you provide. Pre‑approval, however, involves a full credit pull and document review, resulting in a conditional commitment from the lender.

For a more detailed walk‑through of the pre‑approval process, see Get Pre Approved for VA Home Loan – Step‑by‑Step Guide. This step is crucial because sellers take offers backed by a pre‑approval more seriously.

5. Find the Right Property

VA loans have specific property requirements. The home must meet the VA’s Minimum Property Requirements (MPRs), which ensure it’s safe, structurally sound, and sanitary. Common issues that can delay closing include poor drainage, cracked foundations, or inadequate heating.

If you’re eyeing a fixer‑upper, remember the VA’s guidelines are stricter for homes that need extensive repairs. In many cases, a VA renovation loan (the “VA Rehab Loan”) may be a better fit, allowing you to roll repair costs into the mortgage.

6. Submit Your Loan Application

With your COE, lender, and property chosen, you’ll complete the VA loan application (VA Form 26‑1880). This form captures basic personal data, loan amount, property details, and the funding fee you’ll owe.

The funding fee varies based on your military category, down‑payment amount (if any), and whether it’s your first use of the benefit. For example, first‑time borrowers with no down payment typically pay a 2.3% funding fee, while subsequent users might pay 3.6%.

7. VA Appraisal and Underwriting

Once the application is in, the VA orders an appraisal to confirm the home meets MPRs and is priced fairly. Unlike a traditional appraisal, the VA appraisal also checks for “safety hazards” and “deficiencies.” If the appraisal comes back with issues, you’ll need to negotiate repairs with the seller or request a price reduction.

After a clean appraisal, the lender’s underwriter reviews every piece of the puzzle—credit, income, debt‑to‑income ratio, COE, appraisal, and more—to issue a final loan decision.

8. Closing the Deal

Closing day is when you sign the mortgage documents, pay any closing costs (or roll them into the loan), and receive the keys. Because VA loans often have lower closing costs, many veterans end up paying less out‑of‑pocket than with conventional loans.

Don’t forget to keep copies of all signed paperwork. Your COE, loan documents, and the closing disclosure are essential records for future reference, especially if you decide to refinance later.

Key Tips to Strengthen Your Application When applying for a VA home loan

- Boost Your Credit Score: While the VA doesn’t set a minimum score, most lenders prefer 620+. Pay down revolving debt and correct any errors on your credit report.

- Save for Closing Costs: Even though you can roll many costs into the loan, you’ll still need funds for the funding fee, appraisal, and title fees.

- Maintain Stable Employment: Lenders like to see at least two years of consistent employment. If you’ve recently changed jobs, be prepared to explain the move.

- Consider a Co‑Borrower: Adding a spouse with strong credit can improve your debt‑to‑income ratio, but remember the VA loan entitlement is still based on the veteran’s service.

- Shop Around for Rates: VA loans are offered by many banks, credit unions, and mortgage companies. Even a small rate difference can save you thousands over the life of the loan.

Common Mistakes to Avoid while applying for a VA home loan

- Skipping the pre‑approval stage and making an offer without a conditional commitment.

- Overlooking the VA funding fee and assuming it’s “free.” The fee is a one‑time cost that can be financed.

- Choosing a property that fails the VA’s MPRs, leading to costly repair negotiations.

- Failing to disclose all debts, especially student loans, which can affect the debt‑to‑income calculation.

- Not communicating with your lender about changes in employment or income during the underwriting period.

Speaking of student loans, if you’re juggling them alongside your VA loan, you might wonder whether taking a 401(k) loan could help. The article 401k Loan to Pay Off Student Loans – What You Need to Know explains the pros and cons of that strategy.

Understanding Costs Beyond the Mortgage

Even though a VA loan eliminates the need for a down payment, you’ll still encounter other costs:

- Funding Fee: Typically 2.3%–3.6% of the loan amount, but exempt for certain veterans with service‑connected disabilities.

- Closing Costs: Including title insurance, recording fees, and escrow deposits. Lenders can’t charge you a “VA fee” beyond the funding fee.

- Homeowner’s Insurance & Property Taxes: These are escrowed into your monthly payment.

- Optional Services: Such as a VA loan “certificate of eligibility” expedited service, or a home warranty.

If you’re curious about other types of equity financing, you might find the guide Applying for a Home Equity Loan: Complete Guide & Tips helpful for future reference.

What Happens After You Close?

Once you’ve crossed the threshold into homeownership, the VA loan doesn’t end—it merely transitions into the repayment phase. Here are a few things to keep in mind:

- Automatic Payments: Setting up automatic monthly payments can help you avoid missed due dates and potentially earn a small interest rate discount.

- Refinancing Options: The VA offers the Interest‑Rate Reduction Refinance Loan (IRRRL), also known as a “VA Streamline Refinance,” which can lower your rate with minimal paperwork.

- Entitlement Restoration: If you sell the home and pay off the VA loan, your entitlement is restored, allowing you to use the benefit again.

- Property Maintenance: Keep up with routine maintenance to preserve the home’s value and stay compliant with any future VA appraisal requirements.

Remember, a VA loan is a lifelong benefit. Treat it like a partnership between you, the VA, and your lender, and you’ll enjoy the stability and peace of mind that comes with a mortgage designed for veterans.

Applying for a VA home loan can feel like navigating a maze, but with the right preparation, a supportive lender, and a clear understanding of each step, the process becomes a straightforward path to homeownership. Whether you’re a first‑time buyer or a seasoned homeowner looking to refinance, the VA’s guarantee offers a unique blend of flexibility, affordability, and protection. Take the first step today—gather your COE, talk to a VA‑savvy lender, and start turning that “American Dream” into a reality you can truly call home.