Getrawbox Getrawbox

Getrawbox Getrawbox

Related Articles

Buying a home is one of the biggest milestones many veterans look forward to, and the VA home loan program is designed to make that dream more attainable. Before you start touring houses or submitting offers, the first practical step is to pre qualify for a VA home loan. Think of pre‑qualification as a quick health‑check for your finances—it tells you roughly how much you might be able to borrow and shows lenders that you’re a serious buyer.

Unlike a full loan application, pre‑qualification doesn’t lock you into a rate or require extensive documentation. It’s a conversation, usually done online or over the phone, where the lender reviews the basics: your income, employment, debt, and credit score. For many veterans, this early step can shave weeks off the home‑buying timeline and give you confidence when you start making offers.

Below, we’ll break down everything you need to know to pre qualify for VA home loan—from eligibility basics and credit considerations to the paperwork you’ll need and how to interpret the results. By the end, you’ll have a clear roadmap to get started and be ready to move from pre‑qualification to a full VA loan application with ease.

Understanding the VA Home Loan Eligibility

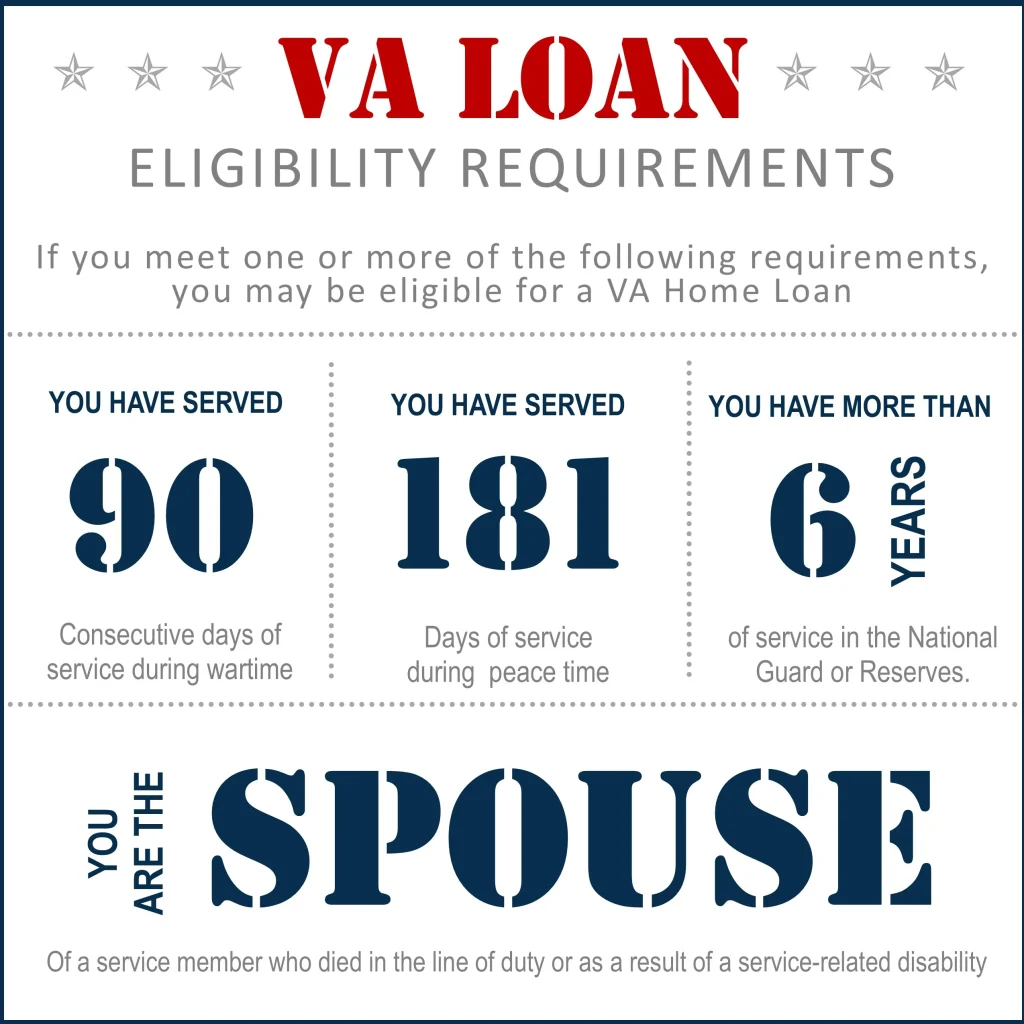

Before you even think about pre‑qualifying, make sure you meet the basic eligibility requirements. The VA loan program is available to:

- Active‑duty service members

- Veterans who have completed at least 90 days of service (or 30 days if discharged for a service‑connected disability)

- Reservists and National Guard members with at least six years of service

- Surviving spouses of veterans who died in service or from a service‑connected condition

Once you confirm eligibility, you’ll need a Certificate of Eligibility (COE). Most lenders can pull this directly from the VA’s eCOE system, but you can also request it through the VA’s website or by mail. Having the COE on hand simplifies the pre‑qualification conversation and shows lenders you’re ready to move forward.

Why Pre Qualify for VA Home Loan Before House Hunting?

There are several compelling reasons to pre qualify for VA home loan early in the process:

- Set realistic expectations: You’ll know a price range that matches your financial picture, preventing disappointment later.

- Strengthen your negotiating power: Sellers often favor buyers who have a pre‑qualification letter because it signals a smoother closing.

- Identify potential roadblocks: If your credit score needs a boost or your debt‑to‑income (DTI) ratio is high, you’ll have time to fix those issues before a formal application.

- Speed up the underwriting process: Lenders who already have your basic information can move faster once you decide to apply.

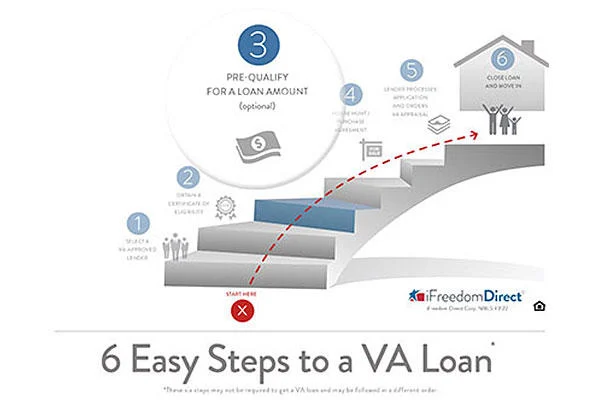

Step‑by‑Step: How to Pre Qualify for VA Home Loan

Step 1: Gather Basic Financial Information

Even though pre‑qualification is informal, lenders will still want to see a snapshot of your finances. Be ready with:

- Recent pay stubs (last 30 days)

- W‑2 forms or tax returns from the past two years

- Bank statements (checking and savings) for the last two months

- Details of any recurring debts (car loans, credit cards, student loans)

- Your current credit score (you can get a free report from annualcreditreport.com)

Step 2: Choose a VA‑Friendly Lender

Not all mortgage lenders specialize in VA loans, and some may have stricter internal guidelines. Look for lenders that advertise “VA‑approved” or “VA‑specialist” services. A quick Google search for “VA home loan lenders near me” or asking fellow veterans can point you toward reputable options.

Step 3: Submit a Pre‑Qualification Request

Most lenders provide an online pre‑qualification form. Fill it out with the data you gathered, and the lender will run a soft credit pull—meaning it won’t affect your credit score. Within a few minutes to a couple of days, you’ll receive a pre‑qualification letter that outlines the loan amount you’re likely eligible for.

Step 4: Review the Pre‑Qualification Letter

The letter will include:

- Estimated loan amount

- Assumed interest rate (subject to change)

- Estimated monthly payment, including principal, interest, and VA funding fee

- Any conditions you need to meet before a full application (e.g., improve credit score, lower DTI)

If the amount feels low, you can discuss ways to improve it—perhaps by paying down a credit card or waiting until you have a higher credit score.

Key Credit Factors That Influence Pre Qualification

While the VA itself doesn’t set a minimum credit score, most lenders have their own thresholds. A score of 620 is often the baseline, but aiming for 680 or higher can open the door to better rates and lower funding fees.

Here are some credit‑related tips to boost your chances when you pre qualify for VA home loan:

- Pay down revolving debt: Lowering credit card balances improves your DTI and credit utilization ratio.

- Correct errors on your report: Dispute any inaccurate items—these can drag your score down.

- Avoid new credit inquiries: Each hard pull can shave a few points off your score for a short period.

- Maintain a consistent payment history: Late payments are a red flag for lenders.

If you’re juggling student loans, check out our article on Does Student Loan Appear on Credit Report? Everything You Need to Know for more insight on how those balances affect your credit.

Understanding the VA Funding Fee and Its Impact

The VA funding fee is a one‑time cost that helps keep the program solvent. It varies based on:

- Whether you’re a first‑time or subsequent VA loan user

- Your down payment amount (if any)

- Your military category (e.g., regular, reserve, National Guard)

- Whether you have a service‑connected disability (in which case the fee may be waived)

When you pre qualify for VA home loan, lenders will estimate the funding fee and include it in the projected monthly payment. Knowing this upfront helps you budget more accurately.

Common Pitfalls to Avoid During Pre‑Qualification

- Skipping the COE: Some lenders will start the process without it, but you’ll need the certificate before a full loan can be approved.

- Relying on a single pre‑qualification letter: Different lenders may give you different estimates, so it’s worth checking a few.

- Overlooking hidden costs: Property taxes, homeowners insurance, and possible HOA fees can affect your overall affordability.

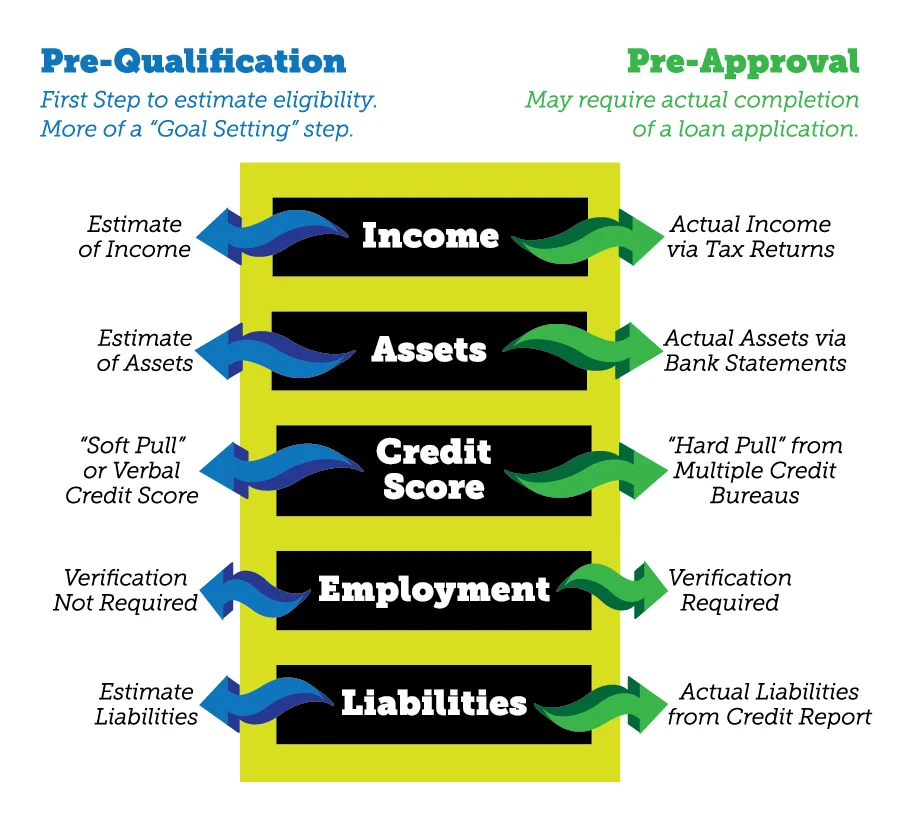

- Assuming pre‑qualification equals pre‑approval: Pre‑qualification is an estimate; pre‑approval requires a full credit check and verification of assets.

Next Steps After Pre‑Qualification

Once you have a solid pre‑qualification letter, you can start house hunting with confidence. When you find a property you like, the next move is to submit a formal loan application and move into the pre‑approval phase. If you want a deeper dive into that transition, check out Applying for a VA Home Loan: Complete Guide & Tips for step‑by‑step instructions.

Another useful resource is our Get Pre Approved for VA Home Loan – Step‑by‑Step Guide, which walks you through the documentation and timeline after you’ve secured a pre‑qualification.

Quick Checklist to Pre Qualify for VA Home Loan

- Confirm eligibility and obtain your COE

- Gather income, tax, and debt documentation

- Check your credit score and address any issues

- Choose a VA‑approved lender

- Complete the online pre‑qualification form (soft pull)

- Review the pre‑qualification letter and note any conditions

- Plan your house‑hunting budget based on the estimate

By following this checklist, you’ll position yourself as a well‑prepared buyer and set the stage for a smoother, faster loan approval once you’re ready to make an offer.

In summary, the journey to homeownership for veterans starts with a simple yet powerful step: pre qualify for VA home loan. It’s a low‑commitment way to gauge your borrowing power, spot any financial gaps, and show sellers you’re serious. With the right preparation, a clear understanding of credit factors, and the support of a VA‑experienced lender, you’ll be on your way to unlocking the benefits of the VA loan program and moving into the home you’ve earned.